A new and interesting insight into the the Swaps market is provided by the transparency of actual traded prices and traded size that is now reported daily in the US to DTCC DDR.

A new Traded Prices tab in our SDR View can be used each day to view these prices.

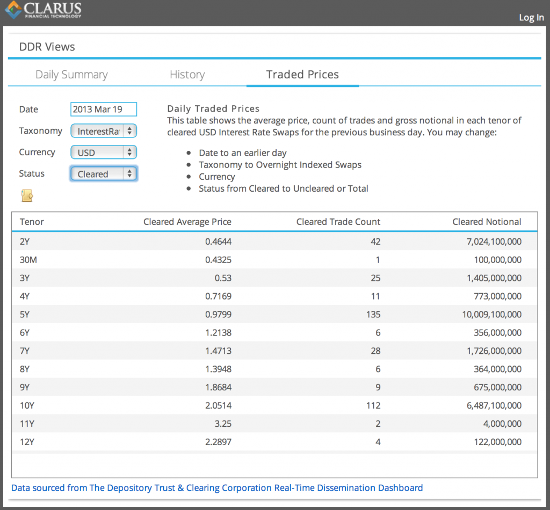

Interesting insights from this are:

- The large volume that is traded in vanilla Swaps for the 1Y,2Y, 3Y, 5Y, 7Y, 10Y, 30Y Swap tenors.

- In USD on Mar 19th for both Cleared and UnCleared this was $1.9b, $8b, $2b, $11.7b, $2b, $7.8b, $2b respectively from 651 trades, which was 86% of the total gross notional of par swaps traded that day.

- How few trades and gross notional is traded in all other swap tenors

- The cumulative notional of these other tenors being $5.7b from 106 trades, representing 14% of total par swap volume.

- The cumulative notional of trades we have excluded as not being standard par swaps (i.e. forward start) is $11b.

- This dominance in trade volumes of standard tenors, lends credence to the argument that Swap Futures or Note Futures may be able to serve as an alternative to Swaps.

- Unless the Swap market is in-fact providing liquidity and hedging to the Futures market and vice-versa, so the two markets depend on each other in a symbiotic relationship.

- Cleared Gross Notional of $34b and UnCleared of $7.6b, or 82% and 18% respectively, excluding the $11b of trades that are not par swaps e.g. forward start.

- The price differences between UnCleared and Cleared Swaps can be observed and is sizeable.

- For 2Y, 5Y, 10Y, 30Y, the average spread is 5bps, 32bps, 64bps & 63bps higher for UnCleared Swaps than Cleared Swaps.

- Which represents the higher credit risk, capital and funding costs of these.

- How comparatively little volume is done in currencies other than G4 by the firms reporting currently.

- As the US market represents around 30% of Swaps activity, we really need to get the European Swaps Repository up and running to provide a further 50% of total activity and so get a better insight into these currencies trading activity.

- Swap Desks should be able to work out their own daily market share in a currency, product and tenor; so no more claims of market share without the figures to back them up.

Granted our view is imperfect in that we make the following simplifications; we have averaged prices of trades done over a trading day, have averaged Libor 1M, Libor 3M and Libor 6M all together as opposed to determining average prices for each of these, have not distinguished between standard market size trades and very large trades. However we don’t believe allowing for these makes any meaningful change to the above observations.

We encourage you to use the SDR View yourself and invite you to give us your observations and feedback at [email protected]

2 thoughts on “Swaps, actual traded prices and size”

Comments are closed.