- The US is introducing SA-CCR to calculate derivatives exposures in 2020.

- We look at the consultation.

- We compare add-ons under SA-CCR and the old CEM methodologies.

- Clarus offer FREE TRIALS of SA-CCR for Excel.

SA-CCR Consultation

The Federal Reserve, OCC and FDIC have launched a joint consultation on SA-CCR, the Standardised Approach to Counterparty Credit Risk.

The three agencies are proposing to introduce SA-CCR for the purposes of “calculating the exposure amount of derivative contracts under the agencies’ regulatory capital rule”.

This is consistent with the stated aim of SA-CCR from Basel which states that SA-CCR is:

A comprehensive, non-modelled approach for measuring counterparty credit risk associated with OTC derivatives, exchange-traded derivatives, and long settlement transactions.

This is a crucial aspect of the consultation (and SA-CCR generally) to understand and something I was initially confused about. This is about measuring derivatives exposures. It’s not about changing how much capital must be held versus a loan or mortgage for example.

Clarus offer FREE TRIALS of our SA-CCR for Excel software. Try it today!

Great – but I don’t get what SA-CCR actually is?

We’ve covered this in a couple of our popular blogs – including SA-CCR: Standardised Approach to Counterparty Credit Risk and SA-CCR: Explaining the Calculations. We also offer an Excel-based SA-CCR calculator, which should prove to be more popular than ever with this consultation. FREE TRIALS are available here.

The SA-CCR framework is designed from the off to be a more risk-sensitive way of measuring the Counterparty Credit Risk inherent in derivatives exposures. The methods it prescribes to measure OTC derivative exposures (cleared and uncleared), are used to measure regulatory capital requirements, such as Leverage Ratio.

If we rewind slightly, we can provide a little bit of background.

There are generally two approaches to measuring credit risk for derivatives;

- If you are a bank with more than $250bn in assets, you can go to your local regulator and ask for approval to use the Internal Models Methodology (IMM) for Credit Risk. This involves designing an in-house model that projects what your exposure to a counterparty (on a derivative) might be in the future across a number of different scenarios. As you can imagine, those scenarios will include a whole host of market data related to the risk factors of the trades (interest rates, FX etc) plus predictions on where credit spreads might go. This credit spread prediction is also based on market data – or based on at least comparable market data if the credit being considered doesn’t have a CDS market. . Assuming it’s a well designed, well understood model, your regulator will go through some assessments and hopefully give you IMM approval. We think only about the largest 12 US banks use IMM.

- Or, if you have less than $250bn in assets, you use the regulatory-prescribed model for measuring credit risk on derivative exposures. This is the Current Exposure Methodology at the moment. This consultation is proposing moving banks to SA-CCR by 2020. Banks use the standard approach if they are not huge, global banks.

That threshold of $250bn in assets is pretty large! This article suggests there are just 12 banks in the US with more than $250bn in assets.

So what exactly is the consultation about?

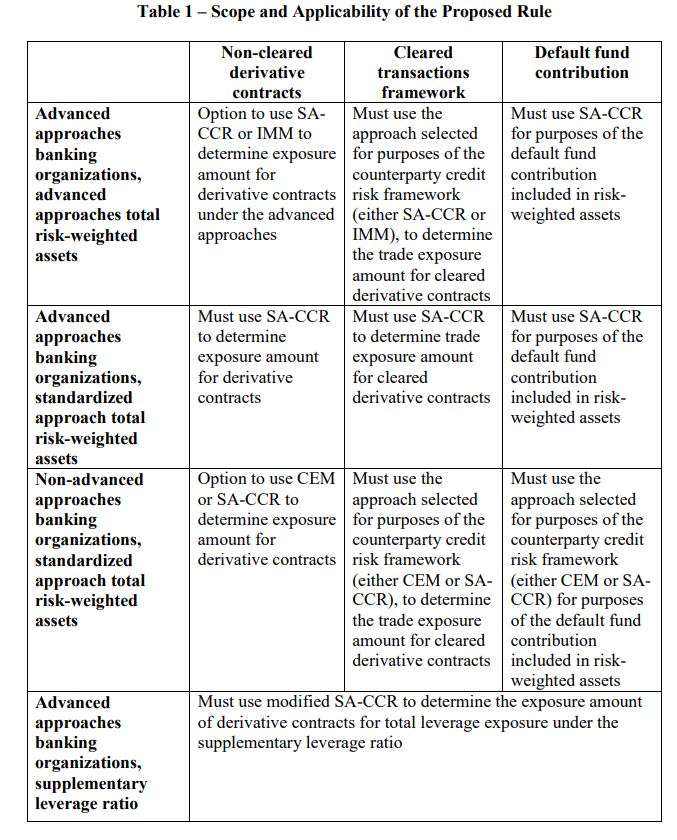

The consultation provides a good overview table of why this matters:

For those without the inclination to read a 248 page consultation (although you only need to read the first 91 really), there is a good summary from Bloomberg of the major points. And we’ll do our best below to give you some colour. In essence, this is about implementing a new Basel standard (not really so new, it was first written in 2014 with a view to implementation of 2017!). This Basel standard, SA-CCR, will now be used by all US banks to measure what their OTC derivatives exposures actually are.

Does this affect IMM banks at all?

Crucially, whilst the really large banks have gone through Step 1 and gained approval to be an IMM bank, this does not mean that they can use IMM for everything. As the table above sets out, it is prescribed by regulators that they must use the standard models for some aspects of regulatory capital requirements. These are:

- Supplementary Leverage Ratio. This is the big one. Everyone at the moment must use the Current Exposure Methodology to calculate their risk weighted assets for leverage ratio requirements (IMM is not allowed). This consultation will change those CEM calcs to SA-CCR calcs. IMM is still not allowed for this portion of regulatory capital.

- Default Fund Contributions. All banks above $250bn in assets must use SA-CCR.

Interestingly, banks with less than $250bn in assets will still be allowed to use CEM to measure their derivatives exposures for both cleared and uncleared. That seems a needless complication to support up to three methodologies.

Why is SA-CCR better than CEM?

Why would we go through the bother of introducing a new model to measure derivatives? The agencies put forward the following reasons:

Relative to CEM, SA-CCR provides;

- A risk sensitive approach to determining both replacement cost and PFE for a derivative contract.

- Improved collateral recognition – exposures are different depending on whether we have a margined or un-margined derivative.

- Recognition of meaningful, risk-reducing relationships for a balanced portfolio – i.e. it is not gross notional based.

- Capture of recently observed stress volatilities among primary risk drivers of derivatives – i.e. it was calibrated after 1995, when CEM was originally formulated!

And of course, relative to the Internal Models Methodology, SA-CCR is both accessible and standardised, as well as easy to understand. Even we can write a blog on it!

Some gritty details to impress your boss with

- SA-CCR calculations exclude XVAs.

- Replacement Cost is always floored at zero.

- When considering collateral held against a trade, we look at the net amount of Initial Margin. This excludes IM held at a CCP.

- For Rates trades, banks can choose whether to net across tenor profiles or gross up into the buckets.

- For Noncleared trades, the Margin Period Of Risk (MPOR) is floored at ten business days.

- For Cleared transactions, MPOR = five business days.

- For CSAs with more than 5,000 transactions. the MPOR= 20 days

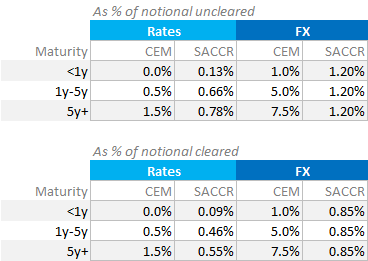

Your cut-out and keep SA-CCR vs CEM table

Finally, we need some idea of how CEM compares to SA-CCR, as this ultimately governs the change in Regulatory Capital. Here’s an overview on a standalone basis of Uncleared (top table) and Cleared (bottom table):

With all of the caveats that go with it:

- This shows an approximate comparison of PFEs under CEM vs SA-CCR, typically referred to as the “add-ons”.

- SA-CCR is maturity dependant, so will change every day with time to maturity. It is not grouped into crude maturity buckets like CEM.

- We have used 0.99y, 4.99y and 6y as our example maturities for SA-CCR.

- Uncleared calcs assume a daily collateralised zero threshold CSA is in place. This gives a Margin Period of Risk for a margined transaction of 10 business days.

- Cleared calcs assume a Margin Period of Risk of five business days.

- We assume full collateralisation, so a zero replacement cost.

- These are standalone trades; no netting is taken into account either within or between maturity buckets.

We think that the netting benefits of SA-CCR, rather than the absolute level of these “add-ons” will end up having the largest impact on portfolios. We therefore encourage you to check out our SA-CCR for Excel calculator to assess your own portfolios.