SBSDR Part 3: Our SEC Comments

I reported on the progress of SBSDR’s a couple times over the past month, both here and here. Notably, May 31 2016 was the final day to comment on the ICE Trade Vault SBSDR application, which is the only application that has been made available to the public with a request for comment on the […]

USD OIS Swap Volumes Surge

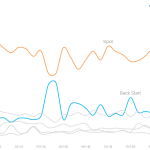

I last looked at USD OIS Swap Volumes in August 2015 and given that there is talk of a second Federal Reserve rate hike in June or July, I thought it would be interesting to look at what has been happening to volumes. First the highlights: USD OIS volumes are massively up and now comparable to […]

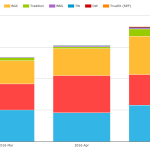

Fewer customer trades & more compression. How does a trader make money in a market like this?

We look at trade count data in the SDRs for Interest Rate Swaps in the major currencies There is evidence of reduced customer activity in large notional trades And a decrease in average trade size This is offset with an increase in Compression activity Those market trends are not very friendly towards traders trying to […]

SBSDR Part 2: What will SBSDR Cost?

A couple months ago, I published an article “SBSDR: The SEC Version of SDR” detailing the generalities of SBSDR – the new trade repositories intended to capture securities based swaps such as single name CDS and equity swaps. At the time, there had been no applications by potential candidates. Fast forward to today, and it appears as […]

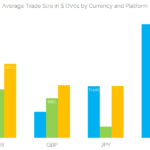

What’s the average trade size in swap markets?

We answer a simple question – what is the average size of a swap trade? We find that average size varies by maturity and currency Average trade size is also different between Dealer to Dealer and Dealer to Customer execution platforms. Overall, we find that USD swaps have the largest average trade size, at $45,000 in DV01 We’ve talked previously […]

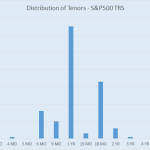

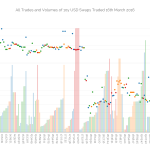

Equity TRS data on the SDR

Today I continue my analysis of equity derivatives data within the SDR, to see what other useful nuggets of data lie within there. Lets pick up from our previous analysis from a couple weeks back. As a refresher, I began by: Taking all March 2016 equity data (847,648 trades) Removed anything that was post-trade (terminations, […]

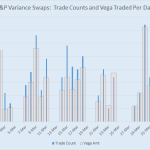

Variance Swaps and Other Equity Derivatives on SDR

You’re likely aware that we’ve been the de-facto “janitors” of the SDR data. However, to date, our focus has been on swaps traded in Interest Rates, Credit, and FX. This week I turned to the world of equity derivatives to see what’s lurking in there. To begin with, I had to grab some raw data. […]

Swaps Price Data – Painting the full Liquidity Picture

Clarus price data has unique features that you cannot find elsewhere Categorising traded prices by package type reveals trends that you cannot see in a flat data series Our curation programme and augmentation of prices adds to our volume analysis in Swap markets A true picture of liquidity can be painted using prices, volumes and price dispersion measures. 10y […]

SBSDR: The SEC Version of SDR

The CFTC began publishing rules about Swap Data Reporting in 2011, and we’ve come a very long way since then. Just read any of our blogs on SDR data and you’ll realize there is a world of data now on this once-opaque market. The SEC, however, took it a bit easier in their rulemaking for […]

US Swaps transparency has yielded numerous benefits

FOW (Futures & Options World) recently published my article on US Swaps transparency. If you are a subscriber to FOW, you can view the complete article here. Otherwise, the article is re-produced below. _________________________________________________________________________________ The Dodd-Frank Act requires both the real-time reporting of all OTC Derivatives trades done by US persons to Swap Data Repositories […]