- Regulations can only take us so far in improving our markets.

- Industry Standards to cope with conflicts of interest are therefore being created by the FMSB and backed by all large market players.

- Swap-pricing tied to the issuance of new bonds is a complex area that the FMSB is creating Standards for.

- We take a look and suggest how Clarus transparency data can help market participants.

This is my 200th Clarus Blog!

I think it says a lot about our industry that I’ve written so much in such a short period of time.

Many thanks for reading – this blog helps to make our Clarus software even better!

Culture in FICC Markets

I was recently made aware of a huge effort in Fixed Income markets to improve culture. This was covered in-depth at the BoE Markets Forum, for which I’ve bookmarked the session on “Progress under FEMR” below:

Two things struck me:

- The scope of the Senior Managers Regime to really change our industry. We’ll follow-up on this in future blogs I think.

- The willingness of our industry to now tackle tough topics. Front and centre of this work is a new body that I had never heard of before – the FMSB.

The FMSB

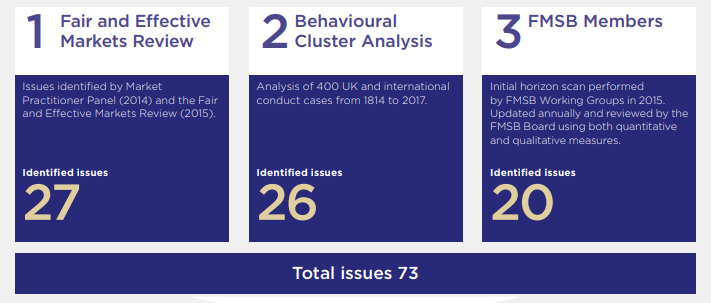

The FICC Markets Standards Board (FMSB) has identified 73 issues (!) in their 2017 annual report that need industry standards to be defined:

So far the FMSB has;

- Produced three Standards (New Issue Process for Fixed Income, Binary Options in the Commodities Markets, Reference Price Transactions for Fixed Income).

- Produced two Statements of Good Practice (Monitoring of written communications, Front Office Supervision).

My feeling is that a lot of this work stems from the LIBOR scandal. With LIBOR seemingly going to disappear in 2021 (see Bill Dudley’s speech at the same event), I think the financial industry is now going to tackle tough topics head-on rather than be left with “another LIBOR moment”.

It’s therefore important to follow the FMSB’s recent work. Today, I will focus on swaps tied to the issuance of new bonds.

Swaps for New Issuance

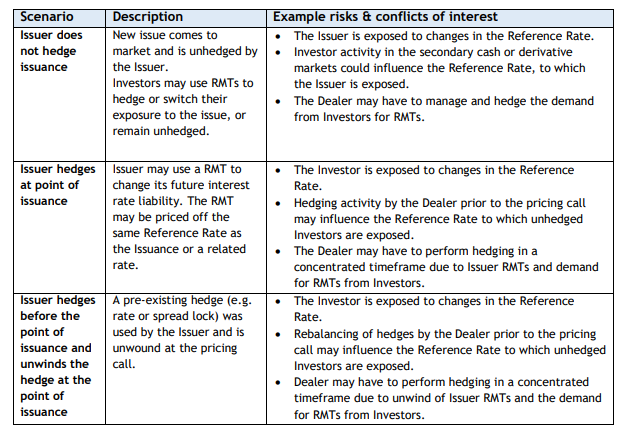

These are the draft standards. They aim to manage the conflicts of interest that arise from a lead manager bank transacting a swap tied to an upcoming bond issue a.k.a Risk Management Transaction (RMT). (I think we should say “swap” as it makes it a lot more understandable).

I wanted to provide some more background over and above the FMSB:

The Standard applies to any Dealers who execute RMTs (Clarus: “swaps”) with Issuers or Investors when the RMT in question is transacted sufficiently proximate in time to the pricing call so that it, or the hedging of that RMT, might reasonably be expected to be capable of influencing the Reference Rate or Reoffer Yield of the New Issue

What does this really mean? In my own words:

Most bonds are brought to market via a syndicate of banks. Large, sophisticated issuers of bonds are mainly concerned with their all-in cost of funds when bringing new debt to market. That “all-in” cost is a relatively complex mixture of:

- Where does the issuer need to price the credit spread to attract existing/new investors? This is typically based upon where their existing bonds are currently trading plus a “new issue premium” (which is actually a discount for investors..).

- What is the spread to a reference funding rate? Historically that reference rate would be a floating rate and hence Libor. But very few FRNs are issued – the new bonds are likely to be fixed rate.

In terms of swap pricing and setting Standards for market behaviour, we are concerned with Point 2 today.

Most issuers of bonds would be exempt from a Clearing mandate, therefore the New Issue swap will have to be priced by traders because:

- The size of risk is way bigger than any on-screen liquidity will ever provide.

- A bilateral trade attracts a number of different valuation adjustments – namely credit (CVA), margin (MVA) and funding (FVA).

- For both of these reasons, a New Issue swap could never just be priced as an “agency” trade or as a particularly large “block”.

Swaps traders are integral to the new-issue process and therefore have to manage their conflicts of interest and not react to non-public information.

It’s a really, really tough area to cover and I salute the banks for tackling it via standards. I don’t see how regulations can be prescriptive enough to help here.

What to do?

The first thing to do is acknowledge the problems. The FSB sets out the potential conflicts of interest:

Which covers;

- Conflicts of interest that could negatively impact both investors and issuers depending on the hedge activity from each group.

- Influencing any Reference Rate as a result of hedging activity by the Dealer.

Define the Standards

Problem defined, we now need some Standards to alleviate the potential problems. The FMSB has drafted 12 Core Principles so far. If I were to put them in priority order, I see three key aspects:

- Disclosure. Make Investors and Issuers aware of the key mechanics inherent in the issuance of bonds. (I’d love to see one of these disclosure letters if anyone has an example.)

- Choose a good Reference Rate. If it’s a deep enough market, the off-setting interest to any hedge is easier to find.

- No Manipulation. In the FMSB’s words:

“Dealers should manage their hedging of RMTs such that it is solely aimed at risk mitigation and is never performed for the purpose of influencing or manipulating the Reference Rate or Reoffer Yield.”

You can read all 12 Core Principles here.

Stopping Short of “Best Execution”

Clarus might normally advocate dealers providing a “tape” of all of their hedges to their clients (issuers and investors) to manage the process. The Standards consider this:

And is further expanded upon:

Dealers will be facilitating other client transactions, or managing their own risk positions. These activities are usually undertaken on a portfolio basis, and so it is not required, and would be difficult, to assign individual hedging transactions to individual RMTs. Nonetheless Dealers should ensure that the management of their aggregate position is consistent with this Standard.

I agree wholeheartedly with the sentiment here – ideally, yes we’d show you all of our hedges. But with large swaps such as these, banks could be warehousing risk for weeks at a time and versus other clients. We have to make sure that these Standards enable banks (and other intermediaries) to fulfill their vital role as liquidity providing intermediaries.

Clarus Transparency Provides the Benchmark

A bank (or other intermediary) would be in a really tough position if a large client asked them for details of their hedges. Whilst the trades may be public data thanks to reporting, the bank would end up providing non-public information in terms of the direction of the trades. That must be a really tough conversation on both sides.

To avoid this, it makes much more sense for the end users of swaps to infer this information from the public trade records. All market participants can use our Clarus traded prices to create their own metrics (or use ours) for a scorecard of syndicate bank hedging.

THAT is the real benefit I see from transparency and is the ultimate benchmark for how banks manage inherent conflicts of interest.

Thanks for reading my 200th blog. Anything you want covered in the next 200, please reach out.

In Summary

- Expect to hear a lot from the FMSB as Standards are issued to deal with conflicts of interest in FICC markets.

- These Standards fill a gap in guiding market behaviour that regulations alone cannot fill.

- For New Issue swaps, the Standards include disclosures, choosing a good Reference Rate and not manipulating that rate. That seems like sound practice to me!

- Clarus transparency data allows market participants to measure for themselves the effectiveness of a lead-manager’s hedging programme.

- This analysis should be conducted by swaps users themselves, not the banks. Clarus data makes it possible.