One of the better known / worst kept secrets in the OTC markets these days is that the largest clearing houses are planning to clear FX Options.

Details on this are very thin. LCH have made a couple announcements over the years with respect to clearing options, and if you look hard enough on the CME website, you will find a 1 pager here on their plans in this space.

Any details are still hard to find. However for CME, the plan seems to be:

- EURUSD, GBPUSD, USDJPY, AUDUSD, USDCHF, USDCAD, and EURGBP

- European style

- Cash Settled

- Some time in 2017

That is about everything one can glean online about FX Options clearing. So I thought I’d explore the data and see what I could find.

HOW BIG IS THE MARKET

Let’s start by looking at what the SDR data in America says about the size of this market.

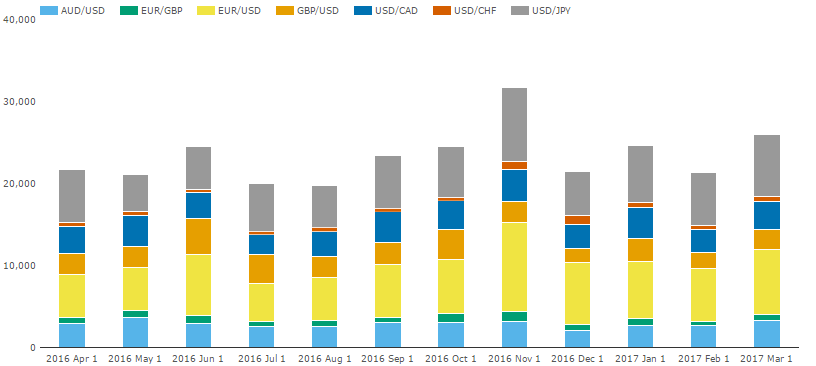

Selecting the 7 proposed ccypairs over the past year, and only vanilla options, we can see monthly trade counts as high as 31,700 in November 2016. For any one ccypair, that same month saw nearly 11,000 EURUSD options:

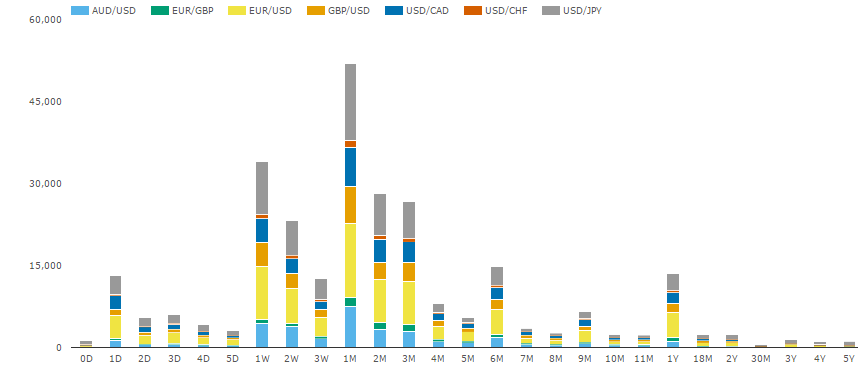

I also pulled notional data from SDRView, and lastly, wanted to get an idea of typical maturities:

From all of this data gathering, we can glean a rough idea of headline metrics for these 7 currency pairs:

- Average trade size is about 30 million USD. This ranges from just under $20 million for AUDUSD, and up to nearly $40 million for USDJPY.

- Roughly 1,200 Vanilla FX Options are traded per day (In America and reported to SDRs). So about 36 billion USD notional per day.

- Most typically traded maturity is a 1 month option, but the standard pillars of 1W, 2W, 2M and 3M also stand out. I was a bit surprised to see nearly 15,000 1-day options traded.

- Roughly 35% of trade activity is reported as ON-SEF.

On the surface, this seems encouraging for options clearing. A possible market of 1,200 trades per day compares nicely with the roughly 2,000+ cleared IRD trades seen on SDR per day.

Note that if I expand my criteria to include all currency pairs, USDMXN seems to have roughly the same activity as AUDUSD. I wonder why CME has left MXN out of the first pass?

MORE SANITY CHECKS

We need to do a few more sanity checks when sizing this market. First, CME only plans to clear European style options. And second, they only plan to clear cash settled. The latter is somewhat intriguing as I had worked in the FX Options industry for 10 years, and don’t think I was ever privy to a cash settled option being traded!

So I examined an arbitrary week of data (5,815 trades) across these 7 currency pairs and discovered:

- Only 42 (<1%) were “AM” – American Style Options. However there were also 56 trades labeled as “AS”. I can’t say I know what “AS” means – perhaps a Bermudan or Canary style option? Or another acronym for American Style? Either way, I am comfortable that European options account for the lions share ~99%.

- I can only find 12 options that have a settlement currency denoted. If you trust the SDR data, this might mean that there were only 12 cash-settled options traded.

So, on the bright side, European Vanilla options in the US represent nearly 1,200 trades per day. On the down side, only 1 or 2 of these appear to be cash settled. I double-checked to make sure there were no deliverable pairs (eg EURUSD, USDJPY etc) reported as Non-Deliverable-Options (NDO’s).

CASH SETTLING

So the market is almost totally a deliverable market. This makes sense – the long-standing issue with clearing FX Options had been how to mitigate the settlement risk of the delivery. Just take any one of our “typical” trades – when it comes to maturity, one bank has to deliver 30 million USD and await payment of say 25 million EUR. The large institutions in the FX market have used CLS to handle FX settlement since 2002, which in simplest terms, guarantees that the exchange of payments happens simultaneously (PvP) so you don’t get stuck waiting for your 25 million Euros to show up. If you don’t use CLS, it’s hard to feel comfortable with the settlement risk involved.

The CME approach appears to skip the settlement risk by going cash settlement, and LCH seem to embrace it with their CLS partnership.

I would surmise that CME’s target market for FX Options clearing is for clients that don’t necessarily use CLS for settlement to begin with.

We should also acknowledge, that while the data tells us that cash-settled FX Options do not trade actively, it doesn’t mean that all participants take their positions to maturity. There is certainly a practice of firms closing out options positions before maturity, whether it is the client who wants to unwind, or even the dealer who wants to mitigate their pin risk.

Speaking of pin risk – cash settling should be able to help everyone gain certainty. Quick tutorial on PIN risk – assume you have sold a 1.1000 call option on EURUSD, and it’s a “NY Cut” meaning it expires at 10am ET. At 9:59am and the market trading at 1.1000, you really want to know if your counterparty will be taking delivery or not, as you need to know your position in order to hedge or not hedge. If you find out at 10:05 that he took delivery and the market is now 1.1100, you’ve just lost a big figure.

Point here is that cash settlement would presumably give immediate certainty to everyone with a position that their trades have either expired or exercised.

On the flip side, we would need to acknowledge three things:

- Some firms may actually want/require delivery. Hence they’d need to then execute an FX trade after expiration

- Cash settling requires a Fixing price. The term “Fixing Price” is not typically involved in positive news headlines these days.

- A central counterpary could / should be a good solution for all option sellers, even for deliverable options, as there would be one point of contact (the CCP) for immediate information on whether the counterparty has exercised or not.

MARGIN BENEFITS

So the market seems large enough, and cash settling could have its own benefits. Surely, we should also expect some benefits of margining.

Let’s be clear though:

- All OTC FX Options are bilateral today

- Only phase 1 UMR banks are having to exchange Initial margin on FX Options

- A large number clients will be coming from a prime-brokerage-like world where their FX Options are margined in aggregate (alongside cash FX and other products).

So it’s hard to say if extracting options out of their existing arrangements and throwing them into a cleared environment would be margin additive or reducing. It all depends on the starting point (margined or not margined) and how much portfolio offsets they are currently enjoying.

But I can’t help myself from throwing some options into the SIMM calculator as a rough estimate to see what numbers we might be talking about. I packaged up 3 different options, spread individually across 3 separate counterparties. The options are:

- ~30mm USD notional

- 1-month

- Near-the money options

- Calls on EURUSD, USDJPY, and USDCAD

Calling the the SIMM Microservice with a CRIF file containing the related sensitivities for these trades:

import clarus

my_CRIF = open('./CRIF.csv').read()

result = clarus.simm.margin(portfolios=my_CRIF)

print (result)

I get the required SIMM margin per counterparty:

SIMM Account Change Margin EURUSD Bank 2400073 0 2400073 USDCAD Bank 1960762 0 1960762 USDJPY Bank 2071943 0 2071943 Margin 6432778 0 6432778

Worth pointing out that the differences in margin for each similar-sized option are presumably due to the different levels of volatility in each pair. EURUSD 1M vol is ~13%, USDJPY ~12%, and I chose USDCAD as that hovers around 7% vol.

If I now novate all of these to a single counterparty (CME or LCH), we can see a vast reduction. Again this is SIMM margin, perhaps to illustrate what we might expect at the upper end at a clearing house:

SIMM Account Change Margin Single CCP 3800245 0 3800245 Margin 3800245 0 3800245

So, we go from 6.4 mm+ USD in margin to under 4mm. Of course, this is a terribly simple example, as we only have 2 USD calls and 1 USD put. But illustrates both the scale of margins for FX Options under SIMM (roughly 7% of notional for 1m ATM), as well as the easy reduction from just putting your eggs in one basket: the answer to minimizing margins begins with reducing the number of counterparties.

SUMMARY

The LCH have planned FX Options clearing for some time, and the CME website claims that FX Option clearing will happen this year. A quick look at the data shows that the market is certainly large enough. We might, however, question how many cash settled options are traded at the moment, as well as the appetite within the market to cash settle their options instead of taking delivery. At the same time, we acknowledge some efficiencies could exist if cash settlement was more readily available.

Margining of FX Options is somewhat unclear at the moment, as neither CME or LCH have disclosed any samples on this. However, using SIMM margins as an estimate, we can see that the amounts are significant, and that while clearing may not reduce the IM on any individual trade (we dont know), we can say for certain that a reduction in the number of counterparties will certainly reduce the costs of margin.

We’ll stay on top of the story as options clearing unfolds over the course of the year.