Last month, I posted a blog titled “Swaps, Actual Traded Prices and Size”.

Today I would like to make a correction in one of the interesting insights I noted in that blog. Namely the point that the “The price differences between UnCleared and Cleared Swaps can be observed and is sizeable” and I went on to note that this was 32 bps (!) for 5Y Swaps, which while surprising, I put down to higher credit risk, capital and funding cost.

This is in-fact wrong.

Prompted by two things; first enhancements to our SDR view and secondly the recent articles in the press on the error found in an Excel workbook used by Reinhart and Rogoff for a prominent research paper, I decided to re-check this finding.

In-fact there is less than 1 basis point difference in prices of USD 5Y Libor 3M Uncleared and Cleared Swaps.

What were these enhancements that led me to this correction?

- Firstly we separated out the Libor tenor basis, as for a number of years the major currencies show a significant spread between the price of a Swap reseting against 3M Libor to that reseting against 6M Libor, by looking at the prices for these separately.

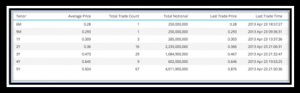

- Secondly as well as average price of all trades for a given maturity, we also show last traded price and the time for this.

- Thirdly we allow drill-down to the list of underlying trades and their prices.

The Traded Prices tab in our SDR View will now show (when we release the new version next week) the following:

From which we can see that the curve of Cleared Swap Prices and Bi-lateral (Uncleared) Swap prices corresponds very well, meaning these prices are within a few basis points.

The table below shows the last traded price and time for the trades on a given maturity.

And also supports drill-down to the actual trades that make up, say the 5Y maturity bucket.

Which then allows us to explain the apparent divergence in the curves at the 5Y point, as simply being bad data. So there is one 5Y Uncleared Swap where the fixed rate is 5.13%, as opposed to the 0.87%. Clearly this is most likely a Swap done at a chosen fixed rate, with either a floating side spread or an upfront fee to break-even; un-fortunately the DDR trade record does not provide these amounts.

Manually removing this trade, will remove the kink in the Uncleared Swap curve and so achieve a much better correspondance.

Also the curve is built from average prices of traded done at different times on the 23 April 2013 trading day and while there are 56 Cleared Swap trades, there are only 11 UnCleared Swap trades. Consequently rather than look at the difference in average prices, if we just look at the prices of the 11 Uncleared Swap trades and the prices of Cleared Swaps at similar times, we find that the difference in prices is less than 1 basis point.

All I can say in my defence was that the insight was number 9 out of 14, so not everyone may have got this far in the detail. If you did and are now reading this, please accept my apologies.

Either way, a lesson learned or more likely re-learned by me.

Check your assumptions and check and re-check your data, before making observations and drawing conclusions.

One thought on “Cleared Swap prices versus Bi-lateral Swap prices”

Comments are closed.