The third calendar week of SEF trading is completed.

Recent news is that the first Made Available For Trading applications have been filed to the CFTC, so we may see SEF trading move from voluntary to mandatory in the coming months. Until then, any data on SEF volumes needs to be taken with a grain of salt.

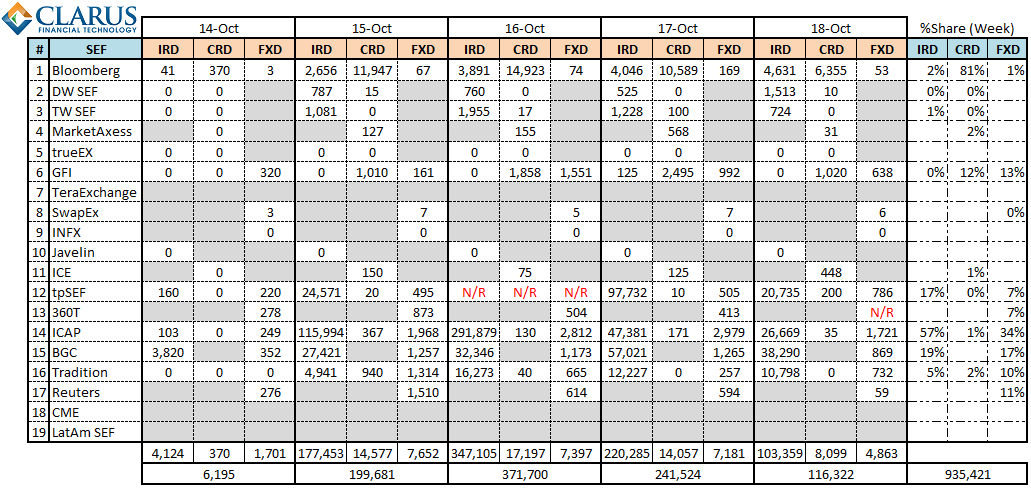

THE DATA

With that said, here is the data. I’ve changed my analysis this week to include all denominations of asset classes, hence the numbers now reflect USD equivalent volumes for all currency denominations of IRD, CRD, and FXD. Once again EQD and CMD volumes were seemingly insignificant so I have left those out.

The data for week ending October 18, 2013:

QUICK ANALYSIS

Once again, it is premature to declare a winner given everything is voluntary and some SEF’s have not yet started. But the data continues to point to a couple facts:

1) The IDB platforms continue to have the majority of volumes in rates and FX. I am led to believe that most IDB voice brokers are now introducing business as an IB into their SEF, so seeing this volume move onto SEF’s is understandable. However, because I would guess that it is still mostly voice brokered, it may not be in the electronic fashion the CFTC had envisioned.

2) Bloomberg continues to have the largest share of Credit volumes. The conclusion I draw from this is that Bloomberg, as the earliest SEF mover, has the most clients on-boarded and hence the majority of whatever D2C business is being done on SEFs. I have to conclude as well that the D2D market is yet to move onto SEF’s in any sizable fashion.

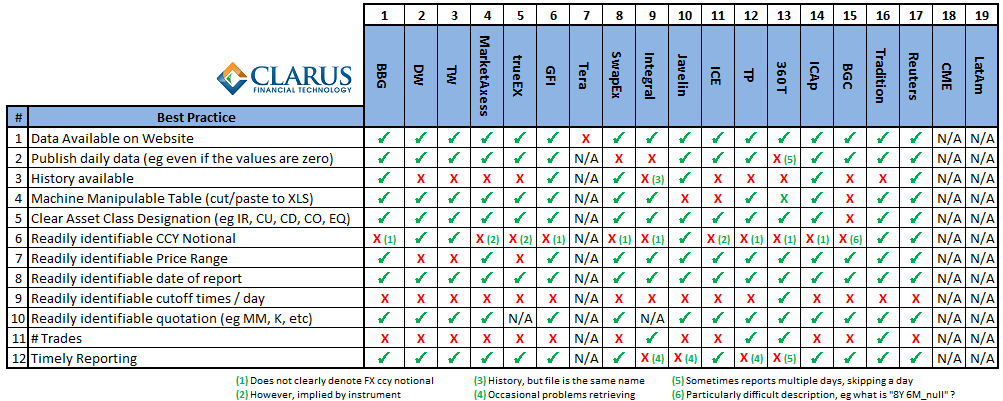

SEF BEST PRACTICES

For my usual readers, you’d be accustomed to me complaining about the effort required to gather and parse this data. Particularly now that I have included non-USD volumes as well, the workload has increased significantly. As I found myself complaining about the lack of reporting standards (for example “why cant they make this easier to interpret?”), I began taking notes. When finished, I had a list of 11 attributes that I felt, in the spirit of transparency, all SEF’s should strive to adhere to. The table below summarizes the best practices and my assessment of how each of the SEF’s currently conform to them.

I include below a brief description of the best practices I would prescribe:

1) Data available on website. Should go without saying that SEF’s need to make this easily accessible. I found general conformity, with only those inactive ones yet to make the data available.

2) Publish daily data. There were many occasions when I would check for the latest reports at 8pm, then at 6am, and still not see data for the previous day. In some cases data a report is not made available if there was no activity, and in some other cases a report is delayed and reported for multiple transaction dates. SEF’s should make the report available on a daily basis regardless of activity, with the leniency to interpret holidays and non-working days as appropriate.

3) History Available. There had been a couple cases where the SEF did not publish data for a particular day, or I was late in checking for the activity report. The archival of public reports should be done and made publicly available.

4) Machine manipulable table of data. My research purposes require me to manipulate the data in Excel. Some firms deliver the data in CSV/XLS formats, some are in HTML, and some in PDF. PDF’s are notoriously bad for extracting data; some may claim that this is in fact one of the intents of the format. I am often able to cut and paste into a text editor and import as space delimited, however spaces in complex data like this mean that data is often offset and not readily usable. Consumers of SEF data should be able to extract and manipulate the data in spreadsheets or more sophisticated data mining tools.

5) Clear Asset Class Designation. When the data is extracted, I want to readily interpret what I am looking at. There is a wide spectrum of conformity here, but I’ve noticed some SEF’s making clear the asset class (IRD=IR, FXD=CU, CRD=CD, CMD=CO, EQD=EQ). The other end of the spectrum requires one to interpret some strings of product description, culminating in my personal favorite product I’ve seen: anyone care to make me a market in “8Y 6M_null”?

6) Readily identifiable CCY Notional. The volumes reported need to be understood. Common complexities are with FX. With my FX background, I am used to interpreting notional data in terms of the primary currency, so that for example a EUR/JPY notional of 1mm means it is 1 million EUR. Just when you think you understand how the data is being reported, you get some USD/IDR trades (market rate is approx. 15,000 IDR to 1 USD) reported as 80 billion. While possible to trade 80 bn USD worth of IDR, it does represent 10% of the countries GDP! The most favorable example I have seen on this is a few firms reporting USD equivalent volumes, which makes the data easy to understand. Cross ccy swaps, equities and commodities also lend themselves to difficulty here.

7) Readily identifiable price range. While my analysis does not mine the price data, the spirit of SEF reporting includes transparency into prices. The best examples I have seen are the reporting of open, high, low, and close.

8) Readily identifiable date of report. Particularly when you are not sure if the SEF has updated their daily activity, it would be nice to have an indication of what days’ data you are looking at. File names, tab names, columns or headers are generally used, but in some cases this had been neglected entirely. This has generally been cleaned up.

9) Readily identifiable cutoff times. The FX market has a fairly well agreed end of “business day”. However the SEF reports are currently made available at widely disparate times of day. One SEF clearly denotes on the report the time window of their reporting – for example from 5pm EST Monday through 5pm EST Tuesday.

10) Trade counts. Is that 100 million notional one trade or 100 small trades? Particularly when more clients onboard and use SEF’s, there is the expectation that average trade sizes will decrease. We will require trade counts in order to understand this.

11) Timely reporting. As a best practice, effort should be made to have reports available at a particular time after the close of the reporting period (as discussed in point #9). I often found myself in the late afternoon waiting for a report to be made available for the previous business day. Particularly for those firms that do not make history available, you need to grab the data before it gets overwritten by the new data. My analysis above is admittedly qualitative on this practice.

YOU WANT TRANSPARENCY, I’LL GIVE YOU TRANSPARENCY….

It’s easy for me to sit at my desk and criticize reporting formats. You must remember that the CFTC do not publish a standard for SEF reporting. This is understandable given the nascent nature of SEF’s and the relative complexity of some of this data. Don’t forget as well that even SDR reporting (across SDR’s) lacks standards.

In the meantime, myself and others interesting in mining this data will soldier on with whatever data the SEF’s provide.

Hey, we asked for transparency, and we’re getting it!

UPDATE

This weekly issue of SEF updates is not the most current. To see all SEF posts, including the most recent, please click through to the SEF Category.

This is great stuff and appreciate seeing it on a weekly basis as this all gets off the ground.

Regards,

Terrence