USD Swaps: Spreads and Butterflies Part III

This is Part III in a series. Please also see Part I and Part II. As we continue upon our noble goal of democratizing swaps market knowledge, we look into (maturity) spread prices and their volumes. We’ve so far been focussed on the previous FOMC meeting, but let’s bring the analysis a little more up-to-date […]

USD Swaps: Spreads and Butterflies Part II

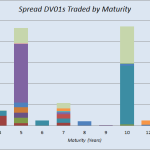

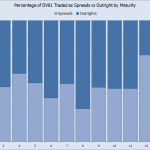

Please see Part I of this Spreads & Butterflies series here. Last week, we saw that up to 45% of vanilla, spot starting USD swaps can be considered part of a maturity spread. This week, we expand the analysis to identify exactly which spreads and butterflies are trading (for the sake of clarity, these blogs will […]

OTC Derivatives Reporting in Japan

Earlier this year I looked into European derivatives trade reporting (see EMIR Trade Reporting) and as not much of note has improved in the public dissemination of aggregate data in Europe, I thought I would look at Asia, starting with the largest market; Japan. While the Japanese FSA (JFSA) requires mandatory derivatives reporting to an […]

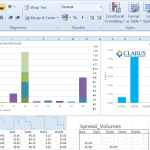

USD Swaps: Spreads and Butterflies Part I

In a new line of analysis for these blogs, we’ve been working on a first cut of data that expands upon the “trade types” that we identify. I think all traders and market participants will agree that there is inherent value in being able to identify whether a particular trade is an outright, one leg […]

What’s the Deal with Invoice Spreads and How Active Are They?

The final no-action relief of SEF packages is due to expire November 15, 2014. Many folks have turned to us asking if this will be something that significantly impacts the amount of trades being dealt On-SEF. BIT OF HISTORY Back when the no-action relief was first given in May, the November 15 date was by […]

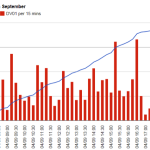

USD IR Swaps Summary Statistics

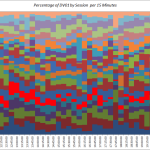

Sometimes the most simple questions are the most incisive. Having spent some time looking at the SDR data through the prism of the SDRView API, let’s take the time to lay down some simple descriptive statistics for the USD IR Swaps markets. What time do USD Swaps Open? The chart below makes it pretty clear: […]

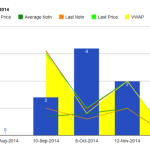

ECB Sep 2014 Meeting: EUR IRS Markets React

Following on from our look at June’s ECB meeting, and our prediction last week that markets would be shocked in the event of actual rate action, let’s take the opportunity to distill exactly what happened. Using SDRView Pro the drill-down nicely shows the ECB’s impact, with 5 years printing at a low of 0.433% shortly after […]

ECB September Meeting – Activity versus Price Indicators

Guest Blog Series Wow, the ECB meeting this week is an important one. It’s not immediately apparent, but when you look into the details of recent monetary policy announcements, this looks like the last chance the ECB has to cut rates until early 2015. Why? It all has to do with the structure of the new liquidity-providing […]

Super Mario’s EONIA Effect

Guest Blog Series Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused Super Mario to the rescue? No, not this Mario. Draghi was again even more dovish than expected at the central-banker’s annual shindig in Jackson Hole. Veering from the script, it looks like he’s ready to push the Bundesbank toward […]

Hawkeye and Super Slo-Mo for USD Swaps

Guest Blog Series Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused With the Premier League back, we’ll have the joys of Super Slo-Mo replays and Hawkeye reconstructing every kick of every game for the next nine months. What if we could have the same for every trading day? If you are […]