If you’ve been following the package trade exemption, you’d know that Invoice spreads are one of the last package trades yet to be traded on-SEF. The swaps are due to be SEF-required (MAT’d) in November of this year.

I wrote a blog last year about the issue here. While I am no further educated on just how these products will trade on a SEF, it seems there could be a new flavor of these packages occurring.

Invoice Spread Recap

Simply put, invoice spreads are an OTC swap traded against a bond future, I go into a bit of detail in that previous article. For the purpose of this article, its worthwhile noting the characteristics. I am led to believe there are many manifestations, whereby the OTC swap dates in relation to the future are as follows:

- Swap dates match the dates of the bond future (swap effective date = futures delivery date, and swap maturity date = maturity of the futures cheapest to deliver underlying bond). This I believe to be a textbook Invoice Spread.

- Swap effective date is spot, with maturity ~ CTD maturity

- Swap is IMM IMM start, with maturity ~ CTD maturity

- Swap effective date is spot or IMM, with a liquid tenor (eg 10YR)

In all cases, the DV01’s of the swap and future are equal and opposite, thereby making it a delta neutral strategy where you are playing the spread between the two. Much like a spread-over treasury package.

Worth noting that the whole CFTC package trade issue would only apply for case #4 (spot starting liquid tenor) and maybe #2 and #3 if the maturity dates chosen were MAT’d tenors.

Finding Invoice Swaps

Because there are various flavors of the OTC swap component, its often hard to find the swap in SDRView. If every invoice swap was the “textbook” variety, we could reliably hunt them down by searching for matching dates.

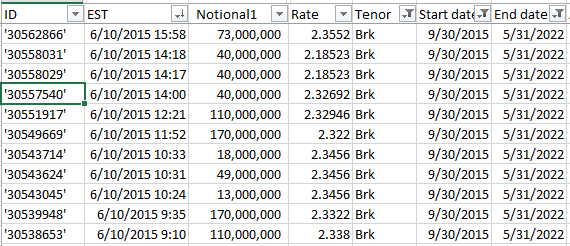

Given that the 10yr bond futures cheapest to deliver is 5/15/2022, I had a look to see what I could find in SDRView that matures in May 2022. Sadly, for my June 10 trade date, I did not find all that much:

I’d like to believe its likely many of these are Invoice Spread related, and its also likely that there are others nestled into SDR activity with non-May dates.

Large Futures Activity

So what is this new flavor of Invoice spreads I mentioned at the start?

Well I was doing some analysis on SEF activity today and came across some interesting looking data. SEFView tracks not only SEF-activity, but also incorporates swap futures executed on a DCM. We originally did this to allow us to track any possible movement of OTC swaps into their futures equivalent products.

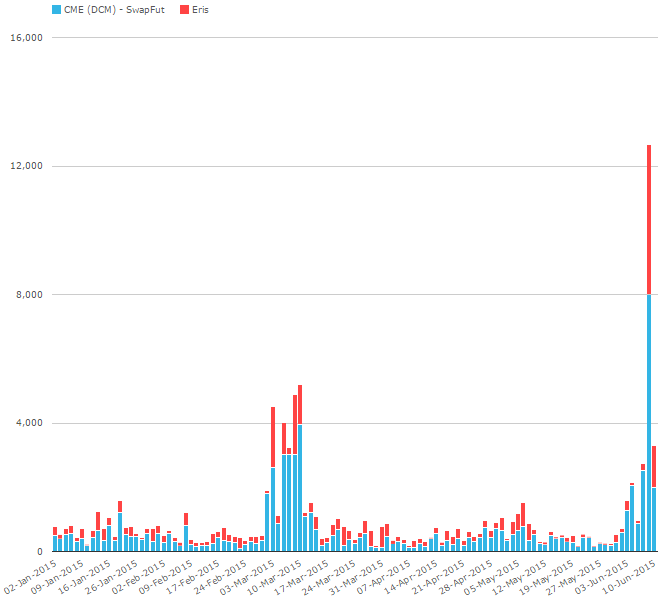

Looking at this activity year to date, we see what we’ve come to expect in quarterly roll activity. In the chart below, the first blip is the early March roll, and the latter blips are this weeks activity, which is also the week prior to the quarterly futures delivery.

But that last blip in particular looks massive. Are swap futures simply picking up?

I drilled into that 09 & 10 June, and sure enough much of it appears to be roll related. But what I found interesting was the Eris drilldown, showing a residual 793 contracts in the 7 year contract, apparently not related to a roll:

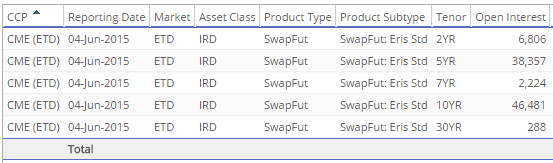

The 7 year contract in itself is a bit odd, as CME does not have an equivalent swap future, and it is not one of the most liquid tenors. In fact, looking at open interest for the 7 year swap in CCPView, we can see the OI stands at 2,224 contracts (as of last week) and pales in comparison to the other tenors (which we should expect):

But importantly, the 7 year Eris swap is roughly the correct swap lookalike to be used in an invoice spread. So my theory goes that folks are trading the 7 year Eris swap future as a proxy for the 7 year swap.

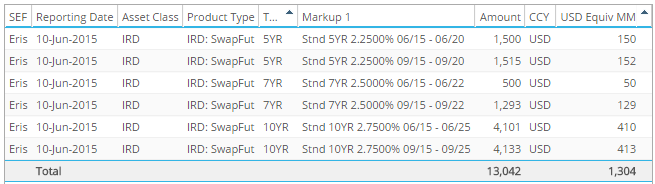

So I went to the Eris website where they publish a trade log and found a good amount of the activity was traded as 1 and 2 lots. I was able to match up the following (and other) Eris swap futures to a corresponding TYU5 bond futures contract.

Now, granted these are 1 and 2 lots (100k USD lot size), but you can see they are executed one after another and could within seconds form a large position (as they are traded in an order book). My theory goes something like this:

- Classic invoice spreads are traded as a package, one execution for the OTC and Futures leg

- An alternative method to trading this spread could be accomplished with Swap futures instead of the OTC swap

- I don’t believe there is any way to execute a “package” invoice spread at the moment, so trades are legged into

- Legging into such a position would be best done in small sizes so that when one side of the trade fails, the algo can stop accruing the position

Plausible?

Summary

To put all of this together:

- Package exemption for MAT swaps vs futures ends in November

- Some flavors of Invoice Spreads may become un-executable because you cannot do an EFR for the future if the swap was traded on a SEF

- There existed some seemingly large Swap Futures activity in early June not explained by simple rolls

- The 7yr Eris future accounted for some of this

- The 7yr Eris future seems a fair proxy to a 7yr swap that would be used in an invoice spread

- Some of the futures trading activity seems to corroborate that the 7yr was traded vs a CME bond future

There might be something in this. If anyone has any further insight into this, please leave a comment or get in touch.