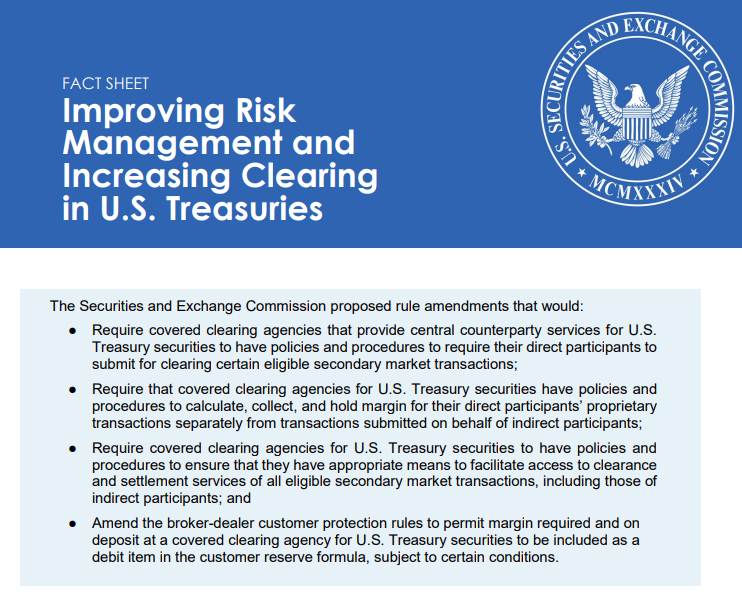

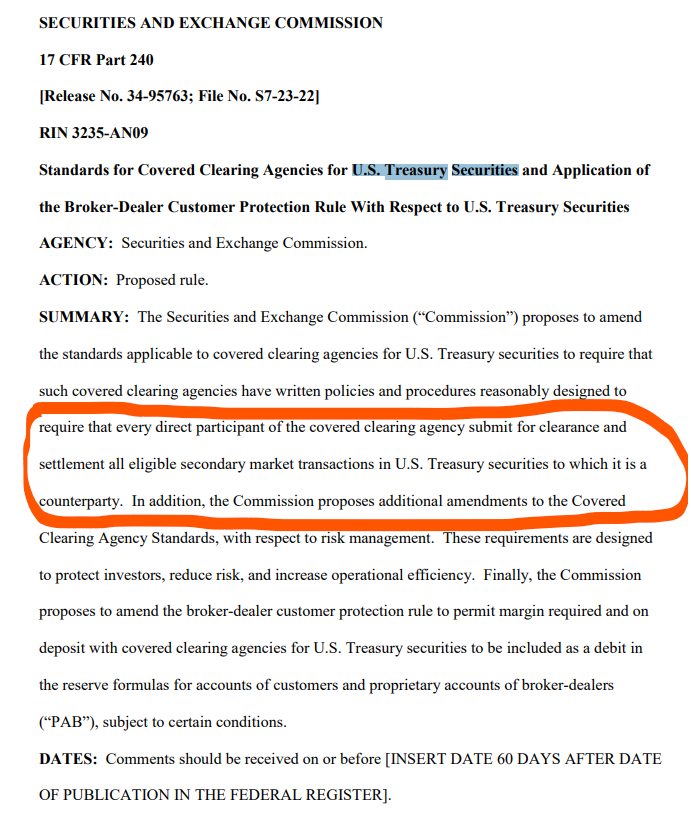

The SEC issued a proposal last year regarding a potential clearing mandate for cash treasuries and repos.

There is a good two-pager summary from the SEC here:

Or you can choose to read the entire proposal here:

Clearing of Cash, Repo and Swaps are all different

First of all, I think it is important to state:

- The Clarus blog has traditionally focused on clearing of interest rate, FX and credit OTC transactions. These are term transactions (longer than one month) that carry counterparty credit risk to maturity.

- “Clearing” of cash Treasuries is different because it is an exchange of cash for a security, and the CCP simply guarantees this exchange. It is more akin to getting rid of settlement risk (and standardising settlement times). Inserting a CCP into the middle of cash treasury trades allows more multilateral netting, reducing settlement risk and simplifying everything (but the CCP will require margin to act as guarantor for all this settlement risk).

- Clearing of Repo transactions sits somewhere in the middle. There is settlement risk both front and back on a repo, but also an element of counterparty risk for the (typically short-dated period) that the repo is held for. However, a repo is collateralised lending (borrowing), so there is an inherent degree of counterparty credit risk mitigation within the product itself. Clearing of repo is therefore more like the clearing we normally talk about, but still not completely comparable.

What Are People Saying?

Even amongst the readership on our blog there are likely to be a really diverse range of opinions on potential new clearing mandates. With this in mind, I thought I would go through all of the comments that were received by the SEC between September and December (and some recently!). That will give us a good flavour of where this proposed rule is heading (and allows the blog a different way of presenting regulatory change to our readers). Let us know what you think of this new approach in the comments below.

SEC Comments

The “Managed Funds Association” were one of the earliest industry bodies to submit their comments.

They provide a good overview of the proposed rules, along with their concerns. Their recommendations, in short, are;

- Expand availability of central clearing

- Implement a clearing mandate for bilateral repo transactions

- Eliminate the clearing mandate for cash market transactions

- Take a phased approach to implementation

(I paraphrase their Exec Summary, otherwise we would be here all day!). The MFA showed that there is a clear benefit in responding to the consultations early, because a) these recommendations are referenced in some of the other responses and b) they certainly influenced how I read the subsequent comments.

Below are 3 or 4 bullets on each of the 30+ other comments received. You will find some common themes!

- SIFMA and IIB:

- Increase clearing incentives and expand availability/remove barriers to clearing.

- Conduct further study particularly cost/benefit analysis of clearing.

- Targeted clearing requirement centred on IDBs.

- Leave Repos to voluntarily clear unless there is strong evidence a mandate is necessary.

- Phase-in implementation.

- Investment Company Institute

- Agree that investment funds should not be subject to a mandate for clearing of cash Treasury transactions.

- Think that investment fund activity done via an interdealer broker should also be exempt.

- Exempt funds from any mandate regarding repo.

- LSEG

- Support a clearing mandate (CB: I think we would have been shocked to read otherwise!)

- Believe they can “innovate” with the market to enable broader access to cleared repo.

- Their supplementary response then goes on to say that CCPs should be exempt from the clearing mandate (and give some good reasons as to why, however strange it sounds to write that CCPs support clearing mandates unless it is applied to their own operations!).

- SIFMA (Asset Management Group) (CB: this is the most “negative” response so far)

- Concerned it will increase costs and not create capacity (their emphasis, not mine).

- Perform thorough cost/benefit analysis.

- Incentivize clearing and promote alternatives to clearing.

- Robust clearing infrastructure required, including a minimum of two clearing agencies.

- Address the difference between cash and repo.

- Collateral segregation at CCPs.

- Phase-in and allow time to implement any changes.

- ASL Capital Markets

- “Trading in these markets (treasuries) is virtually all that we do”

- Incremental steps, not transformative, are required.

- May make initiating a business to trade USTs more costly.

- Better Markets

- “He touched the dead corpse of the public credit and it sprang upon its feet”. I knew Better Markets wouldn’t disappoint in their response!

- “Lack of transparency has hamstrung regulators.”

- Proposal will increase clearing of USTs – which is good.

- Will reduce risks in the market, so long as CCPs are prudently regulated.

- Improves regulatory oversight and transparency.

- PTFs now represent 50% of all trading on IDB platforms.

- Regulating PTFs as dealers will confer numerous benefits in terms of transparency, market stability, investor protection, and fair competition.

- FIA

- Concerned that the Rules will “disrupt significantly” the secondary market.

- FCMs receive significant amounts of Treasuries from end clients before transforming them into cash to post at CCPs. The FIA think these transactions should be exempt from any clearing mandate.

- In a supplementary filing, the FIA appear to have posted the data to back this up.

- ISDA

- ISDA did a survey! See here for the full results (whilst sparing a thought for Reg Affairs officers who then had to respond to both the ISDA survey and file an SEC comment).

- Survey respondents supported reforms to the leverage ratio (SLR), increased access to clearing, ability to post client collateral to CCPs, expansion of cross margining vs futures.

- CME (who owns BrokerTec)

- More clearing substantially reduces number of settlement fails (by up to 74%).

- Generally supportive of any regulatory initiatives that appropriately incentivize centralized clearing.

- Recognise that infrastructure changes are required, and advocate a phased approach.

- Concerns that others may try to narrow the scope of the clearing mandate, which could have deleterious effects on certain trading venues (e.g. BrokerTec).

- DCOs should be exempt from the clearing mandate (how strange that a CCP should argue that clearing isn’t suitable for them!). (Including an example whereby standardisation in clearing could be deleterious to a DCO in the event of a member default).

- Exempt physical delivery of Treasuries versus futures contracts (that is an interesting one!)

- DTCC (who own FICC, surely the biggest potential beneficiary of the rules?)

- Unsurprisingly, they are supportive!

- Citadel

- Any clearing requirement must capture a broad cross-section of the market (including all D2C trades). Market wide is their recommendation.

- Exclude forced bundling of execution and clearing services.

- Fair access for all (indirect client clearing model).

- Do not expand the definition of a dealer.

- Lots of Firms (ARB, Citadel Sec, DRW, Geneva, IMC, Jump, Optiver among others)

- “We are not aware of a market-wide transition to central clearing occurring in any asset class without a clearing mandate.”

- Efficient transition of liquidity, availability of client clearing, resolving hurdles will allow market to realise the benefits of central clearing.

- Clearing mandate should be market-wide; client clearing availability.

- GTS

- Central clearing will lead to more efficient, resilient and liquid Treasury markets .

- No major participant has dropped out of the swaps market as a result of the clearing mandate.

- In Swaps there was a dual mandate to clear – i.e. the uncleared margin rules were also effective.

- Mandate should be comprehensive and help foster all-to-all trading.

- Support phased implementation.

- Treasuries the only uncleared market out of the 3 Rates liquidity centres – futures, swaps, cash.

- ICE

- Clearing has increased market liquidity and transparency in other markets – will do the same in cash and repo.

- Important to have competition across multiple clearing agencies (i.e. it shouldn’t just be FICC clearing Treasuries).

- Supportive of margin segregation as it works in other markets already.

- Should be up to Clearing Agencies which access models they develop as per the needs of the market.

- Clearing Agencies should not be mandated to return excess margin within one day – that is not how other markets work.

- Tradeweb

- Is the infrastructure in place at FICC to cater for the large increase in anticipated transactions? Do they have an appropriate plan to expand access models for certain market participants?

- Should encourage electronic multilateral trading.

- Clearing mandate should increase dealer capacity.

- IDTA

- The Treasury market is not the swaps market pre-Dodd Frank.

- Supporting central clearing in principal (sic) cannot be the basis for imposing a mandate.

- Costs: bilateral trade via BONY/Fedwire costs $3, FICC charge $7 (CB: why did no other responses use data like this?).

In Summary

There are some common threads throughout the responses. In order of frequency:

- Phased approach is necessary. All respondents alluded to the fact that change is hard. To be fair, all respondents are incumbents in the market so this is not a huge surprise to hear people arguing against change.

- The end goal should be a market-wide clearing mandate to really “juice-up” the benefits of multilateral netting (albeit with certain exceptions, including the CCPs arguing they should be exempt!). This is influenced by the sheer number of PTFs and CCPs who have submitted responses.

- Perform a proper cost-benefit analysis before making any changes (this came from a few places but no one actually delivered data/a cost-benefit on their own portfolio). This is mainly the call from “end-users”, investment funds etc. (who are maybe concerned that their directional positions will lead to large margin requirements).

- There do appear to be frequent concerns over whether FICC can really handle a wider-range of customers or appropriately handle new access methods (this seems to be across the board, not sure if these same concerns were raised regarding CME/ICE/LCH during Dodd-Frank?).

Expect to hear much more on this topic over the coming months.