The big VM deadline has come and passed. Did trading grind to a halt?

Prior to the date, based primarily upon what I had read in news articles, I would summarize my sentiment around the VM implementation as:

- The industry had not gotten through even half of the required new paperwork

- Large asset managers being the most impacted, as they might have hundreds or thousands of CSA’s to rewrite/amend

- The CFTC had given a 6 month reprieve, but that didn’t help anyone as very few have the CFTC as their prudential regulator

So I believed the hype, and thought there would be many firms unable to trade on March 1st.

Data

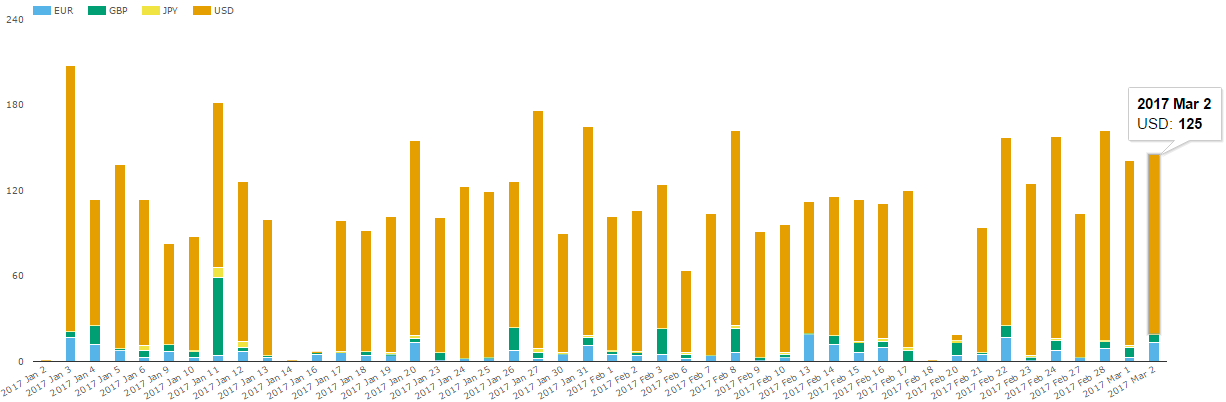

We’re now 2 days past the event, so let’s have a look at what SDR volumes looked like on March 1 and 2. Of course, the VM regime only applies to the bilateral space, so let’s look at Uncleared Fixed/Float swaps in G4 currencies:

Showing:

- March 1 and 2 generally look consistent with other days.

- Quite interesting that only 100-200 bilateral swaps are traded on a daily basis these days. Go Dodd-Frank.

- I had heard some anecdotes that many hedges were put on pre-March 1st in order to get ahead of the deadline, but again nothing too crazy to corroborate that.

I’ll spare the charts, but when I look at bilateral swaptions (roughly 300/day), inflation (maybe 20/day), and XCCY basis (maybe 80/day), none of these showed any drastic reduction in trade counts in March.

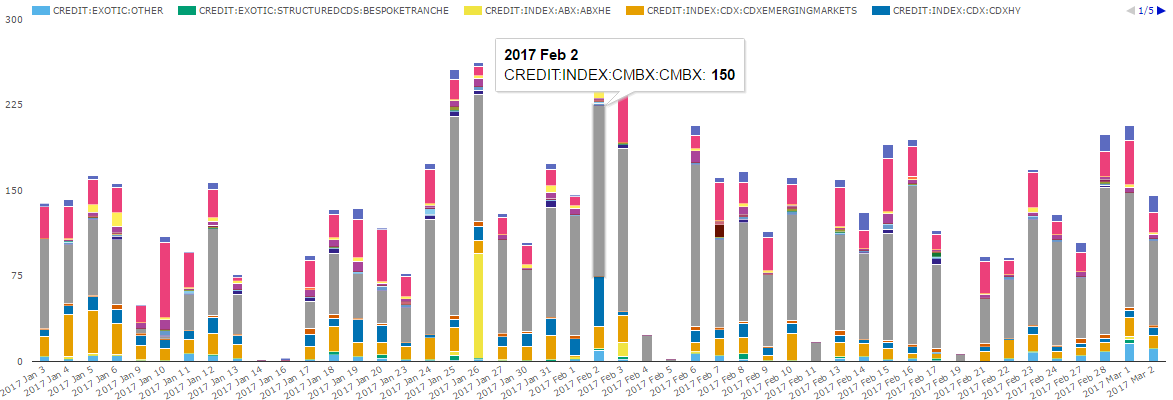

Lets turn to Credit Derivatives. I’m guilty of assuming nearly everything is cleared there, but of course there are non-clearable products like CMBX and options. So worthy of a look, this for all bilateral USD products:

Once again, not much to see here. There were 207 and 146 credit products traded bilaterally on March 1st and 2nd, in line with running averages this year. We aught to highlight that CMBX is indeed an active product with many days over 100 trades/day, which explains CME’s announcement last year that they intend to clear these one day.

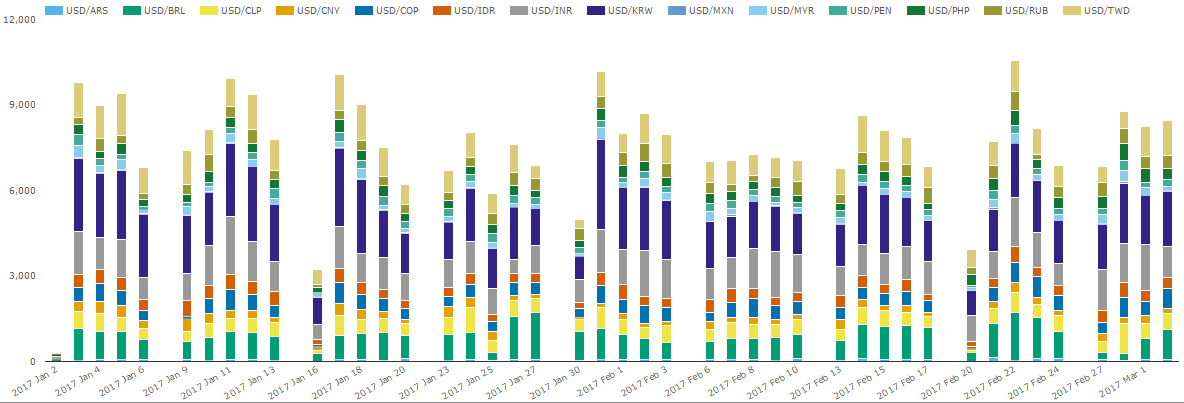

Bilateral FX anyone? Here is Year-To-Date bilateral NDF trade counts:

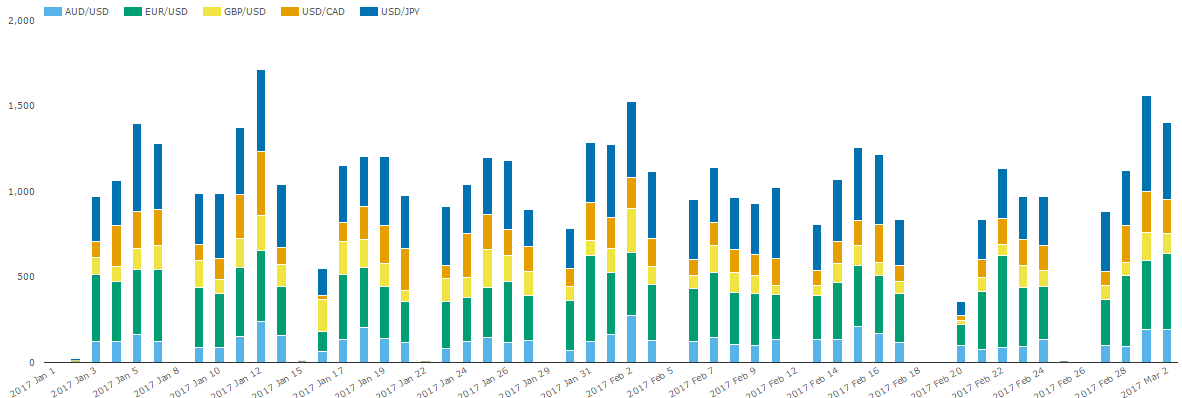

And most liquid FX Options:

So…. Nothing Changed ?

I suppose there are a couple caveats in this data:

- Ideally we’d be able to look at just dealer-to-client activity when pulling these figures

- March 1st was an active day in the market, being the day after Trump gave a “normal” speech to Congress.

But regardless, I think its safe to say nothing ground to a halt.

And don’t forget, even if a client didn’t sign new CSA’s with 10 of their banks, it still means they might have traded as usual, but just with the one or two banks they had finished all paperwork with. So that story might not be one of volume being impacted, but rather one of limited choice and liquidity.

Lastly, I’ve been told there was some guidance given by the OCC and the Fed last week:

My sources tell me these letters basically say “as long as you have SOME CSA in place, can prove you are working to complete them, and do not have massive exposures, go ahead“. Of course that is not legal advice. And Rob Smith at Risk has his own take on this in his article Hazy guidance causes chaos on first day of VM regime, which highlights that banks are struggling to interpret these themselves.

So there you have it. Don’t go stopping what you were doing. And stay safe out there.