- The UK and Europe are currently consulting on both the Derivatives Clearing and Trading Obligations.

- Clarus are worried that the UK consultations risks a significant loss of transparency to markets. Particularly for USD.

- There appears to have been silence out of the CFTC on these important subjects.

- Europe has proposed covering some RFRs in the Clearing Obligation. This is good news for both market transparency and resiliency.

Things are getting very interesting in terms of clearing and trading mandates. There are different approaches being followed by the UK, Europe and the US.

The FCA’s CP21/22 consultation paper on “LIBOR transition and the derivatives trading obligation” gives us an opportunity to review what has been published so far and see what the future may hold.

Derivatives Trading Obligations

Starting with the most recent consultation, the UK’s FCA are consulting on whether to:

- Change the GBP derivatives trading obligation (DTO) from LIBOR swaps to SONIA swaps from the 20th December 2021. The scope of the covered instruments will also increase slightly, basically covering all standard SONIA swaps from 1y through to 30y either spot starting or IMM starting.

- Retain the current EUR DTO, so EURIBOR swaps continue to be subject to the trading obligation (2Y through to 30Y EURIBOR swaps). Neither EONIA nor €STR swaps will be subject to the DTO.

- Retain the current USD DTO, so USD LIBOR swaps continue to be subject to the trading obligation (2Y through to 30Y). Neither SOFR nor Fed Funds will be subject to the DTO.

These decisions intersect with the Derivatives Clearing Obligation (DCO) as well. This is because the rules for governing whether a derivative should be subject to a DTO are:

- the derivative should be subject to the DCO;

- it must be admitted to trading on at least one venue;

- it must be sufficiently liquid to trade only on venues.

We should therefore take a check on what is proposed for the DCOs in the UK as well.

Derivatives Clearing Obligations

The current consultation makes great use of plain English and uses well placed summary tables (e.g. Page 8) that highlight the proposed changes to the Derivatives Clearing Obligation:

| Currency | Current DCO | Proposed DCO |

| GBP | GBP LIBOR 28 day through to 50y maturities. GBP SONIA 7 day – 3 years | From 20th December 2021 GBP SONIA 7 day through to 50y maturities. |

| USD | USD LIBOR 28D – 50Y USD FedFunds 7D-3Y | No Change |

| EUR | EUR EURIBOR 28D – 50Y EUR EONIA 7D-3Y | From 18th October 2021 EUR €STR 7D – 3Y EUR EURIBOR 28D – 50Y (no change) |

| JPY | JPY LIBOR 28D – 30Y | Removed (i.e. no DCO in JPY) |

From this, you can see that the Derivatives Trading Obligation also has to change for GBP derivatives, because GBP LIBOR swaps will no longer be subject to the Derivatives Clearing Obligation (which is the first test for a DTO to be in place).

For USD and EUR markets there is no change to the underlying DCO. The UK regulators therefore have not proposed any changes to the DTO (apologies for the acronym over-load here).

Thoughts

A couple of things jumped out at me when I read through the two consultations. In no particular order:

- I thought that GBP LIBOR trades would continue to be subject to both the DTO and DCO. However, when you stop to think that CCPs will no longer be allowed to clear these derivatives (because the benchmark is ceasing), it does make sense to tidy up the regulation and remove all references to GBP LIBOR.

- I find the stance on USD LIBOR confusing. Regulators keep on referring to the US regulatory statements that no new business should be written against USD LIBOR, for example:

Milestones have been established by the national working group in the US, alongside supervisory guidance from US authorities that use of USD LIBOR in new contracts should stop by end-2021.

FCA CP21-22

This strongly suggests that USD Rates derivatives will all be traded versus SOFR from January 1st. And yet:

- There is no DCO for SOFR trades.

- There is no DTO for SOFR trades.

USD is by far and away the biggest market. Nearly half of new risk (40-49%) each month traded at LCH SwapClear is in USD swaps:

It strikes me that we risk the USD swaps market “going dark” much like pre-Dodd Frank. That is not a good result from this transition to RFRs.

A Clearing Mandate for SOFR makes sense

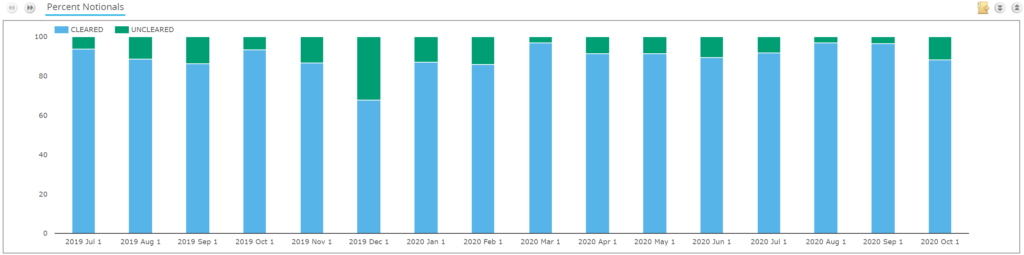

What does the data suggest regarding a DCO covering USD SOFR? SDR data from 2020 shows that over 90% of SOFR swaps were being cleared:

That includes the largest month for SOFR risk, in October 2020 when the discounting switches occurred. SOFR risk continued to be cleared, and there was only a relatively small uncleared market.

The DTCC and reporting counterparties still appear to have problems accurately reporting the cleared status of trades since the DTCC technological changes in November last year so we do not have reliable data to update this time-series.

However, it is fair to say that we have seen nothing suggesting there is a significant uncleared market in SOFR. If you are currently clearing USD LIBOR, you can also clear USD SOFR.

Therefore there is strong evidence that suggests the DCO should be extended to include all USD SOFR maturities.

Is There Evidence for a DTO in USD SOFR?

There is a strong regulatory push for USD trading to transition to only USD SOFR trades. Why is there no DTO proposed for USD SOFR swaps? Looking at the UK consultation papers;

- The liquidity assessments are well done and thorough.

- They use plenty of Clarus data, so I might be a bit biased in that assessment!

- There is also plenty of interesting data regarding European turnover volumes, trade counts etc. that we would love to have access to via MIFID data sometime soon!

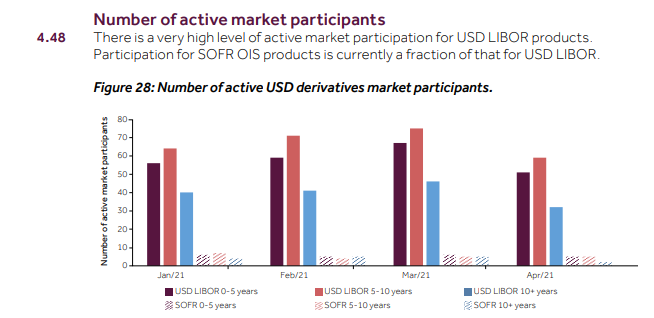

- There is also some interesting regulatory data, such as the number of market participants active in SOFR:

That chart alone seems to support what we have been thinking in private – some banks are largely ready to support SOFR transition but clients are not yet active in the market. If clients were active, you would expect a much higher number of SOFR participants than <10! It is also fair to say that if all banks were ready to transition then we would see more than 10 market participants too. That chart is not a great sign for SOFR adoption.

However we feel that the liquidity analysis misses one key ingredient – the proportion of markets already choosing to execute on venue in SOFR.

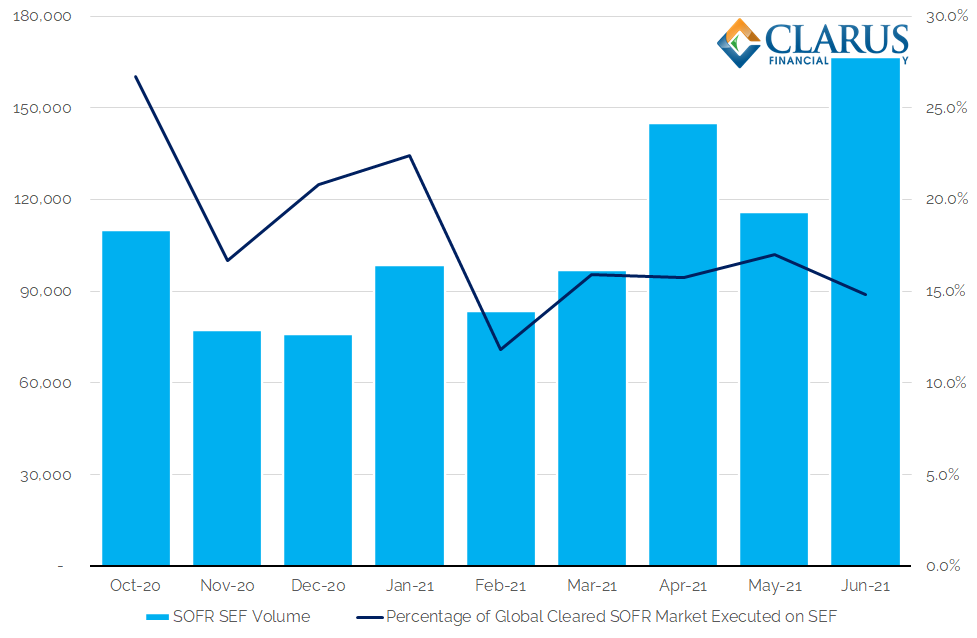

Combining our Clarus data sources, I can do this in Excel very quickly for SOFR:

Showing;

- SEF traded SOFR volumes versus total global cleared SOFR volumes.

- SEF volumes in SOFR continue to climb month-on-month.

- Over $165bn of SOFR-notional traded on-SEF in OTC Swaps during June 2021.

- Compared to the overall GLOBAL cleared SOFR market, this represented 15% of the market.

There is already 15% of the market that is choosing to execute SOFR risk on-SEF. This has been as high as 27% in some months – most notably when SOFR markets were the most active back in October 2020.

If ~1 in 6 trades are already executing on-venue voluntarily, isn’t this a good sign that markets are ready for a DTO?

The US and Europe

As far as I am aware, there has been silence out of the CFTC in the US on this subject. It appears Matthew Kulkin (former director of the CFTC’s Division of Swap Dealer & Intermediary Oversight) agrees:

In Europe, ESMA are currently consulting on both the Clearing Obligation and the Trading Obligation (woo-hoo!). Interestingly, the conclusions of ESMA are different to the UK!

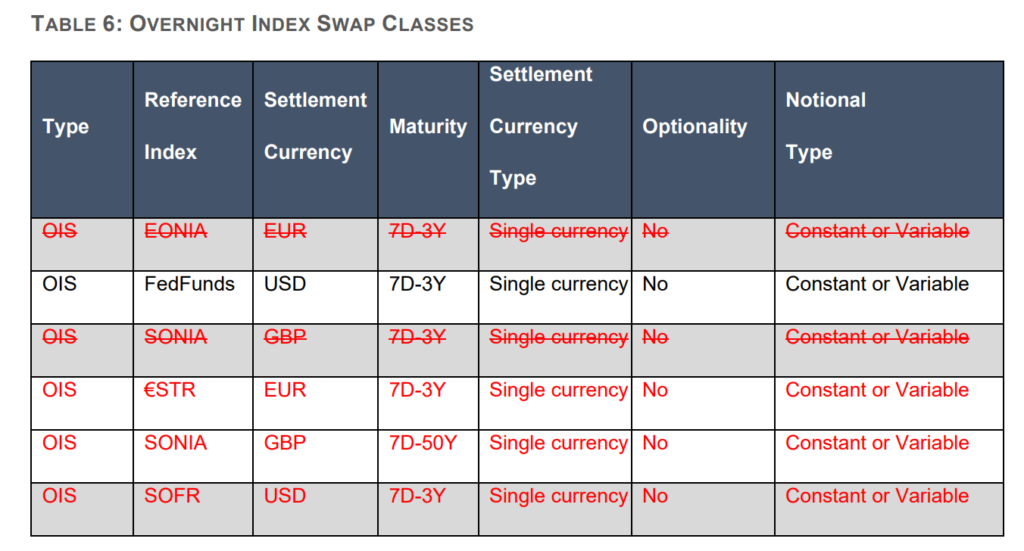

Take for example the Clearing Obligation in Europe (page 38), which proposes to remove GBP and JPY LIBOR but adds SONIA, €STR and SOFR:

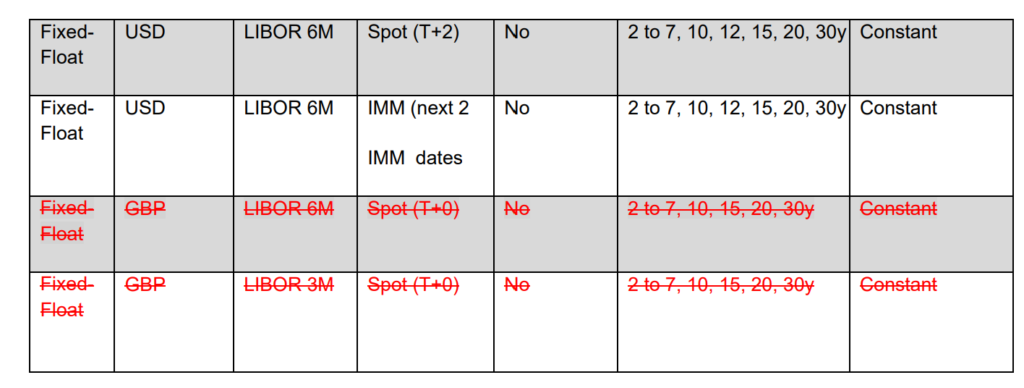

And secondly the Trading Obligation (page 50):

We have a single statement to make: we need to aim for regulatory harmony here!

In Summary

It is way beyond the work of a single blog to suggest how this regulatory harmony could be achieved, but hopefully readers are now aware that:

- The UK are currently consulting on both the Derivatives Clearing and Trading Obligations.

- Clarus are worried that these consultations propose rolling back both clearing and trading mandates which risks a loss of transparency to markets. Particularly for USD.

- Unfortunately, there appears to have been complete silence out of the CFTC on these important subjects. They were the leader in putting in place market reforms. Markets would be well served by a CFTC consultation for US markets.

- Europe has proposed covering some RFRs in the Clearing Obligation, namely short-dated €STR and SOFR and pretty much all SONIA contracts. This is good news for both market transparency and resiliency!