The Land of Make Believe: Euribor and Eonia

Guest Blog Series Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused A wise man once asked me: Why don’t we all trade OIS instead of Libor swaps? The answer-in-a-nutshell goes something like liquidity, customer demand and habit. Certainly, if you look in the futures space, liquidity is concentrated overwhelmingly in […]

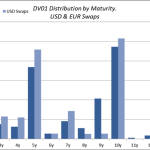

A Six Month Review of Swap volumes

In this article I will look at Interest Rate Swap data volumes and trends in the first half of 2014. This period includes both the start of mandatory SEF trading of IRS (February) as well as the expiry of package trade exemptions (May/June). USD IRS Volumes Lets start with On SEF USD IRS plain […]

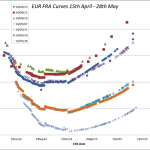

FRA Wars, Episode IV: A New Hope

In a Galaxy FRA, FRA away….the OTC FRA markets were murky places with no one really knowing how much traded during weekly volume matching sessions, or at what price. Enter Dodd Frank, Trade Reporting and Clarus Financial Technology. Now we can produce whole pricing curves from publicly disseminated data. With the right analysis, we can even […]

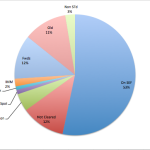

Oracle $10b Bond Issue, Looking for the Swaps

On June 30, Oracle issued $10 billion in bonds; the second largest corporate bond offering of 2014 after Apple’s $12 billion in April. In this article I will look for Interest Rate Swap trades associated with this bond issue. Bonds Issued Lets start with the bonds themselves, which were issued in 7 tranches. (See Financial […]

The Principals of Swap Trading

Guest Blog Series Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused Yes, that is principals not principles. We are not talking stop-losses or take-profit levels today, although you might be able to leverage a relative value strategy out of the findings. With the first two blogs focussing on specific market […]

A Voyeur’s Delight: Bond Issuance and Swaps

Guest Blog Series Guest Blogger Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused Gather round and let me tell you a (hypothetical) story…… After the ECB cut rates, a friendly Debt Capital Markets executive pitched an idea to the European Investment Bank about selling some USD bonds. The EIB were […]

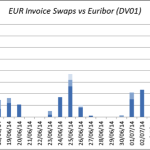

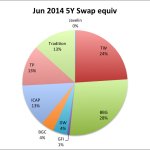

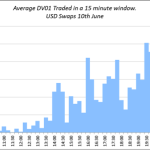

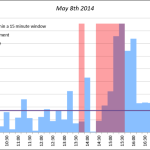

ECB June Meeting – Were EUR Swaps Traders at Lunch?

Guest Blog Series Guest Blogger Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused. When Amir approached me to guest write for the blog, I thought I would use the data to shine a light on the daily peaks and troughs of a swaps trader. After a few years trading, market […]

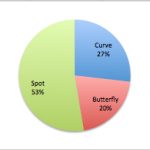

Swap Curve and Butterfly Package trades on Bloomberg SEF

In my recent articles Bloomberg SDR and SEF and Interest Rate Swap Prices, D2C vs D2D, I looked at different aspects of the data now available to us. In this article I am going to show that we can get an interesting insight into Swap Curve and Swap Butterfly trades. (Thank you to one of our regular […]

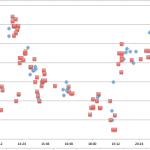

Interest Rate Swap Prices, D2D vs D2C, is there a difference?

In my recent article, Tick data for Swaps: What is now available, I noted that it would be interesting to look at price tick data and to do so for Interest Rate Swaps. While in my earlier article, Bloomberg SDR is now live, I showed an intra-day chart of prices for 5Y IRS comparing DTCC […]

Interest Rate Swaps, Spot vs Forwards, which is the greater?

In last weeks blog, SEF Package Exemptions, So Far So Good, I included a chart showing that 52.5% of USD IRS were On SEF and mentioned that there were lots of Forward Start Swaps that were Off SEF. Today I will take a look at these and provide a breakdown on the USD Swap types that […]