I thought it would be interesting to look at a different product than Interest Rate Swaps and one that is not Cleared, so this article will look at Cross Currency Swaps.

My interest was prompted by one of our SDRView Professional users requesting that we add a new view for Cross Currency Swaps.

When I replied that the volume of trades was low and so we had not prioritised, the response was that “as most Cross Currency Swaps are cross border and involved US counterparties, in actual fact the reported trades represent a larger percentage of the global market in USD/EUR than IRS in EUR”.

I am glad I listened as the the trade data reported to DTCC is indeed very interesting.

Lets start with the largest product, Cross Currency Basis Swaps USD Libor 3M vs EUR Libor 3M.

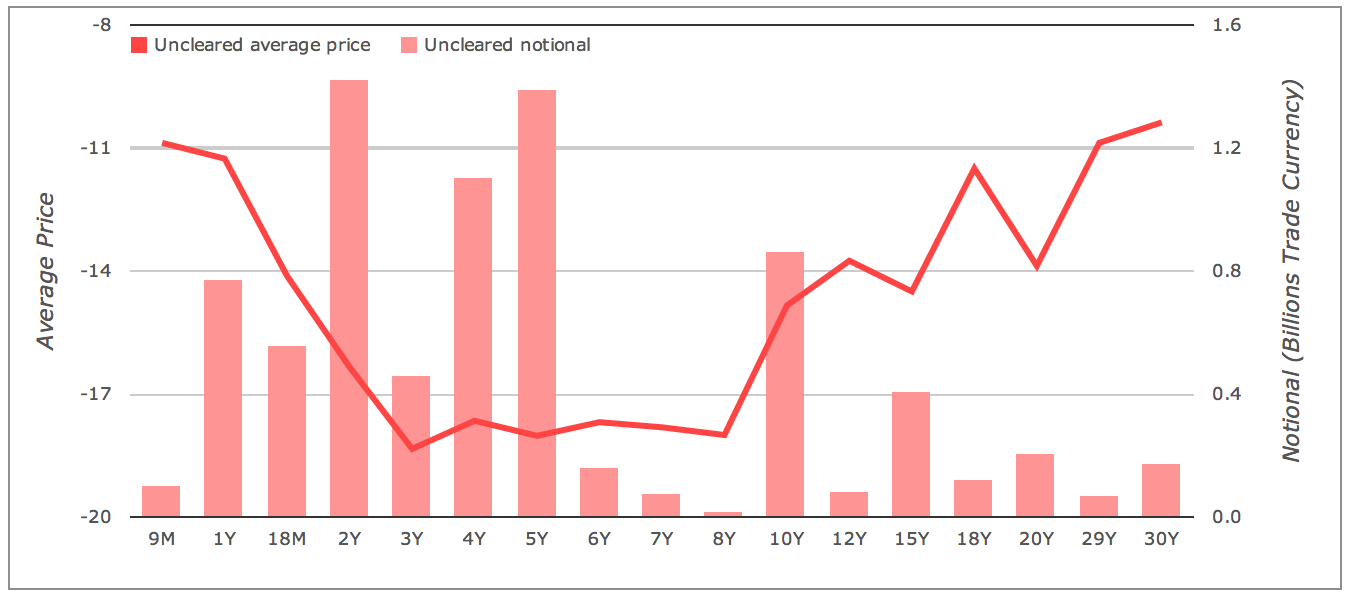

The chart below shows the trades reported in the week of Oct 7th to Oct 11th.

From this we can observe the following:

- Trade maturities range from 9 months to 30 Years.

- The major maturities are 1Y, 2Y, 4Y, 5Y & 10Y, each with weekly volume of > €800 million ($1 billion)

- The currency basis is negative for all maturities and ranges from -11 bps to -18 bps.

- So on a 5Y CCS one side is paying USD Libor 3M and receiving EUR Libor 3M – 18 bps.

- This might seem surprising given that USD 5Y Rates are around 1.5% and EUR 5Y Rates are 1.25%, as following interest rate parity arguments we would expect the EUR side to be approximately EUR + 15 bps.

- However the reality is that the market is not driven by the outright level of interest rates, it is driven by supply and demand.

- There continues to be more demand for USD funding, so the currency basis is negative for all currency pairs except AUD.

Other observations, not shown in the chart are:

- There were 104 reported trades in the week, of which 39 were On SEF and 65 were Of Facility

- Of the 104 trades, only 9 hit the capped notional size

- The average trade size for 4Y and below was > €100M

- For longer tenors the average trade size varied from €35M to €80M

- Trades were not reported in all tenors on every day in the week

- So while most tenors had trades on the last day of the week (Oct 11), some had last trade times on Oct 10 and a few on Oct 9

- The Basis Spread High and Low range for the week was 5 bps for 5Y to 3bps for 3Y

So lots of interesting information.

We could look at other currency pairs, USD/JPY, USD/GBP, USD/CHF.

But I will leave that for you to do yourself using SDRView Professional.

If you find any interesting observations, please send them my way.