Following on from the first ESG blog on the Clarus website, see ESG Investments, our second ESG blog takes a look at the Climate Risk Disclosures of major UK Banks.

Combining many factors into a single score or rating, which can then be optimized is a common approach in Finance. While we do not want to neglect the S & G from ESG, the E and in particular Climate change is a high profile area with a lot of current research and analysis.

However, as with Finance, standardisation is a vital consideration. Can one disclosure be accurately compared to another? Now that the disclosures themselves are being published, let’s try to make sense of them.

Background

Banks are starting to evaluate assets and lending activity taking into account climate risk and it is likely that new risk factors covering climate risk will end up being incorporated into risk management and possibly even regulatory capital calculations.

Many Banks have started to publish voluntary disclosures on climate risk and in the future stress testing exercises may become standardized.

Climate stress testing and scenario analysis

Even if they will not be enforced by regulators, stress testing and scenario analysis may well be the only useful risk tools given the long time horizon of climate impact.

Climate change scenarios typically consider 2 different types of risk:

- One is transition risk, the uncertainty due to events including energy related policies, new technologies, consumer preferences, all interacting with predictions of carbon prices and emissions.

- The other one is physical risk e.g. the probability and impact of floods and hurricanes. This is difficult to model in a local, granular way and requires borrowing techniques from the insurance world.

The challenges compared to looking at the ESG ratings or current carbon emissions of companies should be obvious. These scenarios consider the evolution of an interconnected system, which involves modelling supply-demand curves, consumer behaviour and weather patterns well into the future.

Quite a leap from the analytics most bankers are familiar with.

A quick look at bank disclosures

UK regulators were quick to impose timelines for climate stress testing so this naturally led to more detailed disclosures from British banks.

To generalise a bit, here is what you can find in a typical disclosure:

- Current metrics and ratings as well as exposures of the bank, with detailed plans to reduce emissions e.g. via reducing business with clients dependent on coal

- Impact of climate change on individual assets, given the high-level scenarios by the Central Bank network NGFS which define carbon prices and global warming patterns

And what you can’t find:

- A complete list of assumptions for the calculations – this is perhaps not fair to ask but would be extremely useful, as it is rare to imply anything from the market or historical data in the models

- Sensitivity analysis – most banks integrate third party models via vendors and consultancies, so it is hard to guess the impact of parameter changes

Going too deep into each document is not practical, so let’s pick one theme from each bank.

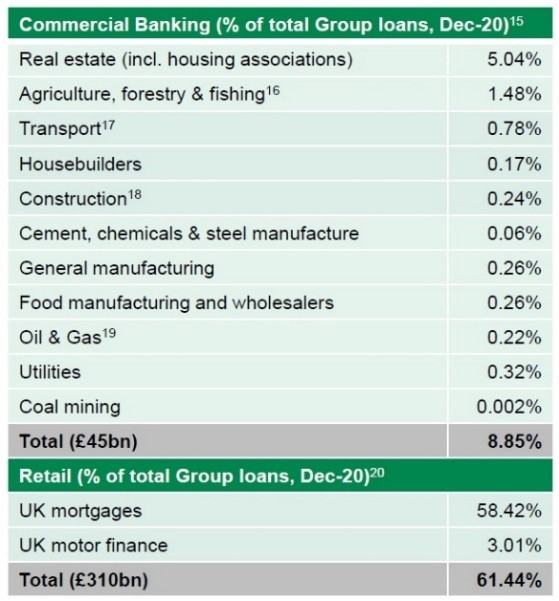

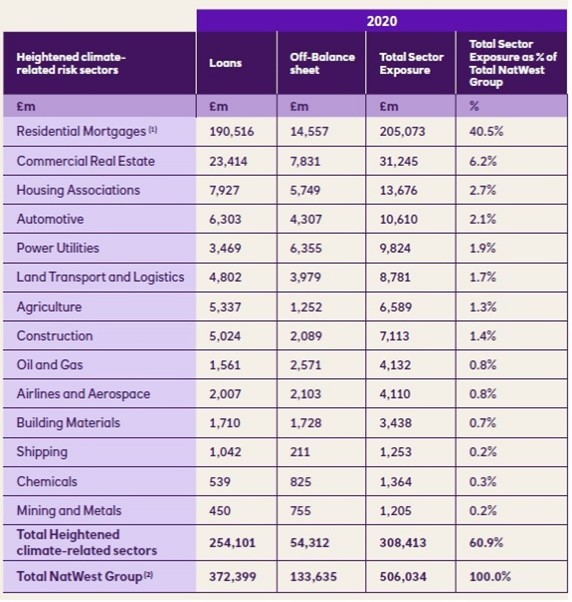

Lloyds and NatWest

I found these two tables below at Lloyds and NatWest disclosures, not surprisingly they are not 100 percent comparable, but we can still get interesting insights.

NatWest very transparently explains that in their scenarios they assume every other bank has NatWest’s exposure profile. This kind of assumption is probably inevitable, one needs to consider the indirect impacts: what if your bank has an exposure to another bank specialised in climate sensitive sectors?

In this specific case NatWest has a higher exposure to transport, construction, oil & gas and utilities, so the above assumption could be a conservative one. Lloyds has more mortgage exposure, but as the physical risk like floods are local, it is not possible to say much looking at total numbers.

Source: Lloyds ESG Investor Presentation 2021

Source: NatWest Climate-Related Disclosures Report 2020

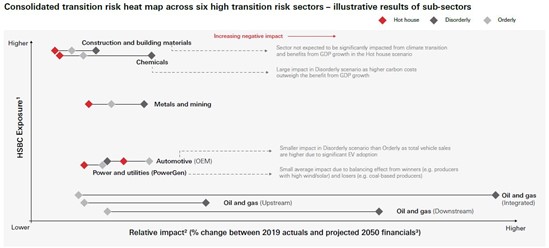

HSBC

HSBC’s disclosure does not cover too much methodology detail, but it probably has the best visual to show exposures and scenario impact in one place.

Here Hot House refers to a business-as-usual scenario with low transition risk but high physical risk, whereas Disorderly and Orderly have low physical risk but high and low transition risk respectively. More info on these scenarios can be found in this NGFS publication.

HSBC has a high exposure to construction and chemicals, but the tail risk seems to be in oil & gas.

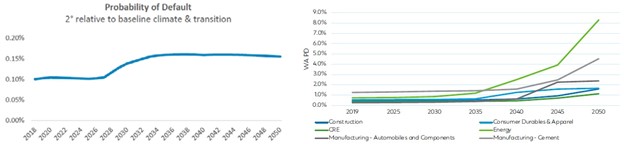

Standard Chartered

Given Standard Chartered is a major player in emerging markets, their climate sensitive lending policy should be of interest to many analysts.

They also cover another important aspect better than most: how does climate change impact corporate default risk? The answer is, it depends.

In the graph on the left below, the transition risk impact on the client’s default probability is small, thanks to a reliance on nuclear and hydro energy sources.

The second graph shows that on average the impact is more dramatic with varying timings for different sectors. The thresholds causing the peaks are highly dependent on carbon prices.

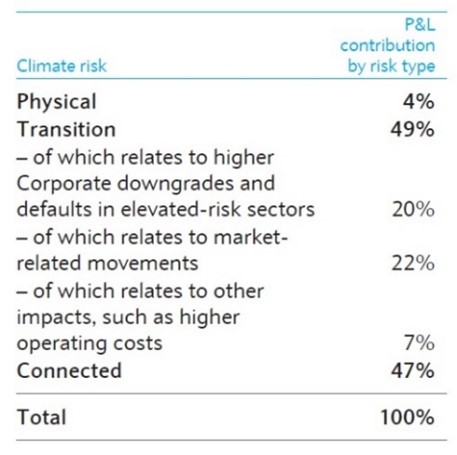

Barclays

I picked up an earlier publication from Barclays as it has a rare discussion of how different types of risk compare against each other with a proper P&L contribution breakdown.

The small contribution of physical risk in the below table may be surprising. This is a clear example of a mismatch between: a) long time horizon of global warming vs. b) Barclays’ current portfolio duration. UK regulatory stress testing will omit traded risk as per the latest update, so these contributions could change significantly.

Barclays also takes into account connected risk: the secondary impact of the physical and transition risk related losses causing a subsequent recession. It is interesting to see an attempt at modelling systemic risk and it does have a material impact, comparable to transition risk itself.

Final thoughts

A drilldown into ‘E’ in ESG opens the Pandora’s box. Standardisation is badly needed to allow for any meaningful comparisons. Similar to how BIS have helped cement standardised risk management models in finance, we need similar standards in the ESG space so that comparisons across firms can be made. Anyone want to suggest a standardised schema?

The good news is that we are starting to see more transparency from the banks on their climate risk methodologies. Bank disclosures may help in the collective modelling effort and could give increasingly valuable insights to outside observers.

One might even contemplate that banks will share the scenario analysis tools with the buy-side and perhaps everybody else one day. So we can all keep making our assumptions but at least with a common language.

This article is authored by Onur Cetin.