Clearing Houses 2Q 2019 CPMI-IOSCO Quantitative Disclosures are now available, so lets look at what the data shows, similar to my CCP Disclosures 1Q 2019 article. Summary:

- Initial Margin for IRS is up 11% in the quarter and 18% in a year

- IM for CDS and ETD was flat in the quarter and up 12% in a year

- LCH SwapClear the largest increase in amount of IM

- Eurex OTC IRS and SGX-DC the largest in percentage terms

- A few CCPs increased their Default Resources; ATHEXClear, BME, CC&G Bonds, CC&G Securities

- OCC drastically reduced the number of failures affecting its clearing system

- We have recently added: CFFEX, ICE NGX, MGEX, OMIClear, TAIFEX.

Background

Under the voluntary CPMI-IOSCO Public Quantitative Disclosures, CCPs publish over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing and more.

CCPView has more than 3 years of these quarterly disclosures for thirty-five Clearing Houses, each with multiple Clearing Services, covering the period from 30 Sep 2015 to 30 Jun 2019. This disclosure data provides insights into trends over time at one CCP and comparisons between CCPs.

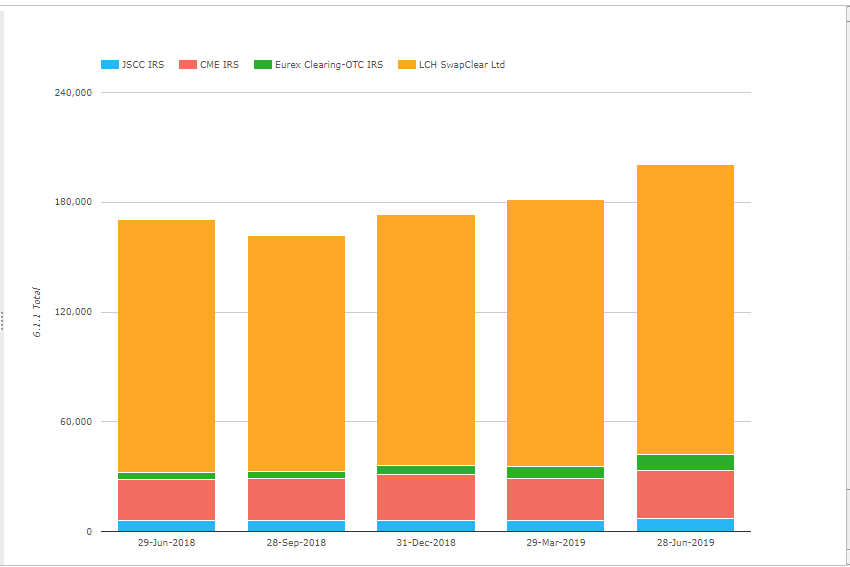

Initial Margin for IRS

- Total IM for these four CCPs was $201 billion on 28-Mar-2019, up $30.5 billion or 18% from a year earlier (YoY) and up $19.5 billion or 11% from a quarter earlier (QoQ)

- LCH SwapClear the largest with $159 billion of Initial margin, up $13 billion or 9% from the prior quarter (QoQ) and up $21 billion or 15% YoY.

- CME IRS next with $26.4 billion, up $3.5 billion or 15% QoQ and up $3.9 billion or 17% YoY.

- Eurex OTC IRS next with $8.7 billion, up $2.2 billion or 34% QoQ and up $5 billion or 142% YoY, significantly increasing from the prior quarter trends of $1.5 billion or 30% QoQ and $3 billion or 87% YoY.

- JSCC IRS with $6.8 billion, up $700 million or 11% QoQ and up $675 million or 11% YoY

Total IM increased by the largest amount in a quarter that we have see for some time, with LCH SwapClear showing the largest absolute increase in IM over the year and Eurex with the largest percentage increase. Eurex increasing it’s gap over JSCC after exceeding it’s IM for the first time in 1Q 2019.

New feature

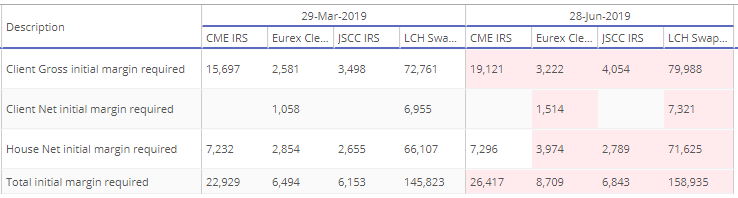

We have recently introduced a new feature in CCPView, one that allows our users to quickly see those disclosures that have changed more than a specified percentage from their historical range. Running this at 5% for the IRS IM required disclosures above shows:

Red highlights Up, Green highlights Down by > 5%

Lots of increases in the latest quarter, only one cell not up > 5%.

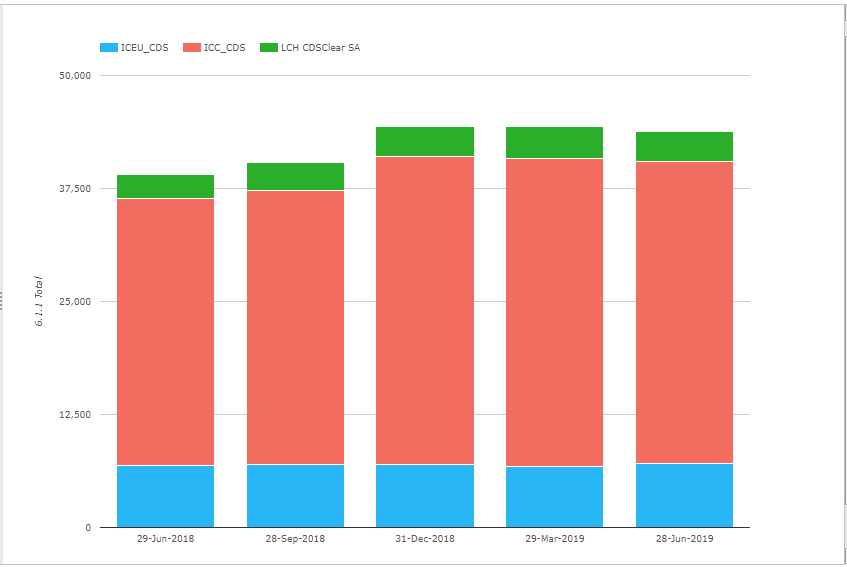

Initial Margin for CDS

- Total IM for these CCPs was $43.8 billion on 28-Mar-2019, down 1% QoQ and up $4.7 billion or 12% YoY

- ICE Credit Clear by far the largest at $33.4 billion, down $600 million QoQ and up $4 billion or 13% YoY.

- ICE Europe Credit next with $7.1 billion, up $360 million or 5% QoQ and up $200 million or 3% YoY.

- LCH CDSClear with $3.25 billion, down $300 million or -9% QoQ and up $560 million or 21% YoY.

CDS with no growth in 2Q19, but a strong 4Q18 means YoY growth is a decent 12%.

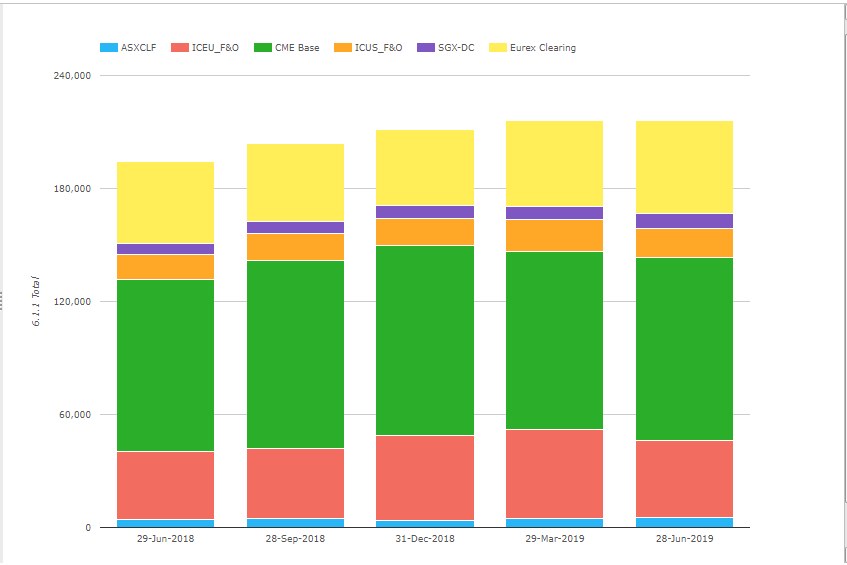

Initial Margin for ETD

- Total IM for these CCPs was $216 billion on 28-Jun-2019, flat QoQ but up $21.8 billion or 11% in a year

- CME Base is the largest with $97 billion, up $2.6b or 3% QoQ but down $2.6b or 3% YOY.

- Eurex is next, after two quarters in 3rd, with $49 billion, up $3b or 6% QoQ and up $5.5b or 13% YOY.

- ICE Europe F&O with $41 billion, down $6b or 13% QoQ and up $5.3b or 15% YOY.

- ICE US F&O $15 billion, down $1.6b or 9% QoQ and up $1.9b or 14% YOY.

- SGX-DC $8.4 billion, up $1.4b or 21% QoQ and $2.9b or 52% YoY

- ASX CLF $5.15 billion, up $170m or 3% QoQ and up $760m or 17% YoY

SGX-DC standing out with much higher growth rates QoQ and YOY than the others, while Eurex returns to second and both ICE Europe and ICE US down QoQ.

Other Disclosures of Interest

There are lots of disclosures for clearing houses and other measures such as margin, default fund, credit risk, liquidity, margin models, back-testing and more; let’s highlight a few from the many CCPs we cover:

- ASX CLF – Maximum total variation margin paid to the CCP on any business day (6.7.1) is at a new 1-year high of $1.3 billion, the previous high $900 million in 4Q 2018.

- ATHEXClear – Securities, which we recently added, shows Prefunded Aggregate Participants Contributions required (4.1.4) have increased to Eur 18 million from Eur 8 million

- B3 – Maximum aggregate initial margin call on any given business day over the period (6.8.1) was $2.2 billion, much higher than prior quarters with $1.1b, $1b, $1.1b and $1.6b.

- BME – Financial Derivatives shows Prefunded Aggregate Participants Contributions required (4.1.4) have increased to Eur 374 million from Eur 242 million

- CC&G Bond – Prefunded Aggregate Participants Contributions required (4.1.4) have increased to Eur 5.5 billion from Eur 4.9 billion and the Estimated largest aggregate stress loss in excess of initial margin caused by the default of any two participants (4.4.7 Peak day Average) is Eur 4.45 billion, significantly up from Eur 3.5 billion.

- CC&G Equities – Prefunded – Aggregate Participants Contributions – Required (4.1.4) have doubled to Eur 2.7 billion from Eur 1.3 billion and the Estimated largest aggregate stress loss in excess of initial margin caused by the default of any two participants (4.4.7 Peak day Average) is Eur 2 billion, up from Eur 1.6 billion.

- CDCC – House Net Initial Margin required (6.1.1) is $2.2 billion, significantly up from the $1.5 billion at the prior quarter end

- CFFEX – China Financial Futures Exchange has Total Initial margin required (6.1.1) of $7.9 billion

- DTCC GSD – the maximum total variation margin paid to the CCP on any given day (6.7.1) is $6.1 billion, up from $4.7b, $3b, $2.1b, $2.5b in prior quarters and the maximum aggregate initial margin call on any given business day (6.8.1) was $2.5 billion, higher than the $1.95 billion in the prior quarter

- DTCC MBSD – the actual largest intra-day and multi-day payment obligation of a single participant over the past 12 months (7.3.4) was $43.6 billion up from $32.8b, $24b, $25b & $14.5b in prior quarters! Mind you this compares to DTCC GSD (Government Bonds as opposed to Mortgage) with the same measure showing $74.8 billion, a large number indeed!

- OCC – Total number of failures affecting core clearing systems over the previous 12 months (17.3.1) is down to just 1, while prior quarter ends show 72, 81, 55, & 47 – so that is some improvement!

I could go on but after jumping from D to O, there are so many more clearing services to delve into. The current list is now:

- ASX, ATHEXClear, B3, BME, CCG, CCIL, CCP Austria, CDCC, CFFEX, CME, DTCC, EUREX, EuroCCP, HKEX, ICE Clear Credit, ICE Clear Europe, ICE Clear US, ICE NGX, JSCC, KDPW, Keler, LCH LTC, LCH SA, LME, MGEX, Nasdaq, NCC, Nodal, OCC, OMIClear, SCH, SGX, SIX, TAIFEX, TFX.

Surely there must be some with names starting with U, V, W, X, Y, Z?

More Disclosures

CCPView has disclosures from thirty five Clearing Houses, each with many Clearing Services, so there is a lot more data to look at covering Equities, Bond, Futures, Options and OTC Derivatives.

With over 200 quantitative data fields and quarterly figures from September 2015 to June 2019, that is a lot of data to analyse.

If you are interested in this data please contact us for a CCPView subscription.

If your firm is not already a subscriber, it would be great for you to become one.

One of our readers pointed out the reason given by OCC for the large drop in disclosure 17.3.1 – “OCC revised this disclosure. Prior reporting included system availability events that were unrelated to core systems enabling acceptance and novation or calculation of margin and settlement.”