- ISDA SIMM v2.6 is effective December 2, 2023

- Updated with a full re-calibration and industry backtesting

- Meaning Initial Margin will change for most portfolios

- In particular, material increases for Commodity and Equity risk

- To quantify the actual impact of SIMM v2.6

- Clarus CHARM can run both SIMM v2.6 and v2.5a on your portfolios

- Listen to the Podcast on Apple or Spotify.

Version 2.6

ISDA has published ISDA SIMM v2.6 with a full re-calibration of risk weights, correlations and thresholds.

The calibration period is a 1-year stress period (Sep-08 to Jun-09, the Great Financial Crisis) and the 3-year recent period ending Dec 2022 (or possibly later, but at time of writing I cannot find this specified, so am going by prior years).

SIMM v2.6 will replace the off-cycle v2.5a (July 15, 2023), which in turn replaces v2.5 (December 3, 2022).

CHARM

Clarus customers using CHARM or Microservices are able to easily run SIMM v2.6 and compare the margin with SIMM v2.5a for their actual portfolios, well before the go-live date.

It is also possible to eyeball the new risk weights and correlations to get a quick feel for likely impacts on portfolio margin levels.

SIMM v2.6 Comparison to v2.5a

Let’s do this by risk class

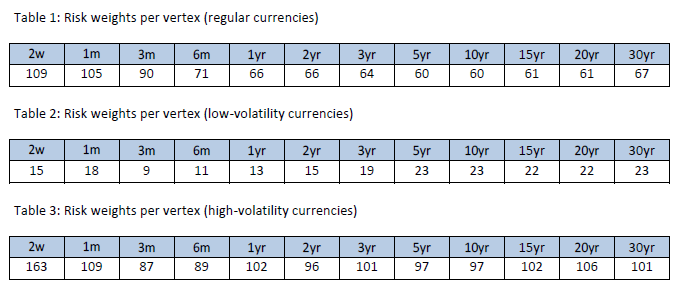

Interest Rate risk

- Risk-free yield curve risk weights are the same as v2.5a

- Inflation risk weight is 61, down from 63

- Cross-currency basis swap risk weight is the same

- Vege risk weight has increased to 0.23 from 0.18

- Correlations for risk-free yield curve tenors are all updated

- The correlation between inflation and interest rates is 24%, down from 37%, so less correlated

- The parameter for aggregating across different currencies is 32%, up from 24%, so more correlated

Foreign Exchange risk

- ZAR is dropped from high FX volatility currencies, leaving BRL, RUB, TRY

- Risk weight for regular volatility currencies is the same at 7.4

- Risk weight for high volatility currencies is up to 14.7 from 13.6 (calc ccy regular)

- While for high volatility calculation currency it is now 21.4 from 14.6

- (a large increase for agreements with calc ccy of BRL, RUB, TRY)

- Historical volatility ratio is 0.57, up from 0.52

- Vega risk weight a touch higher at 0.48 from 0.47, (note in v2.3 it was 0.3, so now 50% higher)

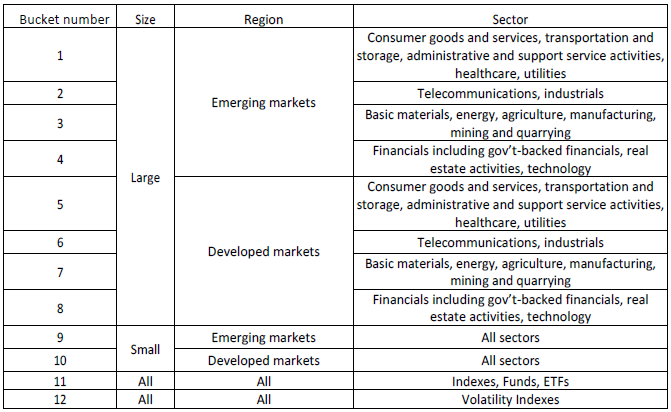

Equity risk

- Equity risk weights are higher for all Buckets except 6, Developed markets, Large, Telecoms, Industrials

- The largest increase is for Bucket 10, Developed markets, Small, All sectors, up to 50 from 32.

- Next is Bucket 12 for Volatility Indexes, also up to 50 from 34.

- Most other Buckets show an increase between 3 to 5, except a couple with 1

- The vega risk weight is not changed

- Correlations a touch lower for buckets 2-4 (Emerging Markets, Large), a touch higher for Developed Markets, Large)

Commodity risk

- Large risk increases in many SIMM buckets

- Coal risk weight is up to 48 from 27

- North American Natural Gas up to 30 from 24

- European Natural Gas up to 60 from 40 (and 22 before)

- North American Power down to 52 from 53

- European Power and Carbon up to 68 from 44 (and 24 before)

- Freight and Other up to 63 from 58

- Base Metals a touch up to 21 from 20

- Precious Metals the same at 21

- Gains and Oilseed up to 15 from 13

- Softs, Other Agricultural and Livestock, Dary the same at 16 and 13

- Indexes the same at 17

- Vega risk weight is down to 0.55 from 0.60

- Historic volatility ratio is up to 74% from 69%

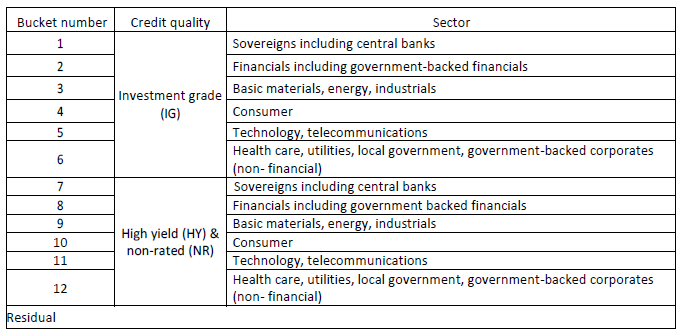

Credit Qualifying risk

- Risk weights all updated except for Sovereigns, which remains at 75

- Investment Grade (IG), Financials similar at 90 from 91

- IG, Basic materials, energy, industrials up to 84 from 78

- IG, Consumer and Technology/Telecomms down a touch

- High Yield (HY) and Non-Rated (NR) Financials down from 665 to 343!

- HY & NR, Technology/Telecomms up to 214 from 172

- HY & NR, Healthcare, Utilities, Local Government, down to 173 from 24

- Residual risk weight down to 343 from 665 (and 452, 333 and 250 in prior versions)

- Vega risk is similar at 0.76 compared to 0.74

Concentration Thresholds

There are many significant changes in concentration thresholds, so I will highlight only a few:

- Interest rate risk – Delta thresholds for regular volatility, well-traded currencies are increased to $330 mm/bp from $230 mm/bp, for regular volatility, less well-traded currencies increased to $130 mm/bp from $44 mm/bp.

- Foreign Exchange risk – Delta thresholds for category 1 currencies are decreased to $3,300 mm/% from $5,100 and category 2 currencies are decreased to $880 mm/% from $1,200

- Equity risk – Delta thresholds for Buckets 11-12 (Indexes, Funds, ETFs) is decreased to $810 mm/% from $2,100 mm/%

For the complete set of new thresholds, please see the ISDA SIMM v2.6 methodology document.

That’s It

SIMM v2.6 has all new risk weights and correlations.

We provide a short summary of the risk weight changes.

Interest rate vega risk with higher margin.

FX risk in BRL, RUB, TRY with higher margin.

Equity risk margin higher for most regions & sectors.

Commodity risk margin much higher for Coal, Gas and Power.

Credit risk margin lower for HY Financials and higher for IG Basic materials, energy, industrials.

Significant concentration threshold increases and decreases.

To get an accurate understanding of how margin changes.

You will need to run SIMM v2.6 on your counterparty portfolios.

CHARM and Microservices provide an easy way to do this.

Contact us if you are interested in this exercise.