CFTC Attempt to Improve SDR Data

The CFTC want to make the SDR data better. On December 22, 2015, when the financial markets had visions of sugarplums dancing in their collective heads, the CFTC snuck out a document, asking the industry to comment on their plans to increase reporting requirement for swaps. The document can be found here. At 68 pages […]

Liquidity Variables in the Swaps Market

We follow-up on a recent Bank of England study on the Swaps market. The Bank report finds that SEF trading has increased liquidity and decreased trading costs. Clarus data backs these findings up with 2016 data… …and shows that liquidity is much greater On-SEF than Off-SEF. This is an important and rigorous measurement of liquidity in today’s markets. Following […]

Volatility and Trading Volumes in Swap Markets

It’s been a volatile start to the year This has led to record volumes in benchmark swaps We explore the relationship between Volumes and Volatility in Swaps markets We find that there is a strong correlation worthy of investigation Volatility Everywhere Check this out from LPL Research via Advisor Perspectives – a six week change in […]

The Bank of England finds this interesting. So should you!

We use a recent Bank of England study to navigate Clarus data on the Swaps market. The Bank report looks at the impact of SEF trading on Rates markets… …showing that liquidity has increased and trading costs decreased. We bring the findings up to date, including API calls to replicate the study for our subscribers. Staff Research Staff […]

Is that a fair price? Measuring Swap Execution

Can we develop a way to understand and measure the execution of any trade? We look at the relationship between Tick Size and Trade Size. The price impact of a trade does vary with trade size…. …therefore a quantitative measure for execution quality is the natural next step. Revisiting the concept of Tick Sizes in USD Swaps, we are going to […]

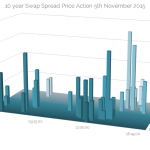

A sideways look at Swap Spreads

We take a look at Swap Spreads, this time by way of Cross Currency Basis swaps. We find that Cross Currency swaps are also moving sharply lower and have seen impressive volumes….. …..with increases in volumes around key price levels that have acted as support in the past. More negative Cross Currency levels would normally […]

Is Balance Sheet contraction driving Swap Spreads negative?

Are negative swap spreads solely caused by balance sheet contraction? There should be some hints in the data if this were the case. We look at the Open Interest in unfunded Swap Spreads by way of US Treasury Futures…. …and extend this to look at the product mix that trades between cash bonds, OTC and ETD products. […]

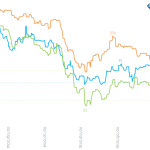

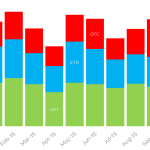

Negative Swap Spreads – Prices and Volume

Last Thursday was an exceptional day for Swap Spreads (a.k.a Spreadovers) in the US. We saw some large price moves, and these were significant enough for their increasingly negative levels to hit the mainstream financial press here, here and here. Prices As we can see in the chart below, Swap Spreads have been on a […]

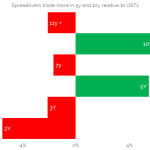

US Treasuries and Spreadovers – Market Comparisons

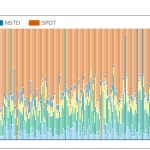

We compare Average Daily Volumes in US Treasury bonds to those in Spreadovers reported to the SDR Spreadovers account for about 2.5% of turnover of US Treasuries The maturity profiles of trading are broadly similar But Spreadovers have a greater concentration of trading in the 5y and 10y maturities. Half of all trades are not […]

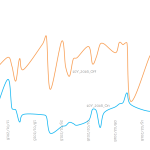

Swap Market Behavior on Fed-Day

Like many of you, I was tuned into CNBC last Tuesday to keep an eye on what the Fed decided to do with rates. Perhaps like many others, I also had SDRView Professional up and running on my desktop to see how the swap market was behaving. Here is what the 5YR USD swap was doing […]