- KCCP defines the amount of capital that must be held versus default fund contributions at a CCP.

- The lower the value of KCCP, the lower the overall cost of clearing.

- CPMI-IOSCO public disclosures show that KCCP has decreased at all of the major CCPs in the past three years.

- We look at the data and estimate some savings.

In a recently published CCP12 report, entitled “Incentives for Central Clearing and the Evolution of OTC Derivatives” the final section focuses on Default Fund Contributions at CCPs. This is an area that Amir has previously covered in his blog “Capital Requirements for Exposures to CCPs“. This week, I took a deeper look into these capital costs.

Thanks to CCPView and CPMI-IOSCO disclosures, I was able to use real data to see what has happened to the cost of default fund contributions at major CCPs.

KCCP – What is It?

Central clearing is capital efficient, and for many asset classes it is more capital efficient than alternatives (e.g. bilateral trading). No surprises there.

However, not immediately obvious is that Clearing carries a capital cost for default fund contributions. This is because a member has to fund (potentially mutualised) losses.

The calculation for how much capital has to be held against these default fund contributions is defined in bcbs282, “Capital Requirements for Bank Exposures to Central Counterparties”. A key component of the capital cost is the “hypothetical capital requirement of the CCP due to its counterparty credit risk“.

ONLY a CCP can calculate the KCCP figure.

Fortunately, the value of KCCP is now published quarterly via CPMI-IOSCO disclosures. These are available as part of a CCPView subscription.

The formula a CCP must use to calculate KCCP is as follows:

\( \tag {1} K_{CCP}= {\sum\limits_{CMi}{ EAD_i . RW . capital ratio}}\)Where;

EAD is the exposure at default for member i.

RW is a risk weight of 20%.

Capital ratio means 8%.

The value of this KCCP variable is a key factor in determining how much capital must be held versus default fund contributions at any given CCP. Let’s look at the data.

KCCP – What Has Been Happening?

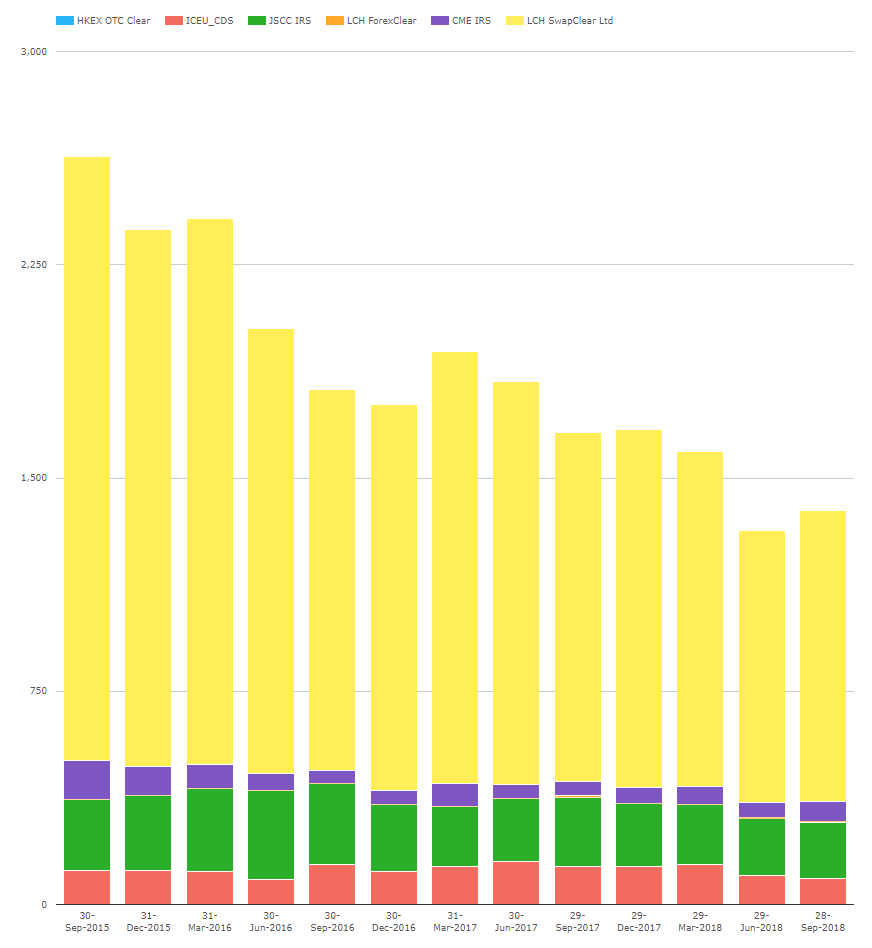

In CCPView, if you select “Disclosure 4.2 KCCP” you will see the following evolution over the past three years:

Showing;

Showing;

- KCCP values as reported via CPMI IOSCO disclosures for LCH (SwapClear and ForexClear), JSCC, CME (IRS), Ice Clear Europe and HKEX.

- The overall value across these 6 CCPs has reduced markedly in the past three years.

- The combined KCCP was 2,632 in September 2015.

- This has reduced to 1,386 in September 2018.

- This reduction has been seen across all of the CCPs.

- SwapClear 52% reduction

- CME IRS 49% reduction

- Ice Clear 22% reduction

- JSCC 21% reduction

This trend was highlighted in the CCP12 report, where they ask:

What could be some of the drivers of a drop in KCCP? Compression should help, as the larger percentage of trades at-market will reduce the credit exposure of a CCP to its’ members. Compression also serves to clean up the risk of a portfolio, generally reducing IM.

An increase in the market-level of long-dated interest rates may also have served to bring legacy portfolios closer to market.

All valid points, particularly about compression. This might suggest that compression will continue to flourish even in a SA-CCR world.

The CPMI-IOSCO disclosures also allow us to do more analysis.

Capital Requirement for CCP Exposures

Using the following formula from the BCBS paper, we can estimate the average capital requirement per member at any given CCP.

Capital requirement for each clearing member is given by:

Where

• KCMi – is the capital requirement on the default fund contribution of member i;

• DFCM pref – the total pre-funded default fund contributions from clearing members;

• DF CCP – the CCP’s pre-funded own resources (e.g. contributed capital, retained earnings, etc), which are contributed to the default waterfall, where these are junior or pari passu to pre-funded member contributions;

• DFi pref – the pre-funded default fund contributions provided by clearing member i.

This approach puts a floor on the default fund exposure risk weight of 2%. Below, we look at the evolution of each of these elements from the CPMI-IOSCO disclosures.

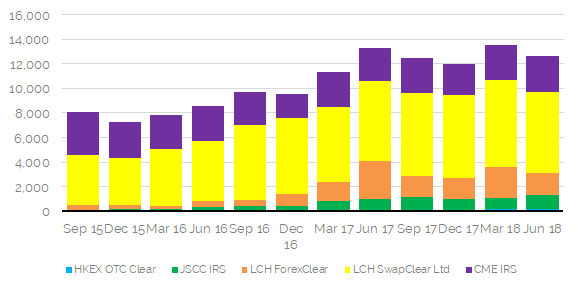

CCP Own Capital (DF CCP)

Looking at the evolution over time, we can see that the total amount of capital pre-funded by CCPs has stayed pretty constant.

Looking at the evolution over time, we can see that the total amount of capital pre-funded by CCPs has stayed pretty constant.

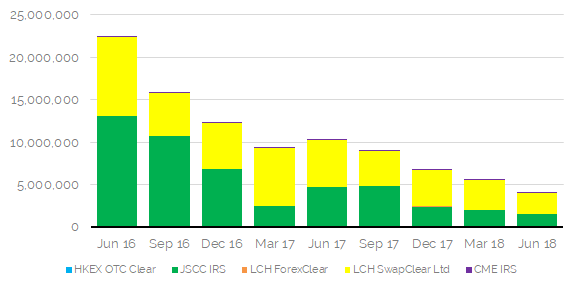

Total Pre-funded Resources (DFi pref)

However, the total pre-funded resources at CCPs have steadily increased. These two charts combined show that member contributions have therefore increased over the past three years.

However, the total pre-funded resources at CCPs have steadily increased. These two charts combined show that member contributions have therefore increased over the past three years.

Capital Requirements Per Member

Finally, we can combine the data points above with the public disclosures for the number of members each CCP has. This enables us to estimate the average cost of capital per member. The chart says it all:

Showing;

- The capital requirement associated with a given amount of a default fund contribution has reduced across CCPs. We choose to use a $20m pre-funded default fund contribution (DFi pref) in our example.

- For an “average” member, the cost has decreased significantly – by a factor of more than 10 for some CCPs!

- For JSCC, the increase in member contributions has significantly reduced the capital requirements at this CCP.

- Whilst for SwapClear, it is a combination of halving the KCCP value and seeing member contributions increase by 62% that has driven the overall fall.

A CCP has to strike a balance between member contributions and the overall cost of capital that pre-funded default fund resources entail. It is interesting to see in the data that there has been a consistent fall in KCCP across all of the CCPs, and a resultant reduction in the capital requirements for an average clearing member. This can only be good for the industry as clearing becomes cheaper.

In Summary

- KCCP largely defines the cost of capital associated with Clearing. It can only be calculated by a CCP, and these values are now made public via CPMI-IOSCO disclosures.

- Using CCPView, we are able to monitor the evolution of KCCP and other key CCP variables over time.

- We have witnessed a dramatic reduction in capital requirements associated with default fund contributions, reducing by a factor of 5 in the past two years alone!

- We believe that compression helps to reduce the value of KCCP.