Last week the EBA published a consultation paper on its its draft Regulatory Technical Standards (RTS) on Initial Margin Model Validation (IMMV) under the European Markets Infrastructure Regulation (EMIR).

This is an important and long awaited publication, particularly for the hundreds of firms in the EU that are complying with UMR IM requirements as of Sep 2021 and the even greater number expected to comply in Sep 2022. The vast majority, if not all of these firms have chosen to use ISDA SIMM for IM, which under EMIR requires model validation approval by EU authorities.

There is an expectation that the EU would grant exemptions from model validation requirements to these smaller firms, similar to those available in the US. Otherwise the more onerous model validation requirements would result in many firms choosing the standard Schedule model, a poor outcome for the industry and one that would lead to un-necessarily high IM requirements, tying up collateral and increasing costs for little systemic benefit.

So what is the outcome?

Well, there is good news and not so good news.

The Good News

The paper envisages two categories of firms:

- large firms (> €750 billion AANA, around 20 firms) will fall under the scope of standard model validation

- all other firms (< €750 billion AANA, P5-6, hundreds of firms) will fall under a simplified validation.

And a transitional framework for the model validation will allow existing IM models (e.g. SIMM) to continue be used, with firms falling under the simplified validation benefiting from a prolonged period of two years to prepare.

So there you have it, perhaps not what some firms hoped for, but welcome nonetheless and will certainly help mitigate the huge number of validation requests and potential market disruption, without such a proposal.

(Note Article 2 of the RTS, does allow NCAs to decide based on the complexity and interlinkages of a counterparties OTC derivatives activity, to apply standard model validation where the AANA is > €50 billion).

The Not-so Good News

Many firms has been expecting an exemption or complete outsourcing of model validation requirements and in particular no requirement to perform Backtesting of the IM model. The argument being that ISDA and large P1-2 firms conduct regular backtesting for ISDA SIMM, so other firms should be able to rely on this, as they can under US jurisdiction regulations. And not being able to rely on such validation would place an onerous requirement on hundreds of smaller firms for no systemic benefit.

A compromise in the consultation paper is that under the simplified validation process, firms do not have to perform static backtesting (on a quarterly basis) but will be required to perform dynamic backtesting (a simpler, daily process).

This is a reasonable position to take, static backtesting could be onerous for many smaller firms, while dynamic backtesting is good practice for all firms.

To understand the detail, lets look at what is required under each of the approaches.

Static Backtesting

Static Backtesting is the generally accepted method to backtest an IM model and performing this for SIMM requires the following:

- Actual or hypothetical counterparty portfolios

- Historical market data for 3Y rolling and 1Y stress period (2008)

- Generation of 1d or 10d scenarios from this data

- Re-value portfolios with these scenarios to get PL time series

- Compare SIMM (1d or 10d) and clean PLs (1d or 10d)

- Perform BIS Traffic Light Test (green, amber, red)

- Investigate Exceptions (PL > SIMM)

To perform this on a quarterly basis requires a significant amount of preparation and resources.

For example, the need to ensure that historial data is available for all risk factors in the current portfolios or if not appropriate proxy data used and then the need to run the back-test which requires computational resources to perform 1,000 re-valuations of each trade in a portfolio.

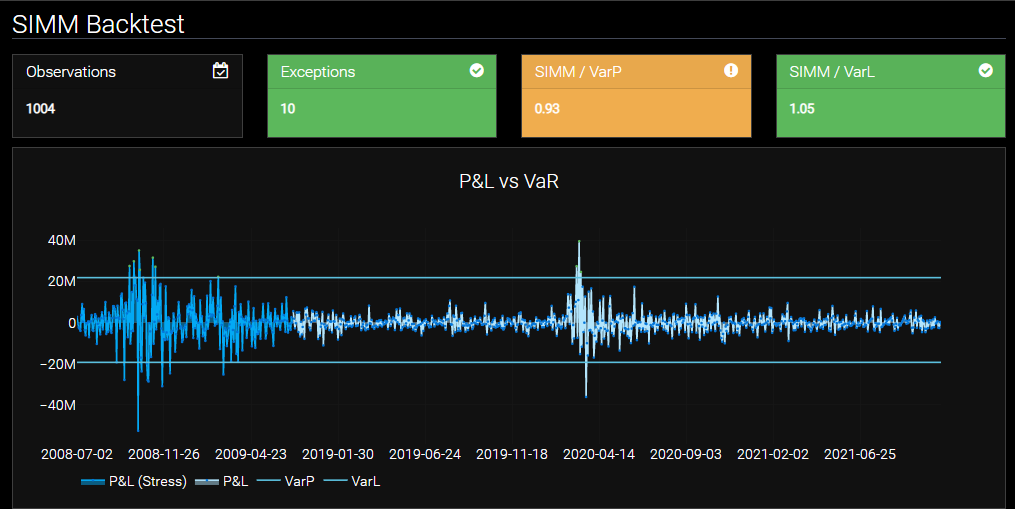

In Clarus CHARM we offer SIMM Backtest functionality to automate this, as is shown below:

Nevertheless the requirement to run Static Backtesting on a quarterly basis remains a significant operational task, requiring clean historical data, specialized software such as CHARM, computational resources for the calculations and analysis of the results and investigation of exceptions.

Dynamic Backtesting

In contrast performing Dynamic backtesting is operationally very different and simpler.

In the simplest terms, it can be seen as just comparing the ISDA SIMM Margin each day with the PL the next day for each counterparty portfolio and building up a time-series over time and counting the number of exceptions (PL > SIMM).

On the face of it, every firm running SIMM, will have these numbers daily and not require any historical data or computational resources to run. Simply collect numbers in a spreadsheet, build up a daily history and compare on which day PL is > then yesterday’s SIMM

Of-course there is a bit more devil in the detail:

- Firstly the daily SIMM we have is for a 10-day MPOR, so we need to re-calculate for a 1-day MPOR

- An approximation is to divide by sqrt(10) but much better is to re-calculate using the 1-day risk weights and correlations published by ISDA

- Secondly the PL needed is not for a book or fund but for trades in a counterparty portfolio (netting set)

- Thirdly the appropriate comparison is not to actual PL but a clean PL (also called hypothetical PL)

- By clean PL we mean PL due to market moves on the start of day position, so stripping out any PL from new trades, settling trades, cashflows, fees and the like

- This clean PL may not be available from existing PL reports, in which case it has to be calculated

- Then there is the automation to calculate or get SIMM and clean PL each day and then build up a time-series of SIMM vs PL comparisons

- The output of which looks much like the CHARM screen shot above but for a shorter time period (the EBA paper says 250 days / 1 year)

From the above it should be obvious that dynamic backtesting is far less onerous than static backtesting.

It does not require scenario generation and clean historical market data or compute resources to run.

Further it is simply good risk practice to collect and compare a time series of daily Margin and PL to assess the adequacy of the Margin over time.

Very simply (and crudely) there is value in doing this by taking 10-day SIMM, converting to 1-day using sqrt(10), comparing to next-days Actual PL and building up a history in Excel or a Database.

Even better if SIMM calculated for 1-day MPOR and clean PL are available from a solution such as CHARM.

What else is in the paper?

At 70 pages, as you would expect, there is a lot.

The full text of the draft RTS, background and rationale and of-course the questions for consultations.

There are a number of other important points that I don’t have time to cover in this blog, such as IM model assessment, supervisory validation by competent authorities by providing the necessary documents , thresholds of 5%, 10% or 20% of the IM computed that trigger a new validation, outsourcing and temporary non-compliance and more.

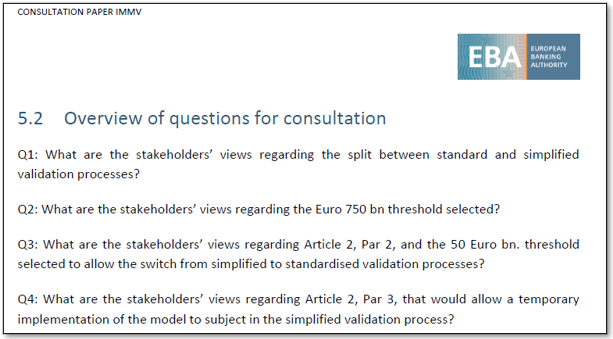

And then there are 37 questions in the consultation that EBA is seeking responses to, starting with:

I would encourage you to read the full consultation paper.

The deadline for responses is February 4, 2022.

Any views or comments, please also let us know.