- We take a look at Invoice Spreads with the help of two new features in the Clarus SDRView products.

- We closely examine swaps related to the new CME Ultra 10y UST Future.

- Swaps related trading looks to be a strong driver of volumes in the new contract so far.

- Looking at the maturity profile of the Spreadover market suggests that the initial growth in Open Interest for this contract is set to continue.

- We expect an increase in volumes over the roll period in the coming weeks.

Added Awesome from Clarus

We tend to be a little bit modest about announcing our improvements to SDRView. So this week, I thought I’d take a look at the latest CME product launch (the Ultra 10 UST future) and use a couple of new tools that our regular readers may not have seen yet.

But first, if you need a refresher on Invoice Spreads, please refer to Tod’s excellent blog here.

Trade Search in Pro

You can now easily filter your search results in SDRView Pro. For example, we want to look at Forward Starting Swaps today, so that we can subsequently drill down into some invoice spread trades.

Fortunately, identifying Invoice Spreads got a whole lot easier now that we can filter our trade lists. All you have to do in SDRView Pro is type the maturity date of the Cheapest to Deliver UST for the Invoice Spread you are interested in.

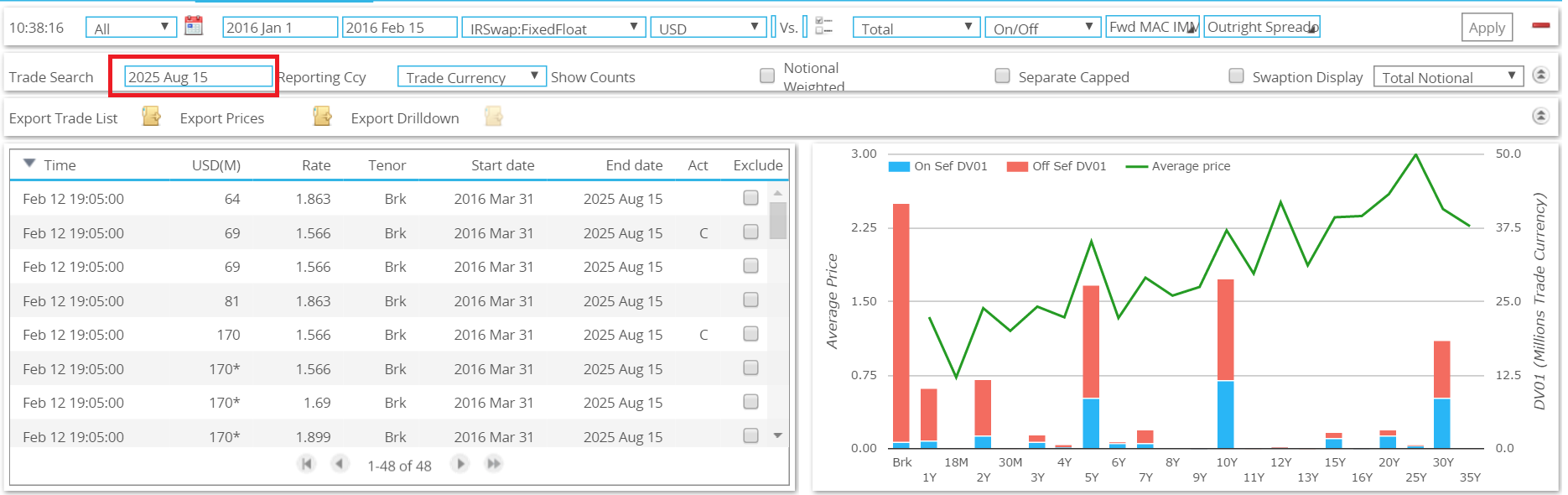

For example, from the CME website, we see that the Cheapest to Deliver UST underlying the new Ultra10 contract matures 15th August 2025. Searching for swaps trades with the same date shows nearly 50 trades transacted in February:

Showing;

- A filtered trade list for trades ending 15th August 2025 – the maturity date of the cheapest to deliver UST for the new CME Ultra 10 UST Future (Code: TN).

This makes identifying specific trends and/or trades much easier, aiding transparency in swaps markets.

More on that new CME 10Y Future

Record launch volumes have been reported for the latest CME contract launch, with healthy open interest and healthy daily volumes. So I thought I’d take some time to take a look at this new contract and see if we can find any swap-related volumes.

The maturity range of the previous 10 year T-note meant that the Cheapest to Deliver UST only had 6.7 years left to maturity. So it has felt like there has been a gap in the deliverable basket underlying CME UST Futures for a while. The headline contract specification of the new Ultra 10 is:

Deliverable basket is original issue 10-Year U.S Treasury Notes, with remaining terms to maturity at delivery of at least 9 years, 5 months and not more than 10 years

Given current quarterly refunding cycles, that should mean that the 3 most recent 10 year UST issues are eligible for delivery.

Given current quarterly refunding cycles, that should mean that the 3 most recent 10 year UST issues are eligible for delivery.

As mentioned earlier, the maturity date of the current Cheapest to Deliver UST is August 15th 2025.

Is this a Swaps-specific contract?

Using the above mentioned Trade Filter, we see the following swaps:

- 44 USD swap trades (vs 3m Libor) with the exact matching dates 31/03/16 – 15/08/25 (the delivery date of the future versus the maturity date of the cheapest to deliver UST) traded this year.

- A total traded notional of nearly $4bn (giving an average trade size of $89.4m).

- A total traded risk amount of $3.4m in DV01, equivalent to 28,600 contracts.

This means that Swaps trading could have accounted for up to $3.4m out of a total $6.4m in Open Interest in the new contract (in DV01 terms. Or 28,600 contracts out of a total of 52,600 as at 12th Feb). Of course, it’s not quite that simple as some of the swap trades could have been in/out swaps and hence represent dealers moving the risk around (“intermediation”). Swaps are also (still) a less balance-sheet intensive way to take on relative value positions. So some of these swap positions are probably related to the expected demand for the new Ultra10 contract.

Still, it’s clear that swaps have been a strong driver of volumes in the new Ultra10 contract so far.

Tenor View in Researcher

Next for today, I wondered if the Swaps market could give us any clues as to potential growth of the new Ultra10 UST future?

For instance, the classic “10-Year T-Note” future (TY), currently has a cheapest to deliver UST maturing on 30th November 2022 – therefore really represents a 6.7 year risk. Why don’t we take a look at the volumes in the swap market for the 6y and 7y buckets, and take a stab at how much risk could move into the new Ultra10 as a result of the preferences displayed in the swaps markets?

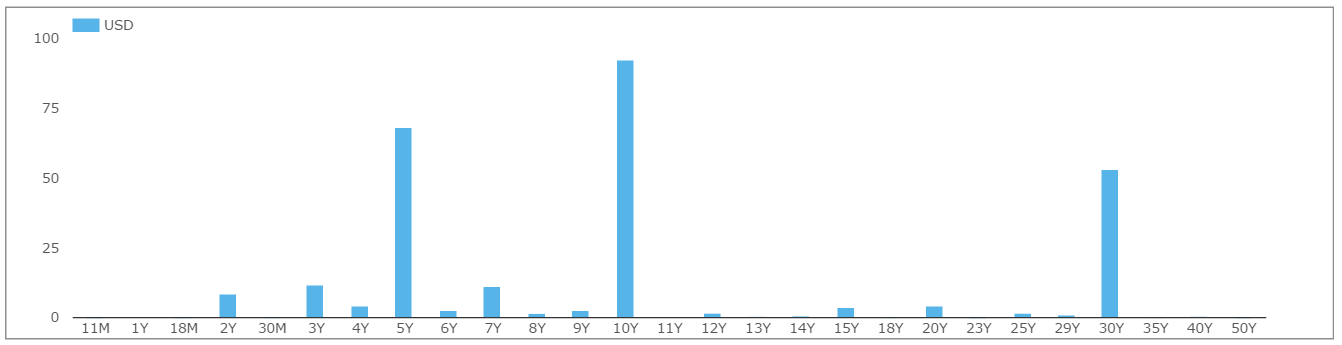

Fortunately, that also means I get to show off one of my favourite new features in SDRView Researcher. From our CustomView, for any time period, any product, any currency combination etc you can now see the results grouped by Tenor. This is particularly cool when using our DV01 measure, and even better when you use the package-adjusted DV01s.

For today, let’s look at the tenors of Spreadovers that tend to trade:

And the API Call is here (please append your own valid token).

Showing:

- Year to date, $92.4m in DV01 has traded in 10 year Spreadovers.

- $68.5m in DV01 has traded in 5 year Spreadovers.

- And hardly anything has traded in the 6y and 7y buckets – just $13.9m in DV01 combined.

I think it’s fair to say that these volumes and maturity distribution are driven by a combination of market preference plus liquidity in the underlying cash UST.

Is it therefore a huge leap to assume that a similar maturity distribution will (eventually) be in place on the CME Rates complex? Given that we have already seen Swaps being a big driver of initial volumes in the contract, it looks like this could have a long way to go. To put some numbers on it, we currently have an Open Interest of about $250m in DV01 terms across the old T-Note and the new Ultra10. A similar maturity split in Futures to Swaps would suggest that Open Interest in the new Ultra10 could grow 33 times to $218m DV01 (or 1.78m contract equivalents)!

The logical conclusion might be that Open Interest begins to drop off in the “old” 10y T-Note future and ends up in the new Ultra10s. We haven’t yet had a roll period when the Ultra10 has been live. But we’d expect to see this trend beginning over the coming weeks as we enter March and the roll period.

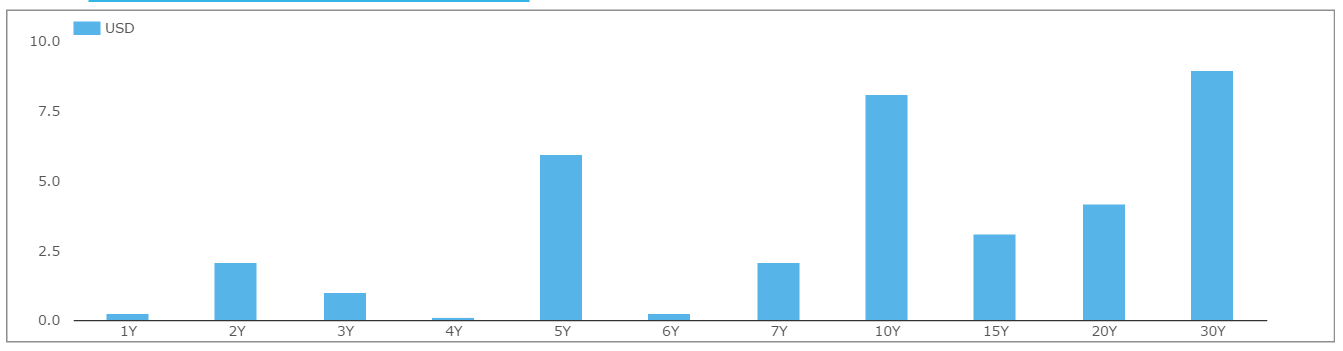

Fortunately, Clarus can also show you the Tenor split of Roll trades. As a reminder, this is what it looked like in USD for December:

I’ll put my neck out here and say that we expect more roll activity in the March period, as positions in the old 10y T-Note are rolled into the new Ultra10.

Talking of Rolls

When I examined the trade list of invoice spreads related to the new Ultra10, I saw that nearly half were transacted as part of Compression or List trading exercises. Given that these are normally risk-neutral exercises, it therefore looks like some Roll activity is already apparent.

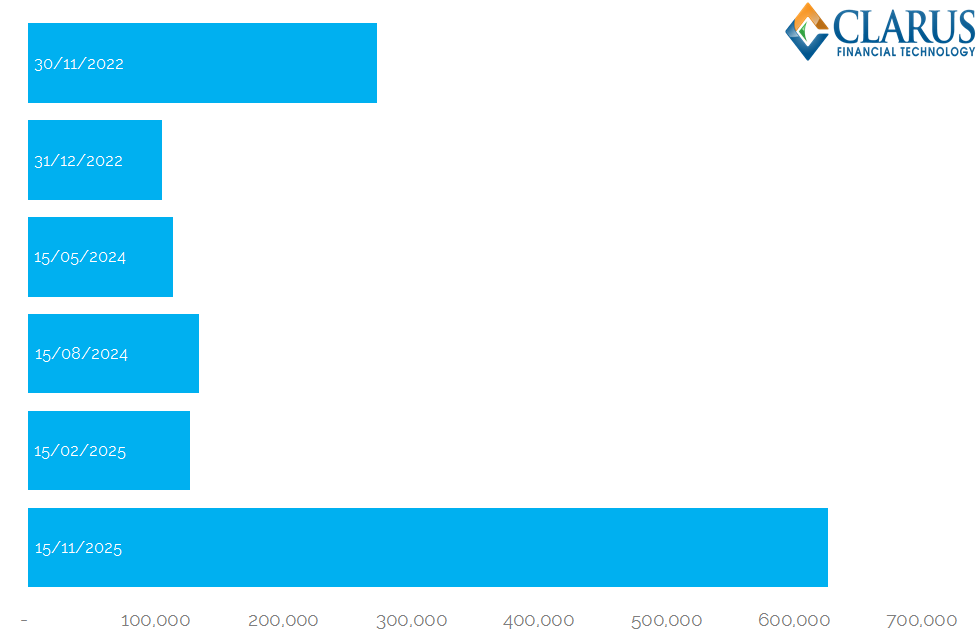

Therefore, let’s take a look at which positions have already been “rolled” out of in favour of the new Ultra10:

What we see is pretty much as expected;

- A narrow range of dates that Ultra10s were compressed against.

- It looks like at least $625k was traded against the 15th November 2025.

- 30th November 2022 is the current CTD for the “old” 10y T-note future, and this accounts for $275k of the List trading/Compression activity.

It will be interesting to see how these volumes continue to evolve, particularly over the roll period. Fortunately, the data will reveal all.

So please subscribe to our newsletter to keep up-to-date with these developments and more across the Rates markets.