Earlier in April, ICE began clearing single name CDS on a larger number of banks. ICE has been clearing single names on various financial companies & banks for a while, but what makes this unique is that they have added swaps on their own clearing members.

The correct terminology is “Clearing Participant CDS” or just “CP CDS” for short.

So, now you can clear that single name exposure you have to Deutsche Bank, etc.

Presumably this is driven at least in part by the Uncleared Margin Rules.

I wanted to check to see how this was going.

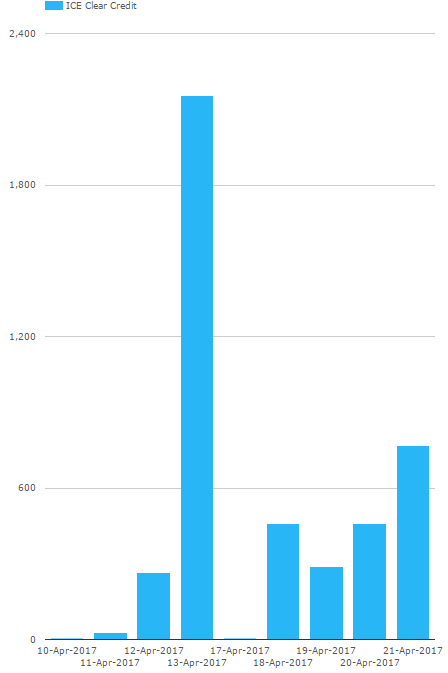

DATA

ICE began the enhanced service on April 10, 2017. Here are daily volumes for CP CDS contracts, extracted by CCPView:

The data looks a bit ad-hoc, I presume we’re very much in the early days of this, and the spike we see is due to some backloading activity.

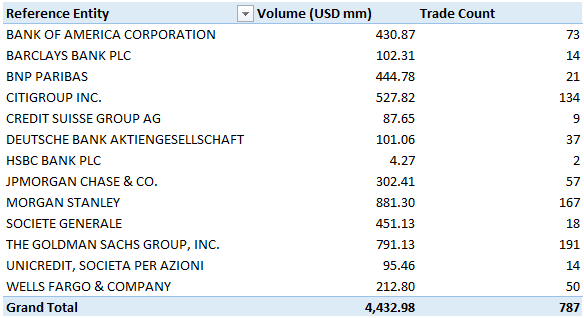

If I drill into the data, we can see the activity by Clearing Participant (Reference Entity):

A couple useful nuggets of information:

- We see both US and European names (all cleared by ICE Clear Credit, but in USD or EUR respectively)

- Morgan Stanley and Goldman Sachs the most active so far

- The average trade size works out to just over 5 million USD equivalent. This seemed small to me.

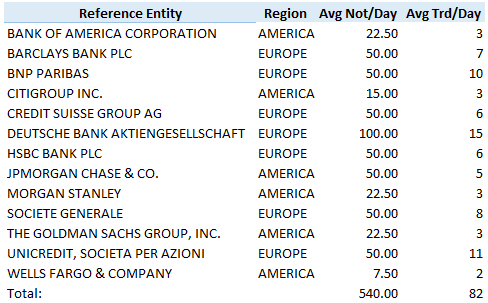

So I turned to the TIW data set, which I always find a bit difficult to navigate and interpret. I pulled their report of the top 100 single names traded from Dec 2016 – Mar 2017, so before ICE began clearing these names. Manipulating that in Excel:

Presumably this is total activity in these names. Which tells me:

- Average trade size has indeed been on the order of 6 million USD equivalent in the previous uncleared space

- These names are not terribly active in non-crisis situations. 82 trades per day on average, spread across the 13 names I chose

- Almost seems like the extent of single name financial trading might be done only by the banks that actively manage CVA.

WRINKLES?

So, as I said in the intro, you can now clear that single name exposure you have to Deutsche Bank and others. Of course, to avoid any wrong-way risk, you probably shouldn’t clear that trade with Deutsche Bank (I believe they still clear in OTC in Europe).

This raised a couple questions in my mind regarding wrong-way-risk:

- How do you keep someone from buying/selling protection on their own name

- What happens in default when a member has to bid on a portfolio that contains their own name

I did some digging and was surprised that the regulatory filings did not seem to make any explicit changes to rules to cater for this. I presume it must be a case of “know your broker”. If you want to read it yourself, the SEC filing is here.

SUMMARY

That’s it for today. Short on time, but I think we can see the jist of it:

- ICE has added clearing of CDS on members’ names

- Activity seems to be roughly as active as in the bilateral space

- Trade sizes seem relatively small, probably born from CVA exposures

And of course, we need to add “CP CDS” to the inside-baseball lexicon of OTC derivatives.