Last week a number of our readers alerted us to the sudden formation of a Basis in Yen Swaps between LCH and JSCC, which is interesting to say the least. So lets look at what the data shows.

Indicative CCP Basis Quotes

Tradition kindly sent us a screenshot of their new page.

Showing, Yen IRS dealer quotes at JSCC, an LCH/JSCC Basis bp and Yen IRS dealer quotes at LCH, with:

- 10Y IRS, the Basis is 1.75 bps

- 20Y IRS, the Basis is 3.25 bps

- 10Y Receive fixed at JSCC is 0.12% and Pay fixed is 0.08%

- 10Y Receive fixed at LCH is 0.1375% and Pay fixed is 0.0975%

Meaning that Dealers are quoting JSCC Cleared Swaps to Receive fixed at 0.12% and Pay fixed at 0.08%, so a customer can pay a fixed rate of 0.12% or receive a fixed rate of 0.08%.

While for an LCH Cleared Swap, a customer can pay a fixed rate of 0.1375% or receive a fixed rate of 0.0975%.

So it is better for a customer to receive fixed at LCH (0.0975% vs 0.08%).

And it is better for a customer to pay fixed at JSCC (0.12% vs 0.1375%).

Assuming of-course that the same liquidity exists at both CCPs.

And in that regard, we have had reports of sharply reduced volume at LCH last week.

Let’s look at whether we can find data to corroborate this.

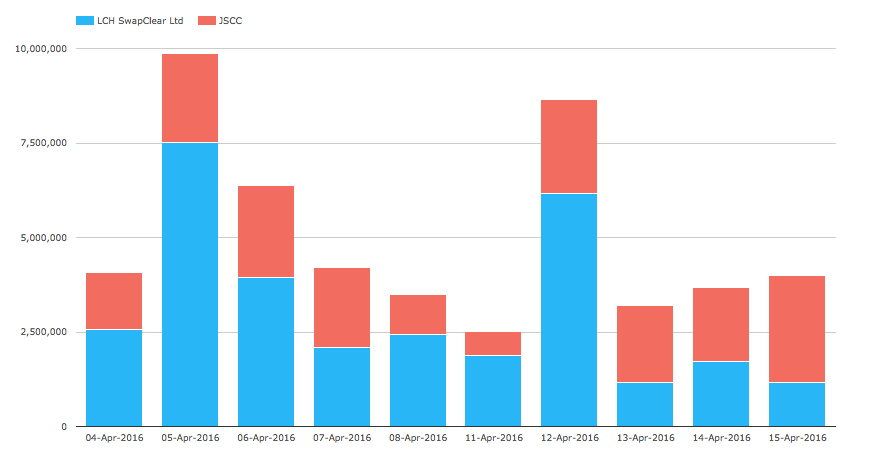

Clearing Volumes

Using CCPView we can look at the JPY IRS Volumes published by LCH and JSCC.

Showing:

- Daily volumes in millions of JPY for the past two weeks

- Certainly some big LCH days; 5 April and 12 April

- LCH volume is higher than JSCC on every day from 4 to 12 April

- JSCC volume is higher than LCH from 13 to 15 April

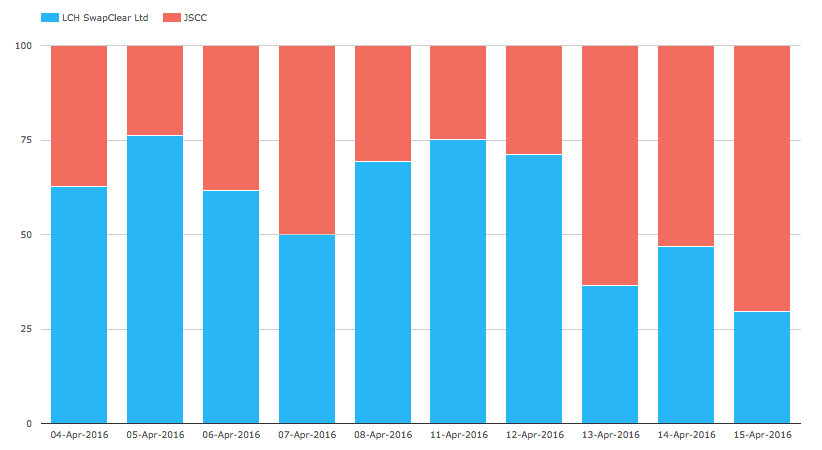

Showing the same chart as percent of total makes this even clearer:

Definitely looks like a significant change starting from 13 April 2016 with much lower relative volumes at LCH.

What other data can we look at?

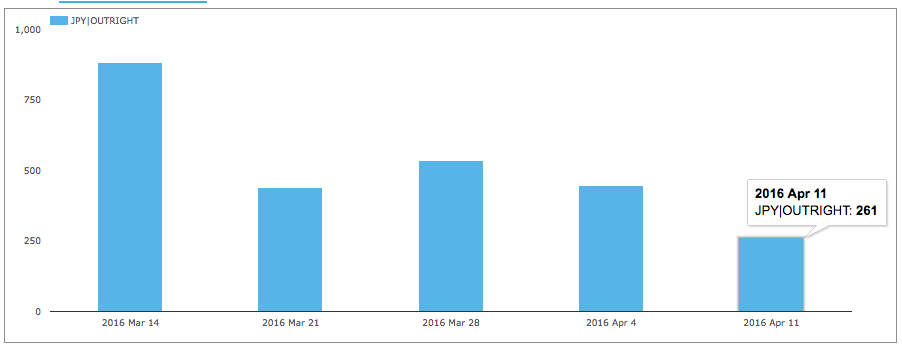

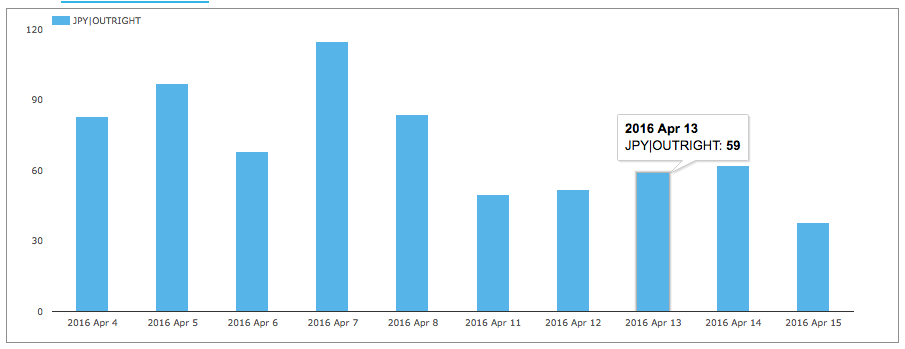

Swap Data Repository

In SDRView we can look at Cleared JPY IRS reported by US Persons to US SDRs (DTCC and BBG) and it is a reasonable assumption that these trades are all cleared at LCH.

Showing that the week starting April 11, 2016 is the lowest volume week, with only 261 JPY Swaps reported.

And the last two weeks by day.

The week of April 11 has lower trade counts each day, confirming what we saw in CCPView.

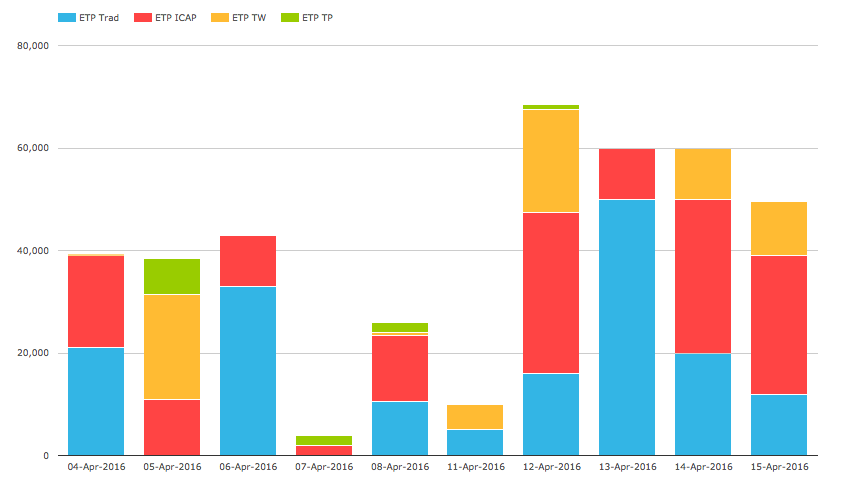

Japan ETPs

In SEFView we can look at the trades reported by ETPs in Japan, which are JSCC Cleared Swaps (5Y, 7Y, 10Y).

Showing JPY Notional in millions and higher volumes from 12 April onwards, backing up the increased JSCC volumes we see in CCPView. Further showing that Tradition and ICAP have the bulk of the volume.

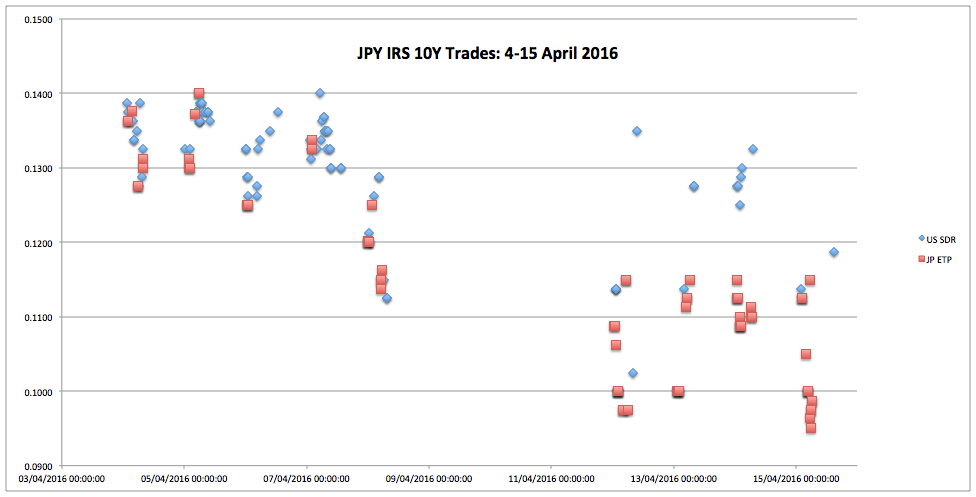

Combining US SDR and JP ETP

Now as both SDR and ETP have trade level data, we can also look to corroborate when the LCH-JSCC Basis appeared and the size of this basis, using actual trade prints.

We do this by extracting 10Y JPY Swaps trade executed between 4-15 April 2016 from both SDR and ETP, ordering the price prints by time (UMT) and producing the following chart:

The left-hand side is trade prices in the week of 4 April, while the right-hand is the week of 11 April.

Blue dots are US SDR, so LCH Cleared, while Red dots are JP ETP, so JSCC Cleared.

Showing that:

- The first prices are around 0.13 and 0.14

- With both red and blue dots at same levels

- So there is no evidence of an LCH-JSCC Basis in this week

- Starting late in the day on 13 April, we start to see differing prices

- On 14-April a number of prints at similar times, show the Basis to be between 1.5, 2.0 and 2.25 bps

- On 15 April, we only have one 10Y LCH trade and a price difference of 2 bps

Interestingly the trade data, sparse as it is, corroborates the Tradition quote of 10Y Basis at 1.75 bps.

Final Thoughts

In December 2015, I wrote a blog on CCP Basis Spreads: What Next and looked for evidence of a CCP Basis in non-USD Swaps and between other CCPs. In that article I looked specifically for an LCH-JSCC Basis and could not find one, but I postulated that one may arise at some time in the future.

We can see that only from 13 April 2016 onwards, has an LCH-JSCC Basis developed in Yen Swaps

The timing and reasons are not obvious.

However similar to the CME-LCH Basis in USD Swaps, it must arise for differing supply and demand dynamics.

We hear that JSCC volume is largely Japanese banks and with a greater preference to receive fixed.

While we hear that LCH volume in JPY is largely Foreign banks.

Outstanding notionals in Yen at both is large, with JSCC at $10.3 trillion and LCH at $7.5 trillion (8 April).

There must have been significant hedging by Dealers between the two CCPs.

We know what that scenario led to in USD Swaps at CME and LCH.

With volatility in the LCH-JSCC Basis higher than Outright rates, firms are now rightly being cautious.

Which has resulted in lower volumes at LCH.

It is early days with only a few days of data.

It will be interesting to see how prices and volumes develop this week.

JSCC introduced a change to their IM model on April 11 and this may have contributed to the sudden formation of the Basis. Will look at the details of that next week.

A few thoughts on your conclusions:

There was a change to JSCC’s IM calculation methodology this week – relative to absolute shifts.

LCH got their license to clear for direct members from Japan (effectively from Monday) – although only non-JPY IRS at the moment but perhaps raising the expectation of clearing JPY in the future.

Looking at:

Obviously JSCC is always flat, so going back to my earlier comments, it may be an anticipated change in access to LCH by Japanese banks that’s the main driver here. As you say, prices and volumes through the remainder of this week will give a better idea of what’s really going on.