What is most traded – Spot, Fwd, or IMM swaps? Or maybe MAC? Ahead of the MAC coupon change on February 2nd, we examine some of the bifurcations that exist in the USD swaps market at the moment.

Liquidity

We’ve talked about Liquidity before, and of course there has been a lot of commentary surrounding where swaps are trading – particularly relevant if you run or own a SEF platform! But this week, we’ll examine an aspect of bifurcation that we see in markets. This can be summarised as which products trade where.

This line of analysis has resulted from a couple of queries that our clients have sent in over the past couple of months, which can be summarised as “If I want to trade X, where should I trade it?”. That’s a subtle hint that if you are trying to make sense of some numbers, please feel free to reach out to us….

Product Coverage

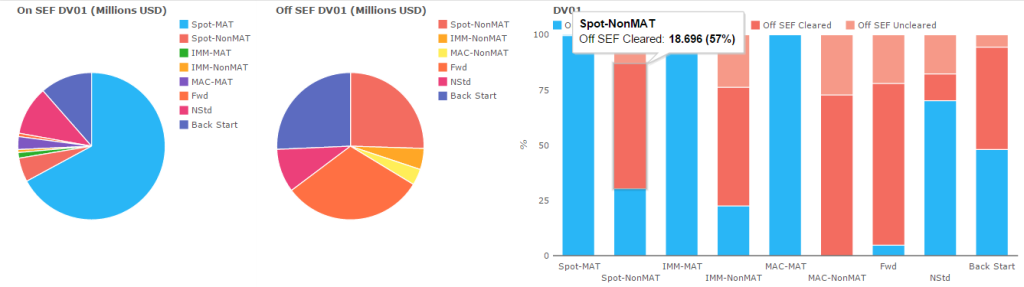

In SDRView Researcher, we produce a daily and weekly summary of the swap subtypes that trade. The below charts show the DV01 in USD swaps that traded for the week-ending 23rd January 2015:

Highlighting that:

- For USD swaps, over 67% of On-SEF DV01 was from Spot starting products that have been “Made Available to Trade” (MAT – Tod has written plenty on the subject, so please have a browse of his blogs on the right hand side if you want a refresh).

- Off-SEF trading saw a pretty fair split between Back-Start swaps, Forward start swaps and the Spot-starting structures that have not yet been “MAT’d”.

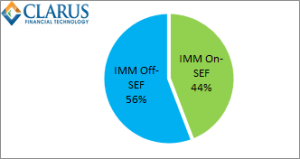

- In addition, in the right-hand panel you can see that of the Spot starting, nonMAT trades, 57% by DV01 were traded off-SEF and were cleared. So if you have a funky Spot trade to do – for example, against a strange index, a non-standard day-count convention or a very particular maturity date, you will likely find more liquidity by picking up the phone and trading off-SEF through old-school bilateral channels.

Pre-Trade versus Post-Trade

Is the above analysis too focussed on the post-trade world, however? If you have a view on 10 year rates, does it help you to decide whether to trade IMM, Fwd, MAC or Spot? And if you are venue-constrained – e.g. you have to trade on a SEF, or conversely, you are European and want to avoid trading on a SEF – should the choice be different? These are the angles some of our clients have been coming at – they know whether a swap is MAT or not, and equally whether the execution mandate applies to them. Therefore, pre-trade, what they also want to know is which products have greatest liquidity, as well as which venues.

Step-by-Step

There is a two-step process to arrive at the final conclusion, so please bear with the baby-steps approach that is coming up. First off – let’s separate the trading world into product types that are relevant pre-trade: IMM, MAC, Fwd or Spot. If it’s a back-start trade you want to trade, then the economics can be different due to compression and line-item efficiency, so let’s ignore those trade types.

If the execution mandate does not apply to you, do you want to trade on-SEF? From a pure liquidity point-of-view;

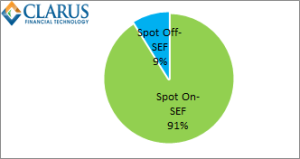

For Spot trades, there is a compelling answer to this – YES:

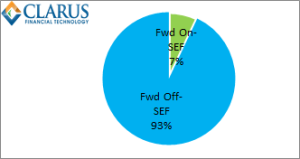

For Fwd trades, NO:

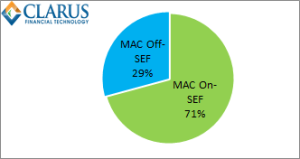

MAC is unsurprisingly titled towards the SEF Universe:

Whilst IMM is a close-tied thing:

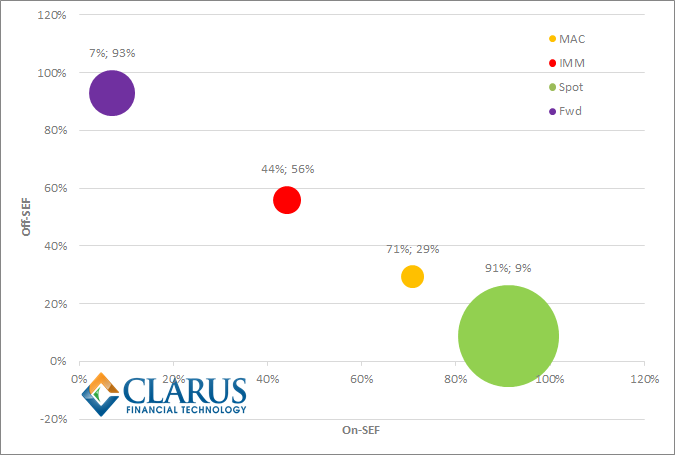

However, this doesn’t tell you what the relative liquidity is between Spot, Fwds, IMM and MAC. If I am a prudent investor, I might just want the product that has the tightest bid-offer spreads, and is most widely traded. In which case, you need to take a careful look at the chart below. We show the proportion traded on-SEF along the X axis, proportion traded off-SEF along the Y axis, and the size of the bubble represents the total DV01 traded in 2015:

I think that is a pretty neat representation of what you need to see pre-trade. It shows:

- Spot starting trades are the most liquid products (large, green bubble). If you want to trade Spot, do it on-SEF as an overwhelming 91% of DV01 goes across a SEF.

- Fwds are the next most-liquid products. However, probably because SEF’s do not list all of the possible combinations, liquidity is focused off-SEF in an almost mirror image of Spot trading.

- For IMM and MAC, they represent more specialised structures and less liquidity overall. IMM structures currently see more risk traded and are more balanced between SEF and non-SEF venues.

- In terms of total risk traded, the comparative sizes of the bubbles show the following split by DV01:

- Spot 75%

- Fwds 15%

- IMM 6%

- MAC 4%

Of course, this analysis comes with certain caveats. As always, we are dealing with a particular universe of reporting counterparties, plus we only see capped notionals – with the possibility that some products may be better suited to block trading than others. For example, the total uncapped notional reported in SEFView for MAC products is $1.6bn higher than the capped amounts reported in SDR. In practice, this small difference is unlikely to change the relative liquidity ranking of each product. For now, we have a landscape that has 75% of liquidity in Spot starting products, 15% in Fwds and the remainder evenly distributed between IMM and MAC products.

As of 2nd February, we will have new MAC coupons. It will be interesting to see how the fledgling MAC-market will cope with this bifurcation – we will therefore update the analysis in due course.

Hi Chris,

Great analysis!

What was the pre tense behind the MAC coupon changes? The link displays the longer dated USD coupons were adjusted down. My understanding is a joint committee supervised by ISDA/SIFMA sets the coupon rates for the fixed side.

Thanks,

Ken

Hi Chris,

From Tod’s blog, he mentioned coupon blending would be helpful for IMM (but not MACs) swaps – is this referring to swaps that coincide with start dates that are the 3rd Wednesday of a quarter or is there a different interpretation for IMM swaps. Appreciate the clarification.

Thanks,

Ken