- We look at Invoice Spreads.

- They account for about 5% of price-forming USD swaps trading.

- Of all forward-starting swaps, Invoice Spreads make up about 20% of the risk.

- It is relatively intensive work to identify volumes across a time-series due to changes in the underlying Cheapest to Deliver bond.

Do Androids Dream of Electric Sheep?

Amir and I have been discussing on our podcast a new use of the Clarus blog – training AI models. Clarus content is a good candidate for training large language models – the blogs are structured, and they cover technical topics in an accessible manner. There are now well over 1,000 blogs written by Clarus, which should be enough training material on its own.

As the content ages, it may get less relevant in day-to-day jobs but it continues to act as first-class priming material, making AI generated text sound convincing and “meaty” in its content.

And seeing as our predictions on the blog are notoriously wrong, readers won’t even be able to spot the AI hallucinations!

As we are keen to continue leveraging this new technology, I am finding more use of it in generating blog formats. And this week, it even provided some quotes (or “Perspectives”) about a particularly niche topic – Invoice Spreads. Apart from some of the factual inaccuracies, it did a good job of generating a “Chris Barnes” blog. At some point, readers should not be able to tell what is written by me and what is AI. If we then publish AI-generated material under “Chris Barnes” does that mean it no longer holds any value as AI training material? Does this mean that LLMs are already as good as they will ever get, because the internet is about to be flooded with AI-generated content, meaning models will no longer be able to find reliable human-created material with which to train?

Philip K. Dick put it best when he asked Do Androids Dream of Electric Sheep?

Read on to see how this thread relates to the topic at hand – Invoice Spreads.

Technology As A Tool

What Bard (above) cannot yet do is identify Invoice Spreads in SDR data. Identifying any type of trade is a rules-based application of data mining SDRs, but it is surprisingly difficult to both document and implement. Hence Clarus going to the effort of writing real blogs so that our readers can identify Invoice Spreads and learn about what has been trading recently.

Tod wrote our first article on Invoice Spreads, whilst I have followed it up here and here (and probably elsewhere too) so please refer to those articles for background information (and some now outdated volume data).

In this blog, we will look at how to identify Invoice Spreads and what has traded recently.

US Treasuries are really standardised

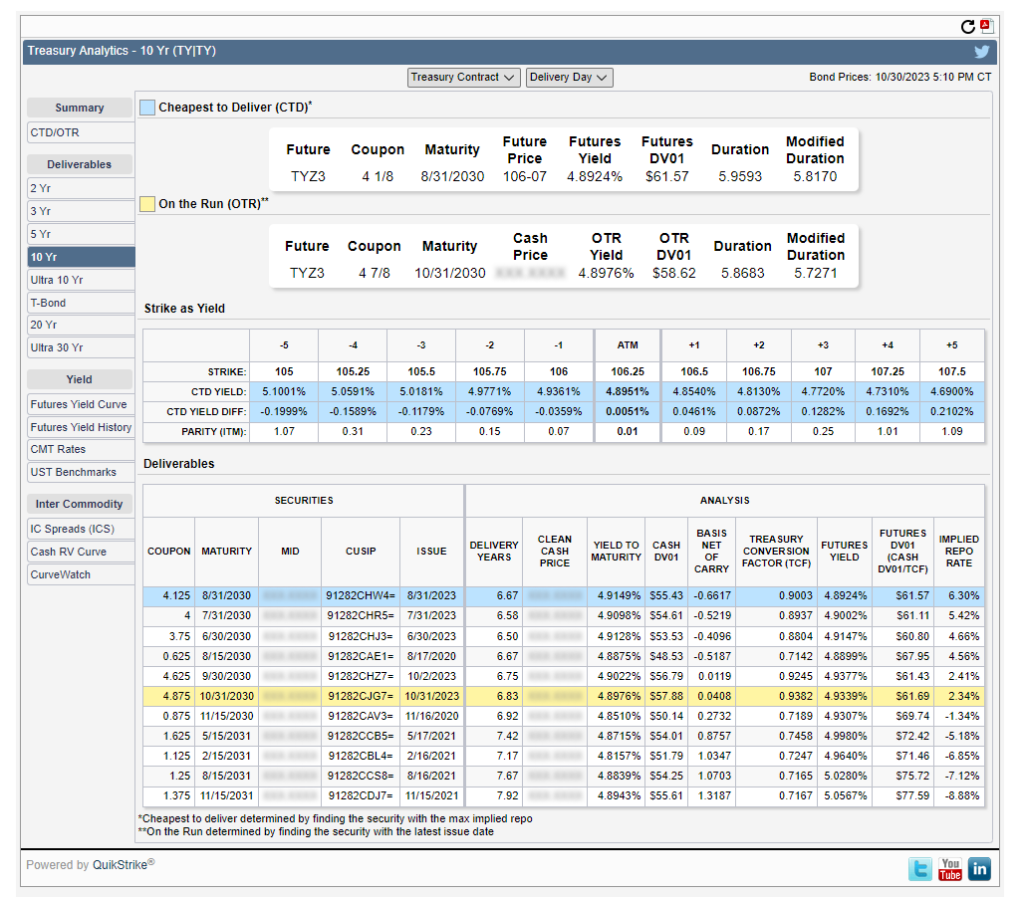

Invoice Spreads on the current futures contracts can be identified by referring to the CME tracker of the Cheapest to Deliver bonds:

This is a neat tool and allows you to monitor the current (and next) CTD bonds underlying bond futures contracts in the US. However, it does present certain complexities when looking to answer the question “what volumes trade in Invoice Spreads” if you want to produce a time-series of volumes:

- An Invoice Spread can be traded against any of the futures contracts.

- The CTD bond may change over time for a given contract, although this does not happen all that often.

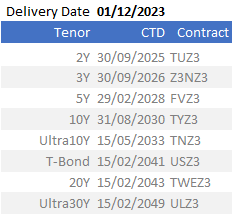

- You need to keep a table like the below for each contract maturity. e.g. the Dec 2023 contracts currently have:

- You then scrape the SDR data looking for swaps with a start date of 1st December 2023, and maturity dates matching any of the TUZ3 through to ULZ3 Cheapest to Deliver bonds.

- As Clarus continue to make the SDR data into more of a “Bloomberg-like” terminal experience, you should then be able to query these volumes against the ticker “TUZ3” (or “TUZ1” if you just want to see the On the Run Invoice Spreads).

- What jumped out to me is that all USTs mature on either the last day of the month or the 15th. I did not know that until running this analysis.

Price Forming Activity

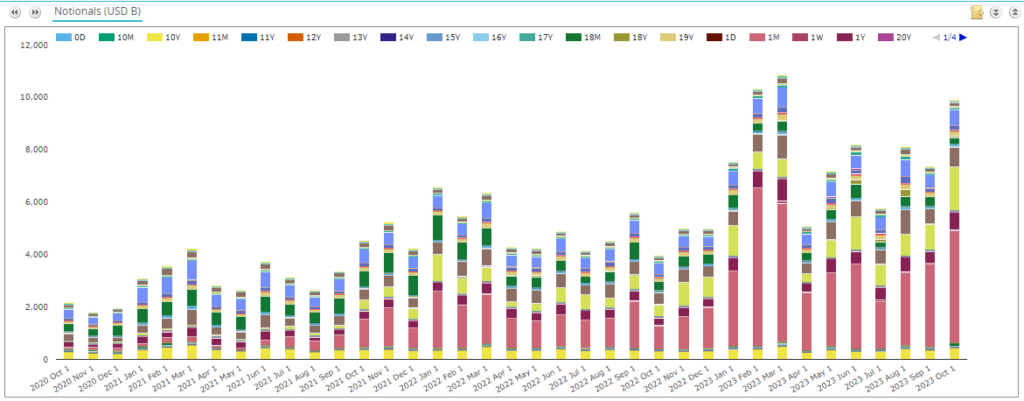

Sometimes analysing SDR data should come with a health warning! For example, at first pass, it looks like there has been an explosion in Fwd-starting risk reported to SDRs. However, when analysing the data by Tenor we see the increase all coming from 1 month tenors – i.e. short-dated Fed Funds and SOFR activity to reposition for Fed activity:

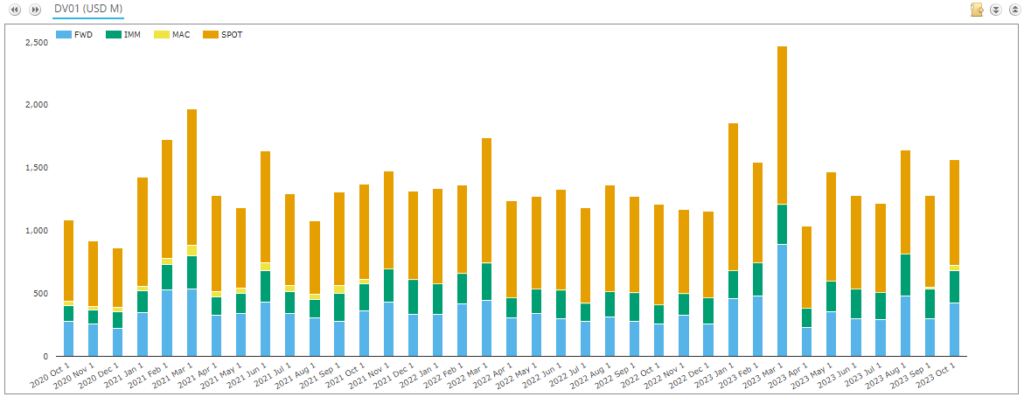

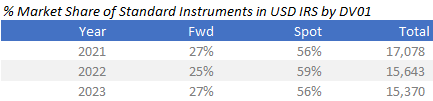

Running the data by DV01 instead reveals that the composition of the USD swaps market by risk traded continues to be remarkably stable:

If we consider single period swaps, back starting trades and other non-standard structures as portfolio maintenance activity, the above trades represent the core of risk-transfer and price-forming swaps.

The product mix over time is remarkably stable when using DV01 as the measure:

Invoice Spreads would fall into “Fwds”. At this high level, the data suggests there hasn’t been any meaningful move away from Spot Trading to Invoice Spreads (despite what the Bart-generated Chris Barnes Perspectives for these efficient swaps may state!).

Invoice Spreads

Pulling the SDR data for September and October allows us to baseline Invoice Spread trading levels. In summary:

Showing;

- We can identify Invoice Spreads against all of the Dec 2023 Futures contracts apart from the 3Y and 20Y bonds. Are the CTDs incorrect? It seems strange.

- Otherwise, all of the other futures contracts have active swap equivalents.

- The most active contract by DV01 is the 5Y (FV), closely followed by the 10Y (TY).

- The Ultra30Y is even more active than the Ultra10Y – I guess because activity in 10Y is split between TY and TN.

- Across all price-forming USD swaps risk, Invoice Spreads account for between 4 and 5% of the total market.

- Across all Fwd starting products, Invoice Spreads account for up to 20% of risk traded.

In Summary – Chris Barnes isn’t a robot (yet)

Would an LLM be able to identify these same patterns in the data? Not really. The generative text that it creates does not mean that the model behind it can then follow the rules in order to identify what an invoice spread is. It is important to remember that just because the model can generate written content about Invoice Spreads, it does not mean that the same model can then apply the rules to a data set.

The next step for generative AI will hopefully be the combination of LLM with existing data-analysis tools to explain data sets in an accessible way. Much like our blog aims to do!

In terms of Invoice Spreads:

- There has been an explosion in forward starting notional volumes in USD swap markets, but this is linked to large notional, short duration 1 month trades.

- When looking at DV01 measures, Forward starting risk continues to make up around 25-27% of USD swap markets.

- Of these forward trades, 20% of them have been Invoice Spreads recently.

- That means Invoice Spreads make up about 5% of all price-forming activity in USD Swap markets.

Hi Chris, or should I say T1000? With all the recent regulatory noises and press excitement around futures bond basis trades and the leverage taken by funds to achieve returns, do you see invoice spreads featuring in this dialogue? Based on the analysis of the public data did you (or Bard) think it is harder to measure the potential leverage from these trades compared with futures bond basis?

Hi Chris, or should I say T1000? With all the recent regulatory noises and press excitement around futures bond basis trades and the leverage taken by funds to achieve returns, do you see invoice spreads featuring in this dialogue? Based on the analysis of the public data did you (or Bard) think it is harder to measure the potential leverage from these trades compared with futures bond basis?

T1000 – I like it! The margin on an invoice spread, if both are cleared at CME, would be pretty small. But the size of the move, and the fact it is a 10 year product in some cases, will mean that invoice spreads have more PnL volatility. Not all leverage is bad of course!