- Good morning, happy Monday and welcome to SOFR First day!

- SOFR activity accounted for 18% of the market (18:30pm London time).

- Today, Monday July 26th, is when a global initiative coined “SOFR First” comes into play for interbank markets.

As per the CFTC MRAC announcement two weeks ago:

SOFR First represents a prioritization of trading in SOFR rather than USD LIBOR, which is designed to help market participants decrease reliance on USD LIBOR by December 31, 2021

Market Risk Advisory Committee for CFTC

July 13, 2021

And back when the SOFR First proposal was first published by the MRAC, they stated:

The Subcommittee recommends that interdealer brokers replace trading of LIBOR linear swaps with trading of SOFR linear swaps. This step will cause trading activity amongst swap dealers on these platforms to switch from LIBOR to SOFR.

CFTC’s Interest Rate Benchmark Reform Subcommittee Recommends July 26 for Transitioning Interdealer Swap Market Trading Conventions from LIBOR to SOFR

Today’s blog is therefore very simple. A look at trading activity in USD swaps being published to the SDRs. Will the switch to SOFR be in evidence?

Monday July 26th 8am London

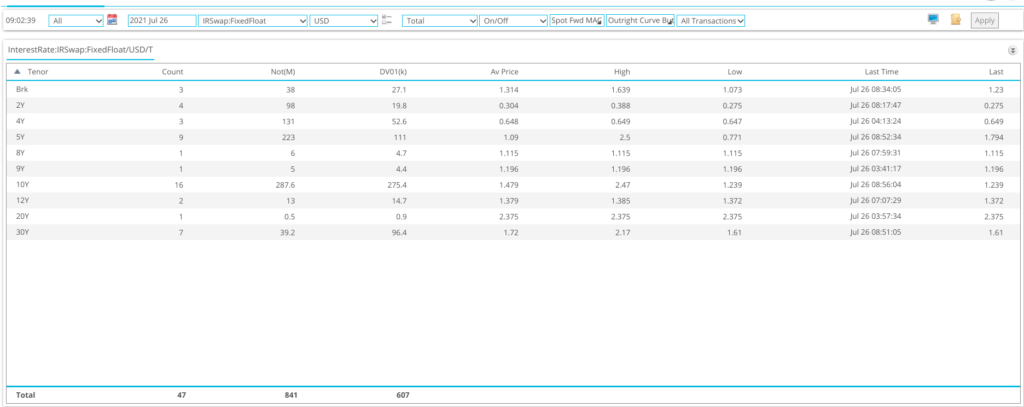

My first look at SDRView Pro today didn’t look like a very “SOFR First” glimpse of the market! We’ve already seen 47 USD LIBOR trades hit the SDRs, totalling $844m in Notional!

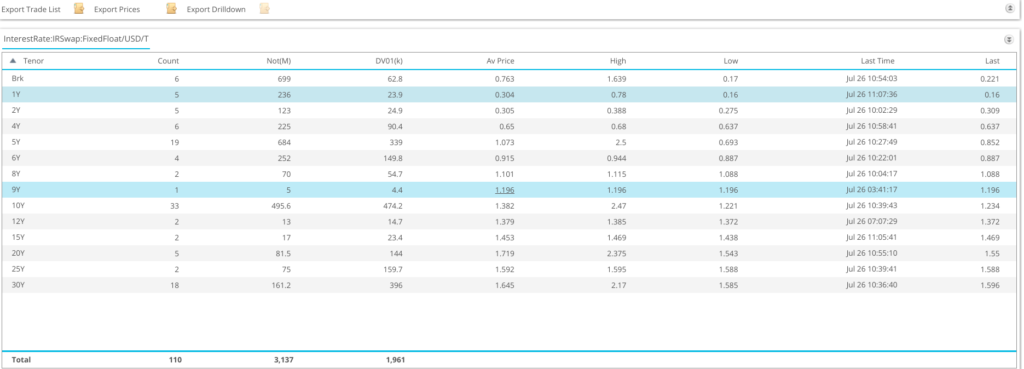

And of course the big problem with all of this continued LIBOR trading is that the exposures will continue long after USD LIBOR disappears in June 2023. 10 years has been the most active tenor so far today:

However, it is probably unfair to expect USD LIBOR trading to simply stop. So have we at least seen a decent amount of activity in SOFR so far today?

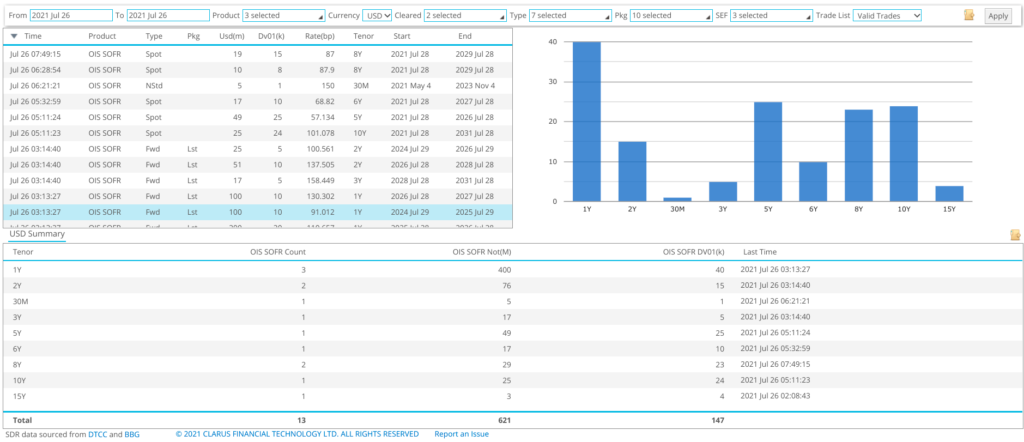

And the answer is YES! Yes we have:

Showing;

- 13 trades

- $621m notional

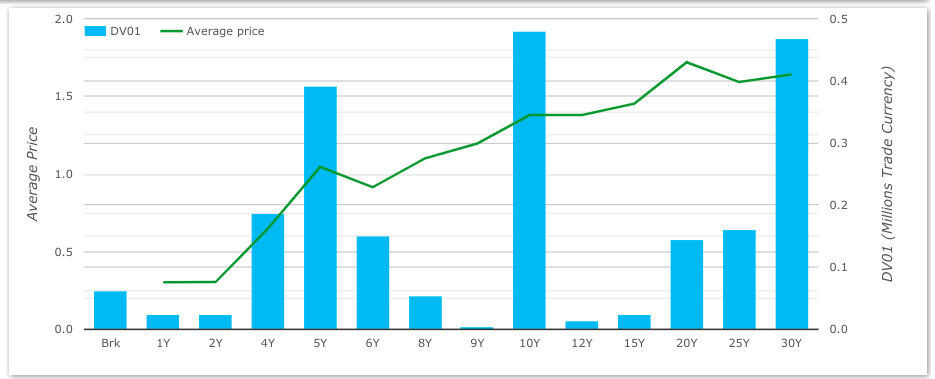

- Activity from 1Y all the way out to 15Y

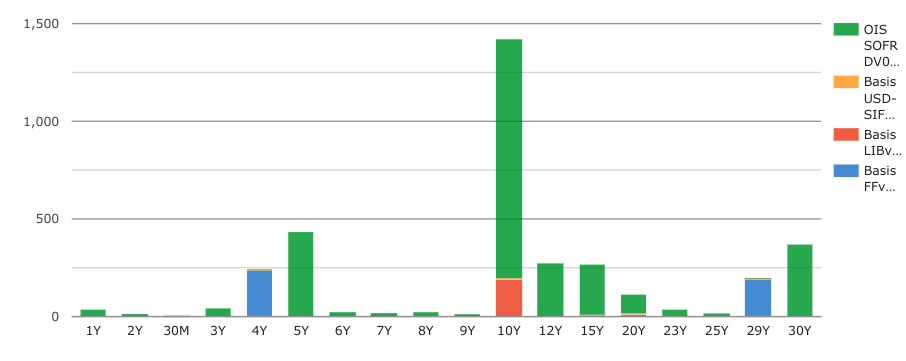

It is worth noting at this point that SOFR DV01 has totalled only $147K versus $610K (!) in LIBOR. But still, it is off to a relatively good start!

And another SOFR trade just hit the tape…..this could be a much busier blog than when I covered SONIA First. Twice.

9am London Monday 26th July

Scores on the doors after another hour of trading:

LIBOR

- $1,935m notional

- 70 trades (!)

- $1.23m DV01

SOFR

- $782m notional

- 18 trades

- $782k DV01

Whilst LIBOR is streaking ahead in terms of notional and trade count, a couple of things to consider here:

- SOFR First, in this instance, is targeted at interbank markets. If I, as a trader, ask my broker for a “5Y USD” price this Monday morning, I understand that the broker is meant to respond with a SOFR price as “standard market practice”.

- In terms of average trade sizes today: LIBOR is at $29m, $18k DV01 and SOFR at $43m, $15k DV01. Not too much of a difference, although it looks like there is more short-end SOFR trading. Certainly no clear indication that LIBOR trades are smaller clients and SOFR trades are large interbank trades so far.

9:20am London Monday 26th July

And what role do SEFs have to play in this transition? You may recall that last week I wrote that we are supportive of both Clearing mandates and Trading mandates in SOFR markets. The evidence is already strong this morning that both of those mandates would be welcomed by the market:

SOFR Trades Today

- 100% of SOFR trades have been Cleared.

- 95% (18 out of 19) have been executed on SEF. Remember that is voluntary – there is no execution mandate for SOFR trades!

The activity so far today shows how much the markets appreciate both clearing and platform execution, even for these new RFR markets.

9:30am London Monday 26th July

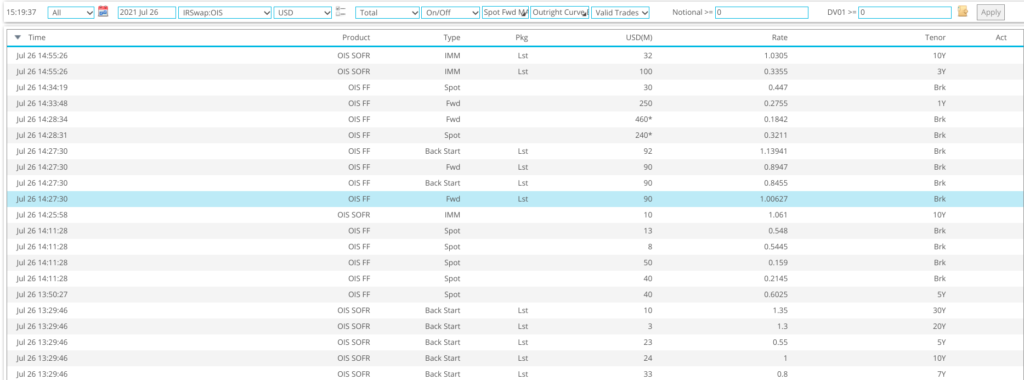

And now a more detailed look at the SOFR trading activity so far today.

And from our ticker summary of SOFR trades:

It has just hit me how much this “Trades” view looks like a consolidated tape, as wished for by MIFID II! Amazing what the market comes up with of its own accord when given unfettered access to the actual data….anyway, I digress.

In terms of SOFR trades today:

- We have seen only one SOFR Spreadover trade. This was actually a curve trade of spreadovers, 10y vs 30y. We mark it as SoS (“spread of spreads”) on the tape above.

- Recall that Spreadovers are the “bread and butter” of interdealer SEFs and account for up to 70% of interdealer SEF volumes. So we expect SOFR Spreadover volumes in particular to pick-up this afternoon as the US comes in.

- There has been one SOFR risk-management package already executed of 6 short-dated, relatively large notional swaps.

- Unfortunately, this package of SOFR swaps has made up the bulk of SOFR activity this morning.

In fact, if we look at only trades done in the London timezone today, I only see 6 SOFR trades since 7am. That is disappointing.

Compare this to LIBOR, where there have been 22 trades! Come on London USD Swap traders, time to flip the switch….

9:45am London Monday 26th July

Truth be told, this has slowed down A LOT. A lot more than I expected. Looks like it will be a long wait until we get the SOFR trade taking us over $1bn notional today. We are at $794m in SOFR notional vs $2,822m in LIBOR. Will we get to $1bn SOFR or $3bn LIBOR notional first today?

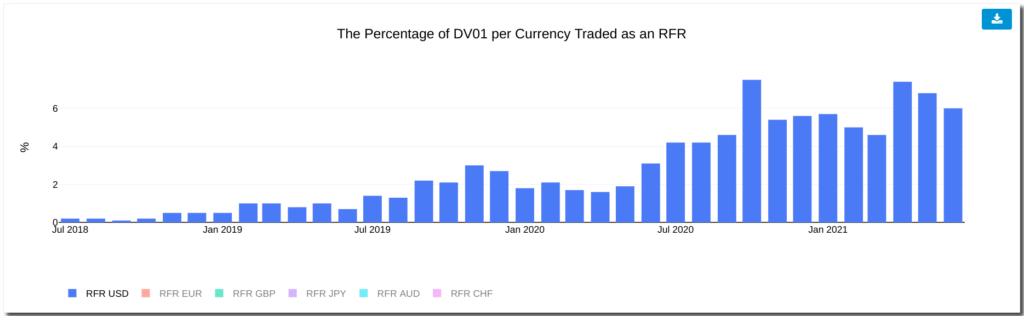

In terms of DV01 traded, our RFR Adoption Indicator for SOFR is tracking at 12% today. Up from the 6% last month, but not great:

This is all very reminiscent of the two SONIA days. It really is slow going trying to change what people trade.

10:15am London Monday 26th July

Well that didn’t take long! We are indeed over $3bn notional in LIBOR swaps traded now:

And SOFR has some catching up to overall, now at $920m notional traded:

Some recent highlights:

- 30Y SOFR has traded (again)! This time as part of a 10y-30y maturity switch (as opposed to a spread of spreadovers).

- 10y-20y-30y SOFR butterfly has traded. These types of packages are a positive sign that interbank markets are indeed beginning to trade more and more SOFR.

- There have been 6 spreadover trades in LIBOR land and only one in SOFR swaps.

And we just hit $991m in SOFR notional with a 10y-30y trade. The $1bn is close!

10:17am London Monday 26th July

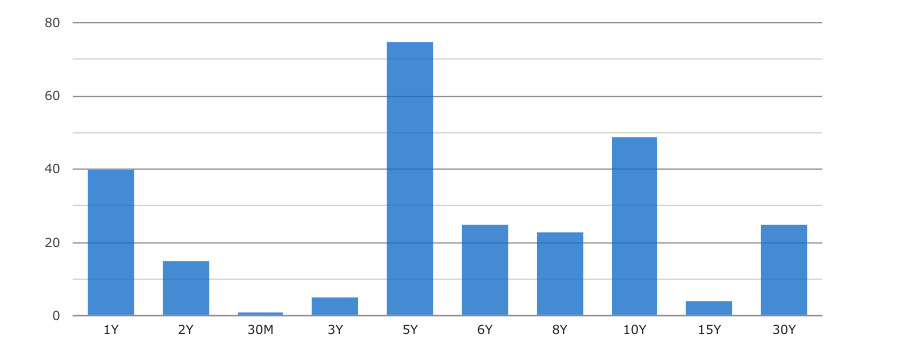

This chart of LIBOR activity today what would annoy me if I were a regulator looking at SOFR First. Why is there so much activity in LIBOR in standard tenors – 5y, 10y and 30y. Standardised tenors, standardised products should be the first to switch convention, not the last?

By the way, 22 out of 24 trades were executed on SEF today so far (92%). A great sign that markets would be fine with a Trading Obligation in SOFR markets?

12:30pm London Monday 26th July

After a brief interlude, let’s check in again where the SOFR market is now at.

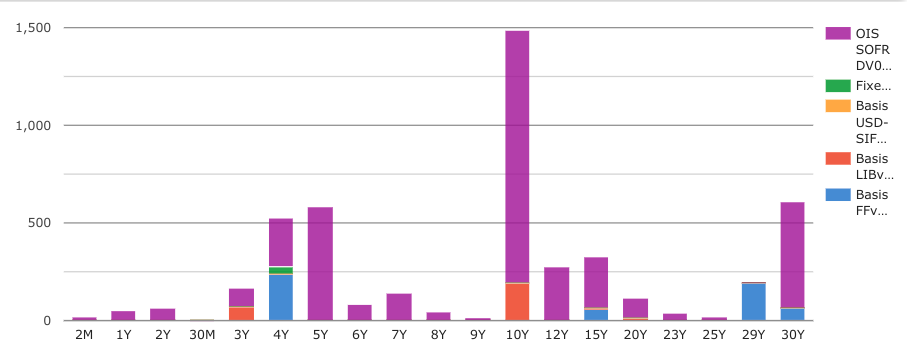

SOFR

- 43 trades

- $1,722m Notional

- $1,100k DV01

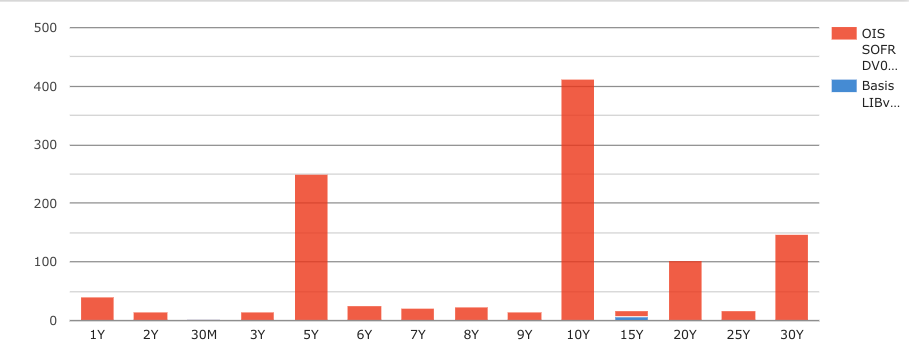

That is a nice pick up in activity in those two hours, roughly doubling the amount traded (both trades and notional). The chart below also show that we have just seen our first basis swap of the day too:

Checking in on LIBOR activity;

LIBOR

- 167 trades (!)

- $5,279m notional

- $3,352k DV01

That is a lot of LIBOR activity!

However, SOFR activity has really picked up a lot more. It now leaves our RFR Adoption Indicator at 25%, which would be an amazing end result if it can be maintained today.

Worth noting that we have indeed seen an increase in the SOFR Spreadover activity, with 9 trades so far today. They can be readily identified in SDRView Pro for our subscribers:

12:30pm London Monday 26th July

14:15pm London Monday 26th July

The SOFR Adoption Index today is still tracking at 27%! If we assume that half of the market is D2C, that means nearly 50% of IDB risk has been transacted versus SOFR. That is pretty good going for a single day!

SOFR

- 61 trades (seems low?)

- $2,800m Notional

- $2,004k DV01

LIBOR

- 246 trades

- $7,869m Notional

- $5,462k DV01

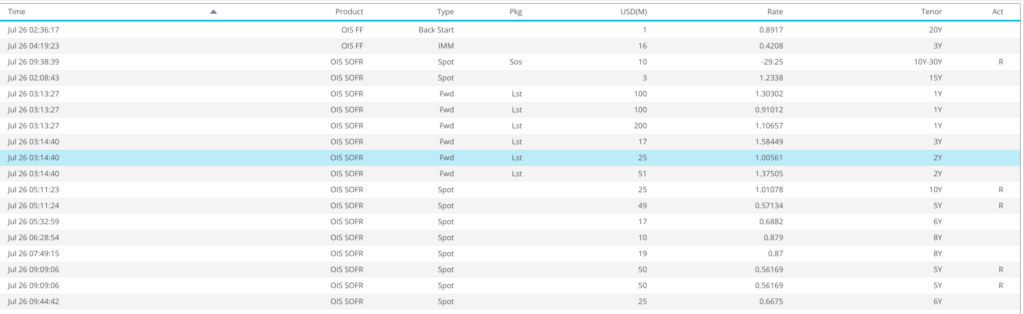

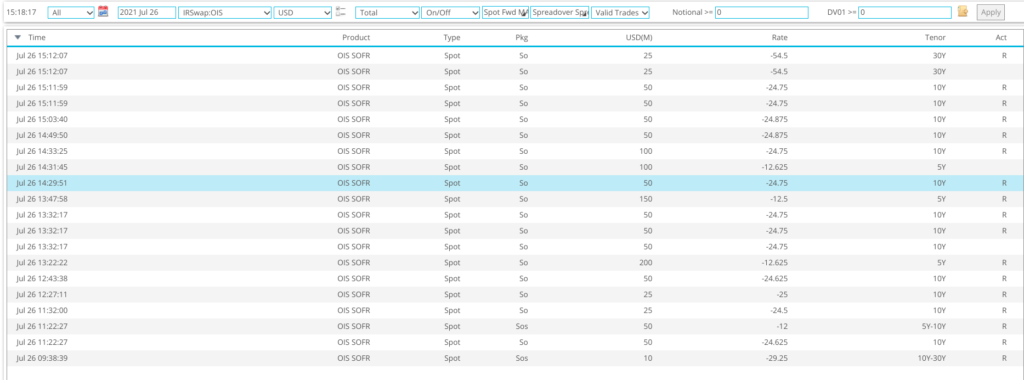

Trade list for SOFR activity so far today. First, 20 Spreadovers versus SOFR

And the other recent SOFR trades:

27% I think would be a great result if we end the day here!

3:25pm London Monday 26th July

I should have waited until New York time to write the intro to this blog! New York hours have seen a pick up in SOFR trading for sure. Estimating it in notional terms, and we have seen 30% of notional executed versus SOFR since 7am New York time.

At the moment, our DV01-derived SOFR Adoption Indicator for today is now tracking at 28% for the whole day.

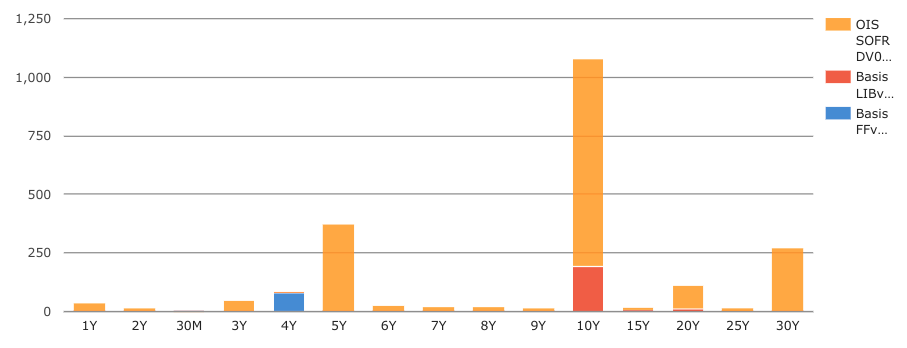

Our chart colours have changed as well as more and more different product types trade in SOFR:

The 30Y area of the curve still lags LIBOR products at the moment though….

6:45pm London Monday 26th July

Final scores for LIBOR and SOFR for today’s blog. I’m sure there will be lots more commentary soon. I think I would summarise it as a “good effort” and certainly one of the more successful days in the transition story.

RFR Adoption Indicator

18% of DV01 risk traded as SOFR today.

SOFR Activity

- 114 trades

- $7,726m Notional

- $4,702k DV01

LIBOR Activity

- 644 trades

- $40,420m Notional (!)

- $22,161k DV01

Most importantly, we saw sustained SOFR activity throughout the trading day. There was trading across the whole curve in a number of different products. Spreadovers versus SOFR can be considered particularly successful with 28 different trades. There were “only” 22 Spreadovers versus LIBOR.

Well done US markets, this feels like a good starting point. Of course, we now expect the market to get closer to 50% SOFR trading, but let’s celebrate the first small step.

8:00pm London Monday 26th July

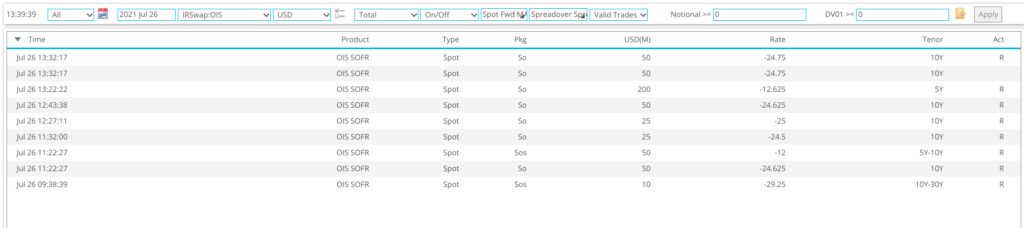

As a reminder we covered SOFR SpreadOvers are now starting to trade on June 16, 2021 and reported a small number os sporadic trades between 9th June and 16th June, so it is great to see that today we see:

- 23 SOFR Spreadover trades, On SEF and Cleared

- 2 of these where Curve Switches, one 5Y-10Y, the other 10Y-30Y

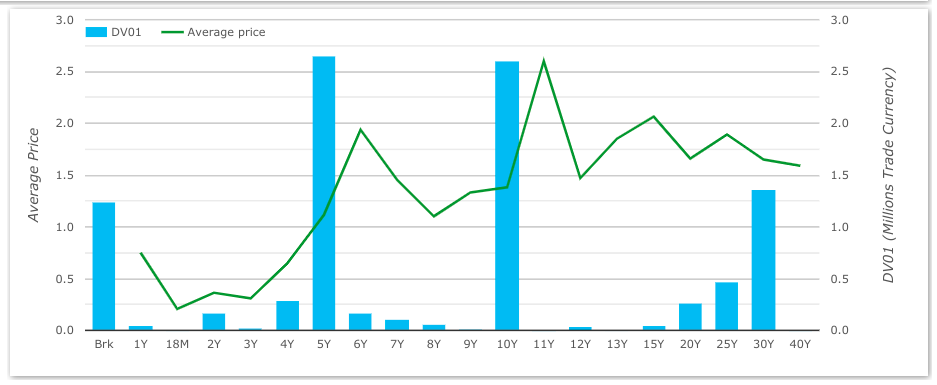

- 7 trades in 5Y, $850m notional, a last price of -12,5bps

- 14 trades in 10Y, $690m notional, a last price of -24.75bps

- 4 trades in 30Y, $85m notional, a last price of -54.25 bps

- An overall $1.6 billion gross notional or $1.3m DV01

Which compares favorably to Libor SpreadOvers with 20 trades of which 6 were curve switches and a total gross notional of $1.96 billion or $1.5m DV01.

It will be interesting to see if this roughly 50-50 split continues in the days ahead.

We will of-course continue to follow and analyse the data.