Following on from my article on the CME-LCH Basis Spread, I will now look into the details of hedging this basis with CCP Switch trades.

Example Portfolio

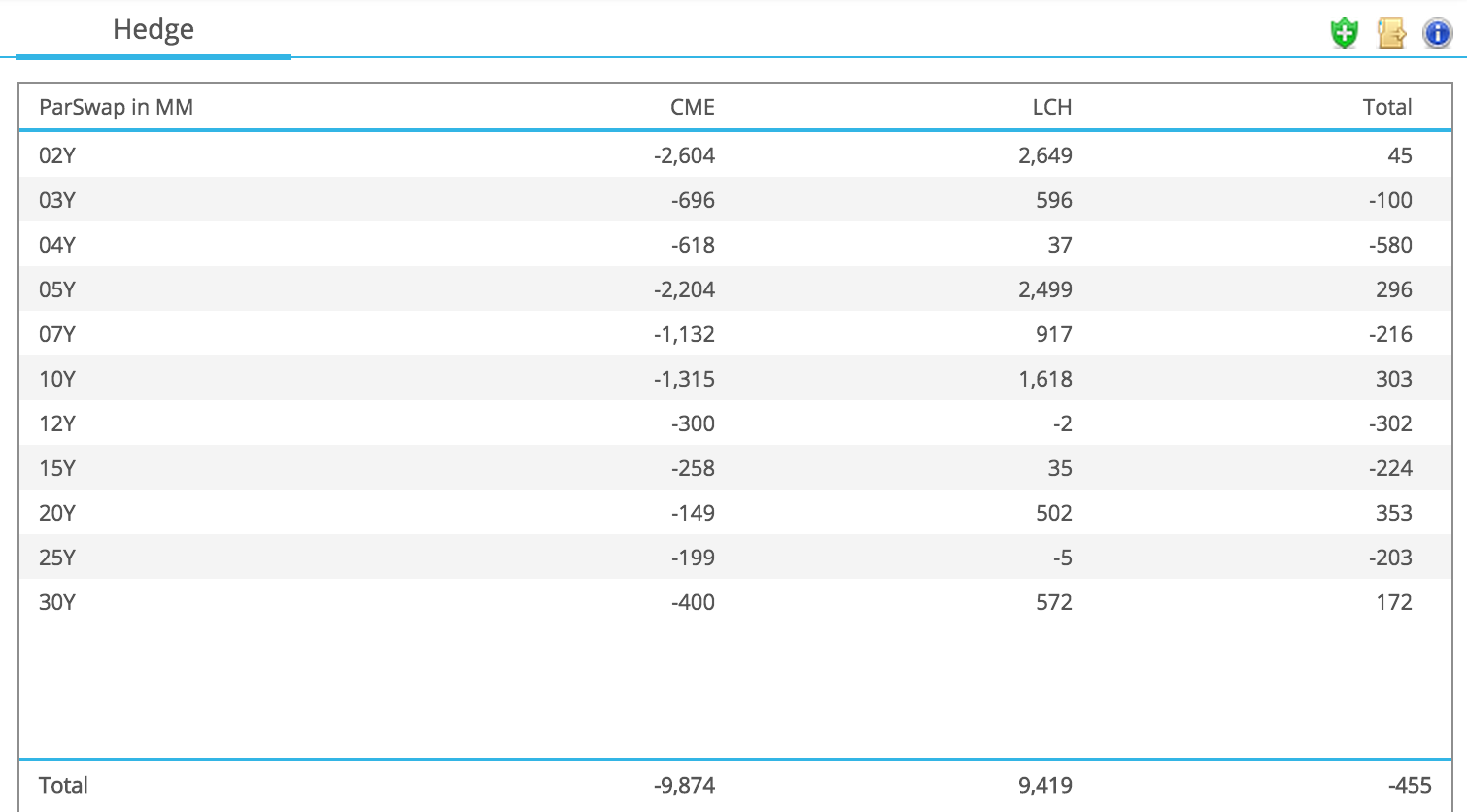

Lets start by constructing an example portfolio of USD Swaps in which we are net receivers in our account at CME and net payers at LCH. Using CHARM we can show each account in Swap equivalent notional terms by tenor as below:

Showing that:

- At CME we are net receivers at 2Y on $2.6 billion

- At LCH we are net payers at 2Y on $2.6 billion

- So one is hedged by the other

- Similarly for other tenors

- Except at CME we have positions on all the 11 tenors shown

- While at LCH we have hedged with seven major tenors

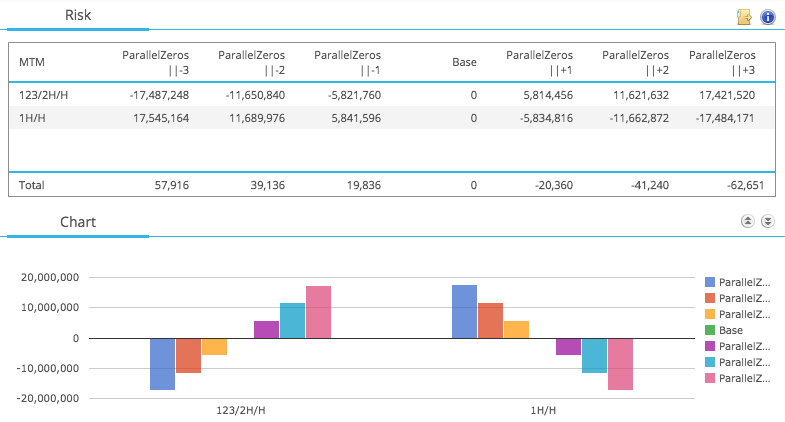

We can check how the hedging performs by applying parallel shift scenarios to the USD curve.

Showing that in each scenario the loss from one account is off-set by the gain in the other and our total mtm change is small.

Initial Margin

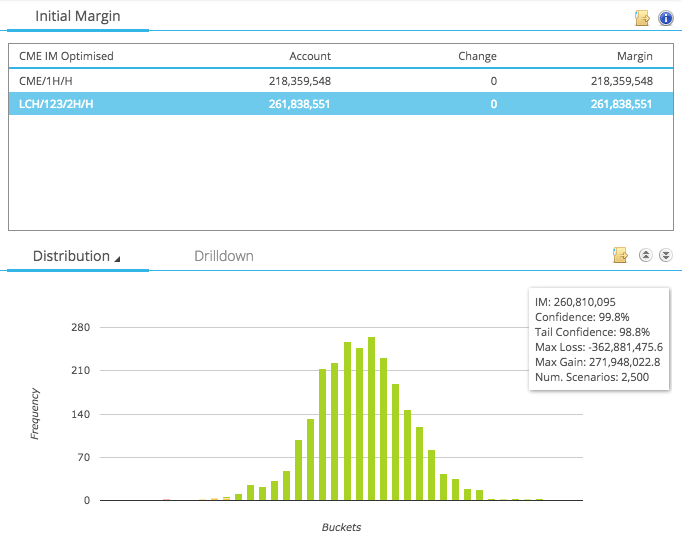

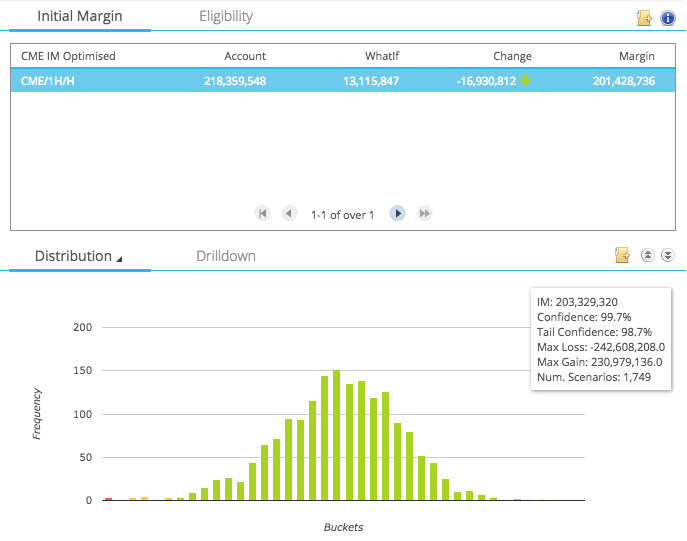

Let us now look at the Initial Margin requirement of both accounts.

Showing that:

- For our CME account, IM is $218 million

- For our LCH account, IM is $262 million

- An overall gross requirement of $480 million

- Which needs to be funded

Contrast this with the situation if all these trades were in one account at CME or LCH; probably no more than $5 to $10 million.

The CCP Basis Risk

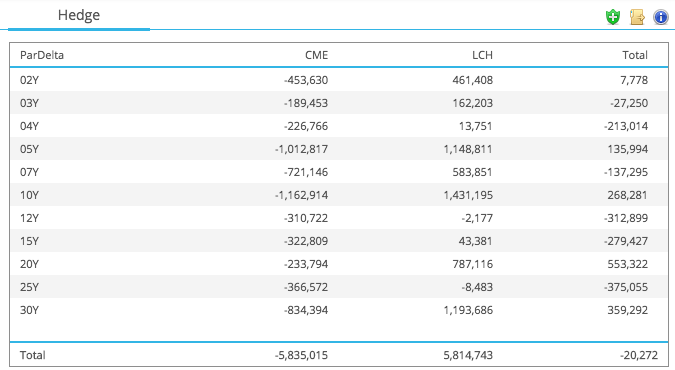

First lets look at the interest rate risk in our portfolio to each CCP. To do so, it is easiest to look not at the Swap equivalents at each tenor but at the 01 of each par swap.

Showing that for a +1bps rise:

- Our CME account would lose $5.8 million

- Our LCH account would gain $5.8 million

- Overall we would only lose $20,000 per point

- So a seemingly well hedged interest rate position

- Perhaps one not too dissimilar to that found at some Dealers

However our basis risk here is that the CME Swap prices and the LCH Swap prices do not move in lock-step.

That is what we know happened in recent weeks. The widening of the spread from 0.15 bps to up to 1.9 bps depending on tenor, would have caused the CME account to change in value while the hedge did not.

So as our CME 5Y 01 is -$1m and we know the 5Y CME-LCH Basis moved out to +1.2 bps, we would have lost $1m on this move. Repeating this for each tenor in our example portfolio would give us a $7.5 million portfolio loss.

And the risk remains that the basis could widen further and we could incur more losses.

So how can we quickly hedge this risk?

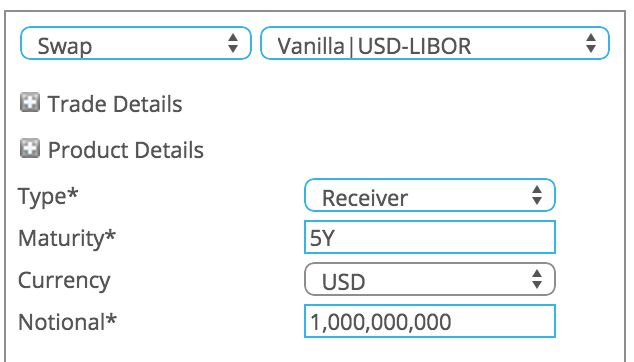

CCP Switch Trade

Enter the CCP Switch trade, where we can transact in large size on a specific tenor, simultaneously Pay Fixed at CME and Receive Fixed at LCH and transact at mid (not pay the bid-offer).

Lets do this on the 5Y tenor where we have a -$1m CME position, hedged with a +$1m LCH position by entering into a $1 billion trade, which on the LCH side is Rec Fixed.

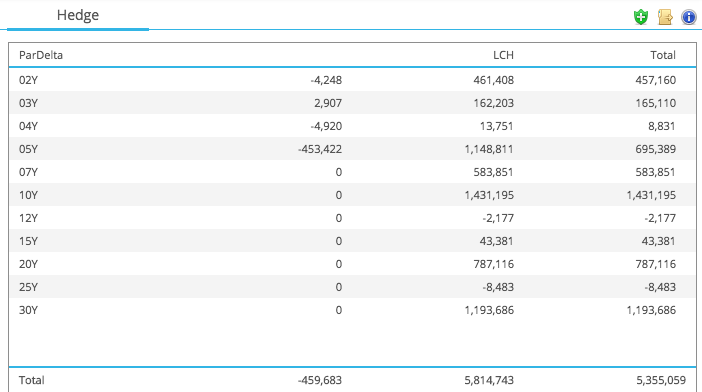

Our 01 risk at LCH would then change as follows:

Showing that the:

- LCH Side of the Switch trade has an 01 at 5Y of -$450k

- Which reduces the LCH Account 01 at 5Y to $695k

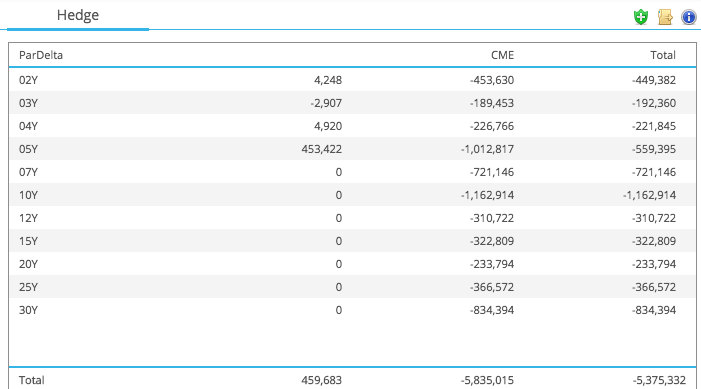

And then then CME Side.

Which shows the opposite effect.

Meaning that instead of:

- CME 5Y of -1$m offset at LCH by $1.1m

- We have CME -$560k offset at LCH by $695k

So while we have not eliminated the 5Y basis risk, we have almost halved it. Meaning that should the spread widen by a further +1bp, we would not lose $1m but $560k.

However from my last article you will recall that we have done this trade by paying away the basis. Using the prices from that article, but this time ignoring the 0.25 bid-offer, it means that on the CCP Switch trade we are Receiving Fixed at 1.65642 and Paying Fixed at 1.66842. So losing 1.2 bps on the trade i.e. $600k.

Is it worth it to pay $600k plus whatever the brokerage is to reduce the risk by $440k of 01?

Before we answer that we need to re-visit our Initial Margin.

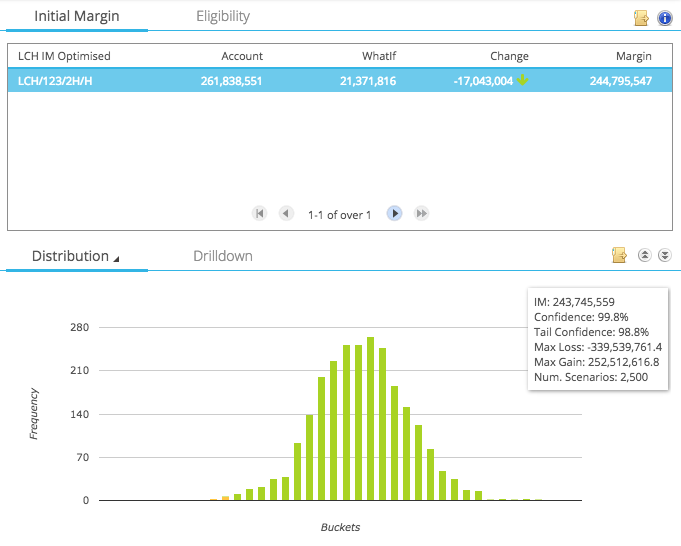

Margin after the CCP Switch trade

Using CHARM, first on the LCH Account.

We see that the IM is reduced by $17 million to $244 million.

And then the CME Account.

Also a reduction of $17 million.

So in total we have reduced our overall margin requirement by $34 million.

That results in a lower funding cost of margin and a lower default fund contribution.

Our funding cost gains depends on our assumptions of the funding rate and term; should it be over night, should it by 5Y and what about the decay of a 5Y Swaps IM over time?

Assuming an overnight funding rate of 50 bps, this is a saving in funding cost of 0.50% on $34m = 0.50% * 1/360 * 34,000,000 = $472 per day. Present Valuing for five years, that would be DV01 5 year swap * Notional * 50bp = (~$460 per million) * 34 * 50 = $782,000, But IM will not be constant for 5 years, so lets take an average maturity = 460*34*50*0.5 = $391,000.

Meaning that our funding cost saving is around $400,000.

Our default fund contribution could be estimated crudely at 8% of IM, which presumably would be charged at an equity capital rate of say 10%, so a saving of $270,000.

Now these calculations are very much Dealer specific, but even our simple example shows a saving of $670,000.

That makes the $600k not look too bad at all.

Wrapping Up

However we also know from my prior article that CME have announced a change in their curves to incorporate CME specific swap observations.

That will mean that even though we are paying +1.2bps more than we are receiving on this CCP Switch trade, assuming the basis remains at 1.2bps, the mark to market of the trade will become zero and not minus $600k.

Even better.

What is not to like about the CCP Switch trade?

Well we still need to find a Dealer to do the opposite side, so Pay Fixed at CME and Rec Fixed at LCH.

Whats in it for them, except perhaps to avoid the bid-offer and transact at mid?

Well they may have the opposite position. (Though we know this is unlikely to be true at all tenors).

They may have a different view on the CME-LCH Basis, in terms of will it widen or shrink.

$20 billion volume in a couple of weeks shows trades are being done and there is a two-way market.

We need to watch the data and see how it develops.