Last week, CME announced it would end it’s clearing offering for Credit Default Swaps, and instead focus it’s effort on other innovations in clearing services for Interest Rate and FX, including:

- FX Options launched by 2017 year end

- Interest Rate swaps for 3 more currencies – CNY, CLP, and COP by early 2018

- Further capital efficiencies within listed & OTC products

The presumption here is that the incumbent CDS clearing house (ICE) is just too competitive. So I thought it appropriate to evaluate the CDS clearing space.

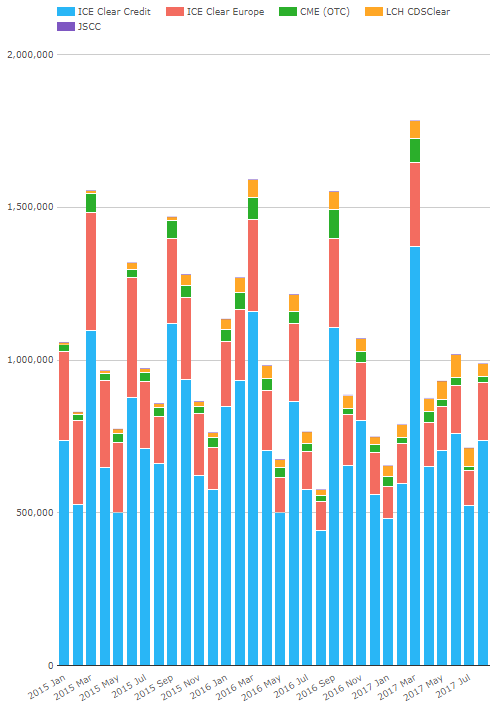

Headline Clearing Data

To start with, let’s look at monthly notional cleared volumes across all CDS. This include both single name and indices, per month, since Jan 2015:

This shows just over $1 trn of notional cleared every month across the globe. If we break this down to percentage terms, we can see:

So pretty clear that the ICE clearing houses dominate clearing of CDS. In fact, my general rule of thumb when explaining CDS clearing has been:

- CME clears in 1 day what JSCC clears in 1 month

- ICE clears in 1 day what CME clears in 1 month

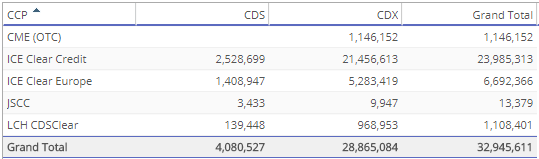

Breaking Down the Numbers

If we’re wondering about how much single-name comprises here:

It’s clear that the vast majority of CDS clearing is CDS Index. (Our terminology CDX is CDS Index, and CDS is Single Name). Also worth noting that CME never did have any Single Name business.

Lastly, if we look at just CDS Indices:

It shows that ICE dominates the business in all of the major indices (IG, HY, EM, and iTraxx Europe). The only non-competitive space looks like iTraxx Japan, which is only cleared by JSCC. But 100% of a small number is still a small number!

More Currencies for CME

Final thing to mention is CME’s strategic initiative to focus on more IRS and FX. We know about their upcoming FX Options clearing, so I wanted to check on their more recently launched currencies (MXN & BRL):

Showing that:

- CME has a decent portion of USD IRS

- However lags behind other incumbent LCH in other most other currencies

- JSCC handles most of the JPY

- ASX handles nearly 1/3rd of AUD

- CME has had a tremendous amount of success in MXN and BRL

So it seems plausible that extending rates clearing into CNY, COP and CLP could strengthen their reach.

Summary

The data generally corroborates the notions:

- ICE is dominant in CDS clearing

- CME has been successful in launching more exotic IRS currencies

So the move completely makes sense. We’ll be back when CME launch more currencies, and of course when they launch FX Options.