Last month I wrote about the potential for a very non-linear transition when LIBOR is discontinued.

This was also covered in a recent Risk article: ‘Beware the cliff edge in Libor fallbacks’. The impending announcement on the timing of LIBOR cessation process was covered by Chris Barnes earlier this month, Also with the potential for IBA to soon conduct a consultation on LIBOR cessation, the focus is really starting to turn to the actions needed from now until the end of 2021.

This blog looks at the potential scenarios in the last months of LIBOR before the cessation which is expected at the end of 2021.

It is important to consider a range of outcomes to properly stress-test portfolios and adjust limits and/or trading intentions if required.

Benign transition alternative

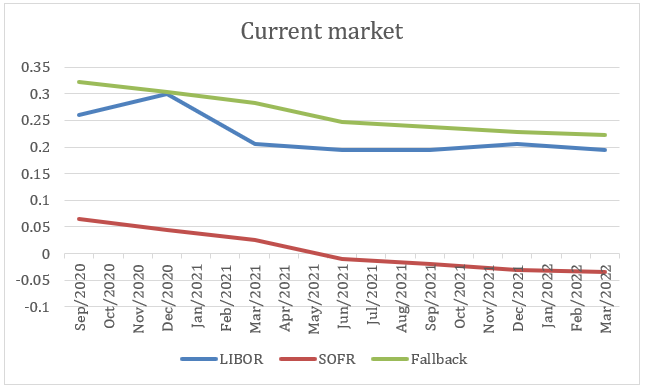

Markets are currently pricing a smooth transition from LIBOR to SOFR and SONIA between December 2021 and January 2022.

The following chart shows the 3-month USD LIBOR and SOFR. Also, the green line is the fallback rate calculated from the SOFR and the Spread adjustment.

Although the LIBOR and fallback rates are quite similar, they are not identical. This can arise from projected Bloomberg spreads and assumptions about the potential trajectory. Either way, the rates are quite similar and converge nicely between now and the end of 2021: there is no appreciable cliff event in December 2021.

Not-so benign alternatives

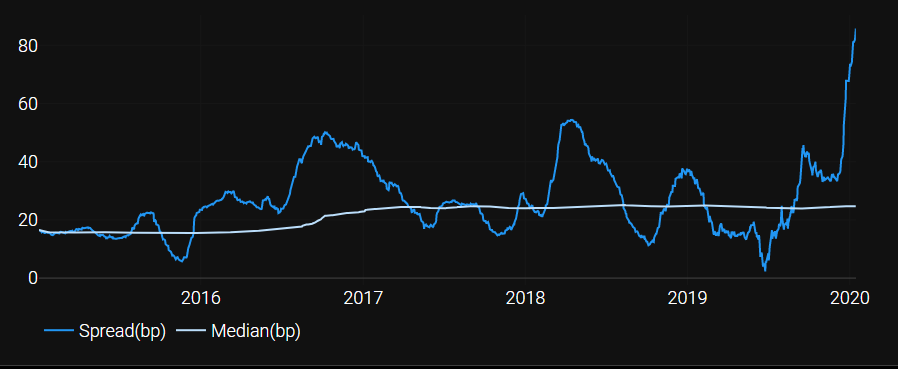

However we know that the actual spread does vary considerably and often from the 5-year median (grey line) which is the Spread adjustment (see charts below).

The March 2020 spike and the slow decay into June 2020 is a feature of a fast-changing market where the LIBOR looks forward while the SOFR looks back. This well-known effect stems from timing mismatch between the two.

This is most obvious in the 3-month spread (due to the longer tenor) but is also clear in the 1-month chart.

If the benign run into the end of 2021 does not play out as predicted, what could the fallbacks look like?

Outcomes in a less benign world

I have looked at some of the extremes in the recent 5 years for USD and how this may impact valuations before and after the cessation event.

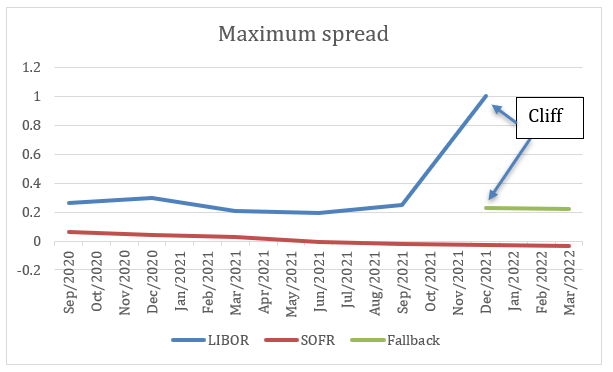

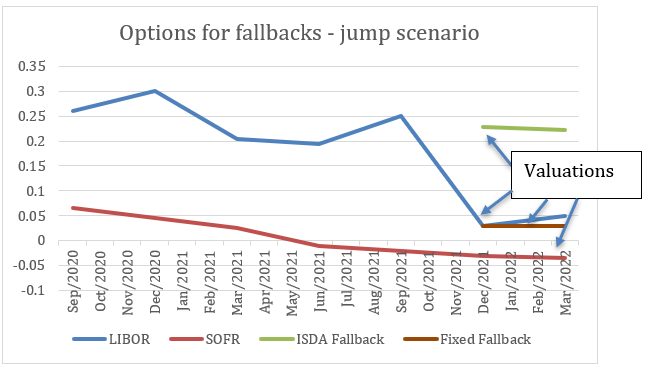

Firstly, what if the spread is at a maximum? This is shown in the following chart for 3-month USD.

LIBOR is around 1% on 31st December 2021 but it ‘falls back’ to just around 23 bps on 3rd January 2022. Now that is a cliff!

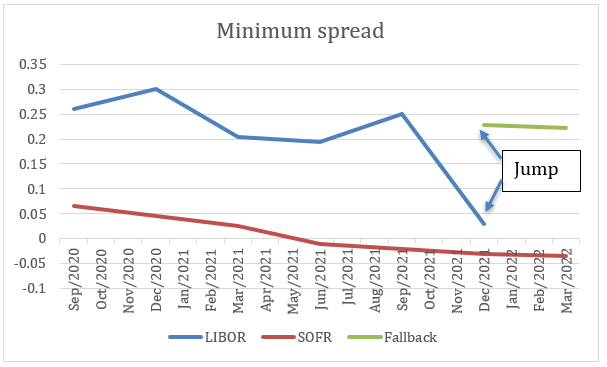

In another case, a minimum spread looks like this:

LIBOR is around .03% on 31st December 2021 but it ‘falls back’ to around 23 bps on 3rd January 2022. Now that is a jump!

Both these events have happened within the last 5 years and could become a reality again in December 2021.

What could a prudent risk manager do?

I outlined a few options in my last blog. These are:

- Include a cliff (or step) function in revaluations for derivatives to be used if required;

- Add some scenarios to estimate the potential valuation outcomes in positive and negative cliff events; and

- Manage rate fixes before and after the assumed ISDA trigger date (currently sometime in January 2022).

However, most banks are also required to stress-test their portfolios and report the results regularly to regulators. Modelling step functions (cliff edges) is often challenging but will need to be done to properly represent some scenarios around LIBOR cessation.

So, I have added to the list above with:

- Consider the stress tests used in portfolios subject to LIBOR cessation; and

- Add the step functions (cliff) as required.

One way to do this is using Clarus Microservices. This set of tools can be used to provide the valuations for trades or portfolios through a potential cliff event.

What about the buy-side?

Apart from their internal portfolios, many banks have customers who have exposures to LIBOR and therefore the cessation event. The buy-side has a similar risk to the cliff event and needs to see valuations and scenarios to assist with decision making.

Generally, the buy-side has at least 4 options:

- Do nothing and accept a potential ‘zombie LIBOR’ or the current fallbacks in contracts;

- Incorporate the ISDA fallbacks in contracts;

- Incorporate other, non-ISDA fallbacks (e.g. last LIBOR, common in debt issues); or

- Move straight to RFRs like SOFR.

These options could all have different valuations at the time of renegotiation. And they will almost certainly have different outcomes at the time of LIBOR cessation.

Buyer’s regret

With at least four alternatives for LIBOR after a cessation event (and many more in option 3 ‘Other’) there is a risk of choosing the wrong one based on valuations after the renegotiation – buyer’s regret.

Clarus Microservices offers an easy way to value the alternatives at the time of a renegotiation and create different scenarios for outcomes.

The scenarios are very important because they give a range of potential outcomes from now until cessation on a nominated date. This will help in making informed decisions about the alternatives.

And don’t forget to consider appropriateness. For example, if a derivative is used to hedge a specific risk it is usually better to match and offset the two exposures.

For risk management and stress testing, Clarus Microservices can also be used to check scenarios and valuations in an easy and accessible format.

Summary

The cliff event is a real risk which needs to be considered when making a decision on alternatives for LIBOR post cessation.

A decision to use a particular alternative, remembering there are at least four basic types, will have consequences now and at the time of cessation. There can be different valuations now as well as in the future.

Look at the valuations and the scenarios while matching the risk to the hedge.

And make sure you are well informed by using an independent valuation service like Clarus Microservices.