- LIBOR will probably see an announcement towards the end of this year that it will be discontinued.

- This was announced by the FCA on 22nd June.

- This has moved markets already because it impacts the dates to be used to calibrate the fallback spreads.

- This means that we have already seen the last 6 month LIBOR fixings that will impact the calibration of these spreads.

- The largest impact appears in single currency tenor basis spreads.

Wow, I started this blog thinking I’d throw something out there about the large volumes in 3s6s basis we saw last week.

Little did I realise that I would end up down a (quite fascinating!) rabbit’s hole of pre-cessation triggers and the realisation that we may have already seen the last relevant 6 month LIBOR fixings! Who knew?!

You would think that this would be bigger news around these derivative parts….?

WTH? LIBOR Is Still Around, Right?

Yes, LIBOR is still being published, and we expect it to continue to be published all the way until end of 2021.

However, it looks like we will have a pre-cessation trigger as at the end of THIS YEAR (this side of Christmas 2020 to be precise).

This announcement regarding “pre-cessation” came last week (June 22nd) during the Risk.net webinar below:

So what happens now? According to the ISDA documentation I read last year, I think that the five-year median observation period for the spread adjustment is now therefore pretty much set in stone. It will run from:

- Pre-cessation announcement date minus one business day defines the Spread Adjustment Fixing Date.

- Any LIBOR fixing with a period end-date up to the Spread Adjustment Fixing Date will contribute to the five year median spread adjustment calibration.

- However, that means that any 6M LIBORs published in the prior six months, (and 3M LIBORs published in the prior three months etc), will be excluded from the calibration. This is to prevent potential market moves in the RFRs themselves as a result of the pre-cessation announcement.

This was made clear in this ISDA consultation last year:

Because the long-run spread adjustment will compare data for the relevant IBOR over each relevant tenor and data for the relevant RFR compounded over a time period with the same length as the relevant tenor (for which data will not be available until the end of the relevant period), the historical data used will not include the most recent published IBOR data. This is

because data for the relevant RFR may not be available for the entire relevant period if that period extends beyond the date on which the fallback trigger event occurs. This also will ensure that any data for the relevant RFR after the fallback trigger event has occurred would not be

affected by knowledge in the market of the fallback trigger event. Thus, for example, if the tenor referenced for the relevant IBOR is 3-months, then the last IBOR publication used as a data point for the purposes of calculating the spread will be for a date at least three months before the fallback trigger event occurs.

ISDA Consultation on Final Parameters for the Spread and Term Adjustments in Derivatives Fallbacks for Key IBORs

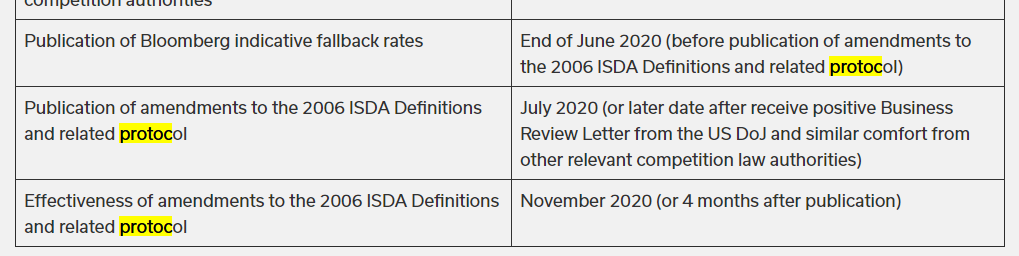

To be clear, we now expect to be given notice in November or December 2020 that LIBOR will discontinue at the end of 2021. This expected pre-cessation announcement sets in stone specific dates for how the parameters for the fallback spreads will be calibrated.

Listening to the webinar again, I think the discontinuation announcement will come as soon as possible after the ISDA protocol closes (to allow market participants to sign-up to the fallbacks themselves). According to the ISDA website, this protocol is expected to close in November 2020:

Tenor Basis Market

As a result of this announcement, we saw some fascinating moves in tenor basis markets (and significant volumes).

These moves were seen in both GBP and USD markets:

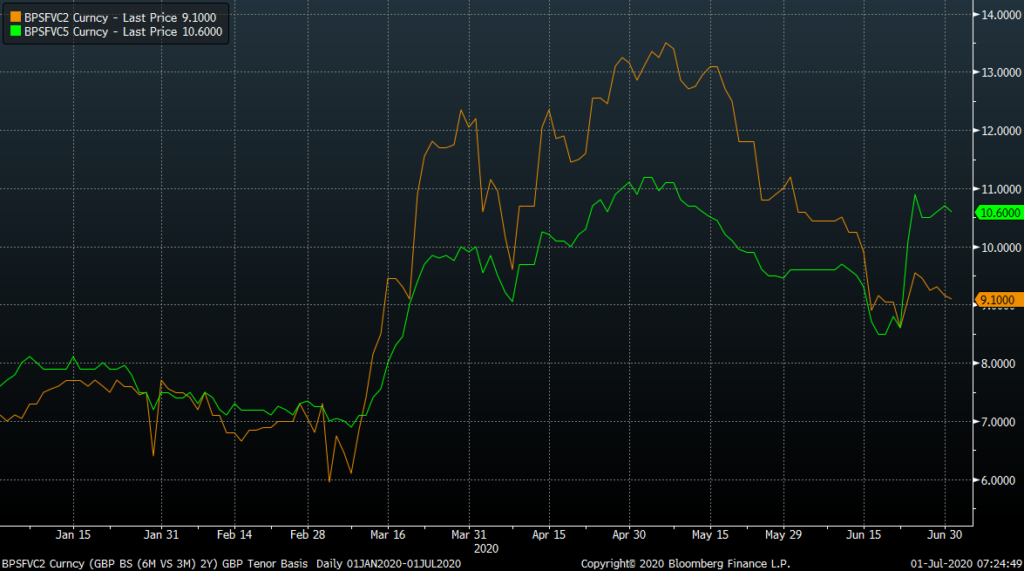

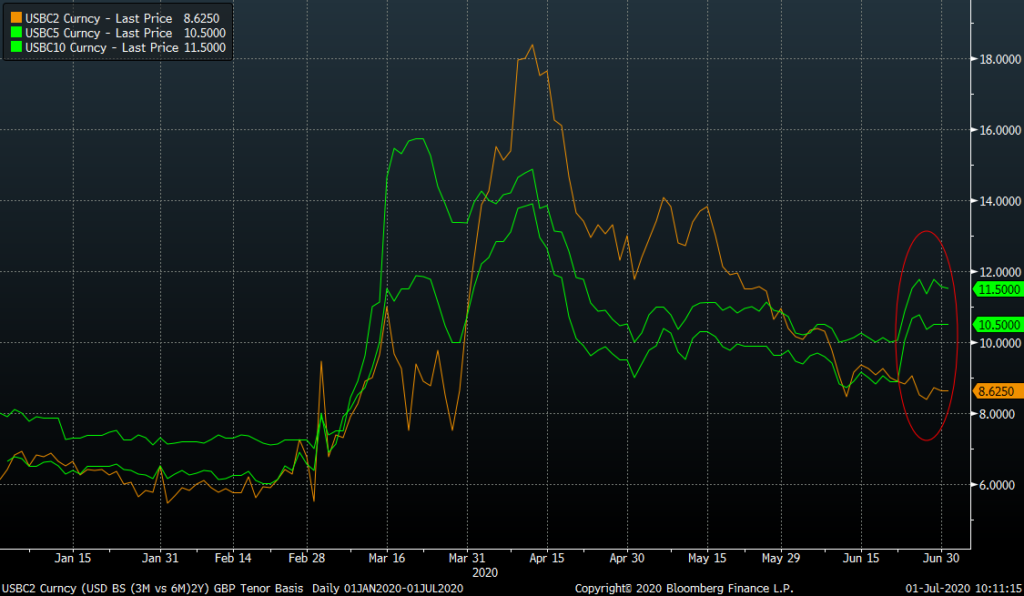

Courtesy of Bloomberg, the chart shows;

- 3m vs 6m tenor basis in GBP since the start of the year for 2Y and 5Y maturities.

- The 23rd June saw a sharp jump higher of 2 basis points in 5Y 3s6s.

- This was replicated in all tenors longer than 3 years.

- However, 1Y and 2Y 3s6s hardly moved.

Anyone familiar with tenor basis will be surprised that the short-end didn’t move. However, this is due to the impact of the fallbacks on the forwards. What has essentially happened is:

- A 1Y GBP 3m vs 6m LIBOR tenor basis swap will NOT be affected by the fallbacks. Both 6M fixings (and all 3M fixings) will be as per published LIBOR rates up until the end of 2021.

- A 2Y GBP 3m vs 6m LIBOR swap traded today (30th June) will have all four 6M LIBOR fixings applied as normal. This is because the final 6M fixing is taken six months prior to maturity (i.e. the fixing date is 30th Dec 2021).

- However, trade any swap longer than that, and you are into fallback territory for all but the first four 6M LIBOR fixings.

- This theory was distilled in market moves, where we now know the dates for the spread calibration once the fixings “fallback”.

And that final point is what makes it so interesting. 3M vs 6M tenor basis used to be a forward-looking measure. It was a credit and short-end rates play. 6M fixings represented rate expectations for a 3×6 forward starting FRA, plus any credit compensation required for lending unsecured funds for an 3 extra months.

Post fallback, what is a 3M vs 6M tenor basis? It is now a backward-looking spread, measuring the realised spread of a 6M fixing versus the actual RFR fixings over that same period of time.

The 3s6s basis curve has therefore been made up of two years of forward-looking measures, then an abrupt cut-off for any fixings after 31st Dec 2021, which revert to a backward-looking, realised measure of RFR fixings. This has been the case for a while now. However, the parameters for the calibrated spread after 2021 have now been more closely defined, so we can accurately forecast what the spreads will be.

The Calibrated Spread

It is worth noting that the calibrated spread between 3M and 6M LIBOR rates for a given currency will be constant in perpetuity from 1st January 2022.

No longer will this spread fluctuate each day as credit is repriced or rate expectations change. It is a fixed spread. For ever. So whilst we do not know what the RFR rates will be that create each individual period, we do know that the realised RFR rates for the 6M period and the two 3M periods will be the same. This also means that 3M and 6M LIBORs become effectively fungible risks after this date.

Why Did The Market Move?

For 6M LIBOR, we can assume that the last possible fixing taken into account for the five year median period was 18th June 2020. This assumes a latest possible pre-cessation announcement of 18th December 2020 from the FCA (the end date of a 6M LIBOR fixing 18th June 2020).

Working backwards:

- Five years of history prior to 18th June 2020 puts us at 18th June 2015 for the start of the calibration period.

- Previously, the market appeared to be assuming that this calibration period would be more like June 2016 to June 2021.

Now the slight unknown, using GBP markets as an example:

- We don’t know exactly where SONIA will fix every day until 18th December 2020. Particularly given prior speculative trading around negative rates in the UK.

- However, absent any rate moves, we can pretty confidently say that SONIA will continue to fix around 6.5 basis points, as it has every day since April.

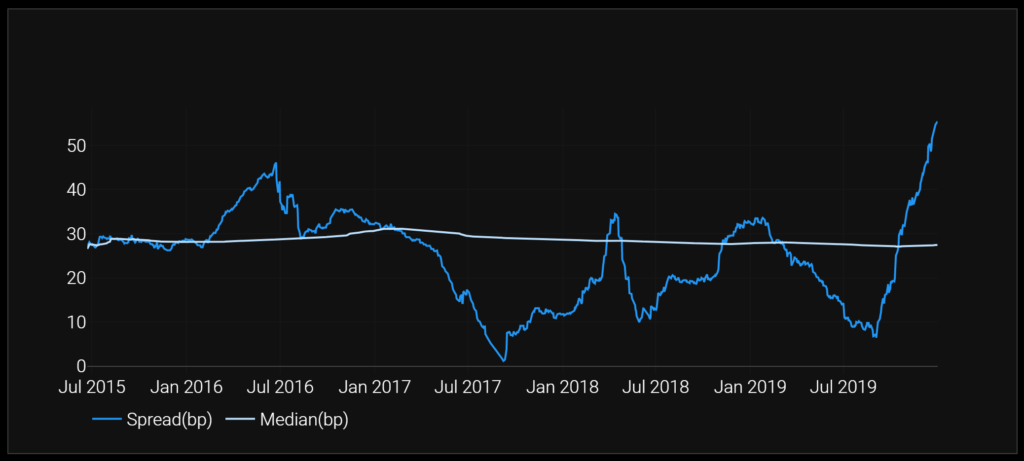

You can see from our IBOR Fallback app from CHARM, that the daily spread of 6M GBP LIBOR versus realised SONIA has been increasing as a result of the unexpected rate cuts in March:

The final (known) data point comes from the high point of GBP LIBOR 6M fixings (around 88bp) from the turn of the year. The question for the future calibration will be how quickly those 6M fixings dropped relative to the speed with which SONIA dropped each day.

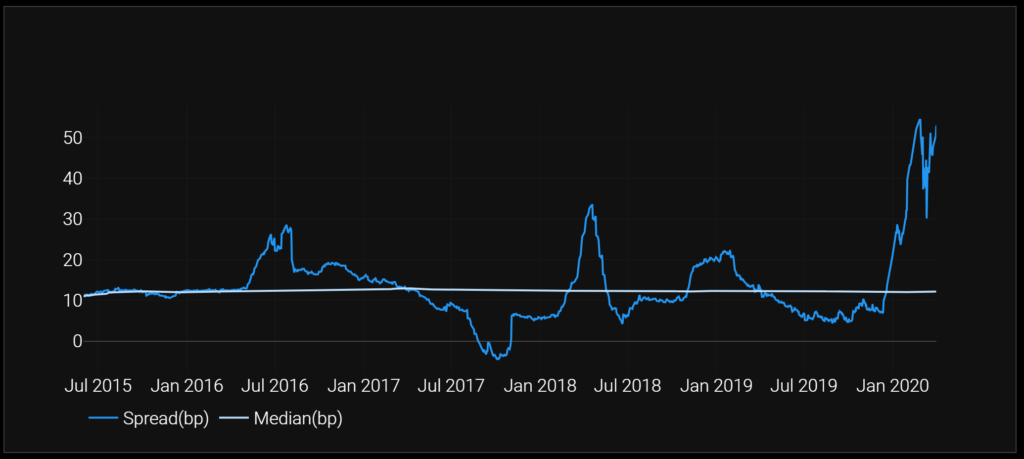

From a 3s6s basis perspective, we can already see the effect on the 3M LIBOR spread of these unexpected rate cuts:

To complete the analysis, expect market participants to be projecting forward the daily spreads versus a realised SONIA fixing of 6.5bp until December.

Struggling with your own analysis? Contact us to subscribe to our IBOR Fallback App.

USD 3s6s

The same can be said for USD markets – and the 3s6s also jumped in 5Y and 10Y tenors here:

However, whilst SONIA fixings are somewhat predictable, SOFR continues to be a different animal. Since the market volatility in March, SOFR has already increased from 1bp to 9bp. Absent a decent forwards market, I’m not sure what the market will be using to project the SOFR forwards to anticipate the calibration in USD? CME SOFR futures maybe?

CHF and JPY 3s6s

I’ve not completed the analysis for CHF and JPY yet. Are the spreads in 2015 different to those anticipated in 2020? I will leave it to our subscribers to use our IBOR Fallback App to complete their own analysis.

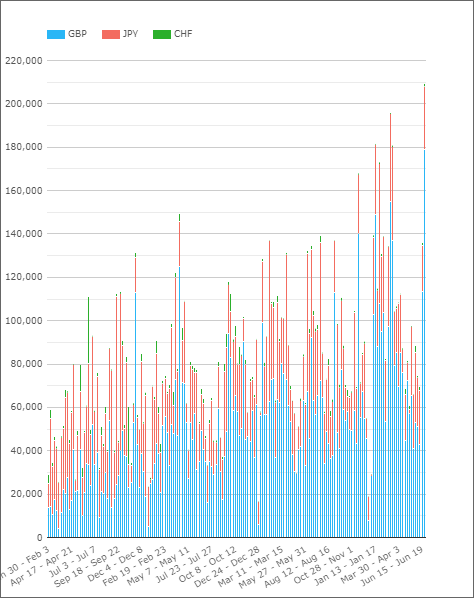

How Much Traded?

Last week saw all time record volumes traded for GBP, CHF and JPY single currency tenor basis. CCPView shows the cleared volumes traded last week:

Showing;

- Volumes topped $200bn equivalent in a single week for the first time ever last week in cleared basis swaps for these three currencies.

- These basis swaps cover all flavours of single currency tenor basis swaps:

- OIS vs LIBOR

- 3m vs 6m

- 1m vs 3m etc

- The chart excludes USD because the volumes in this currency are far more volatile than others.

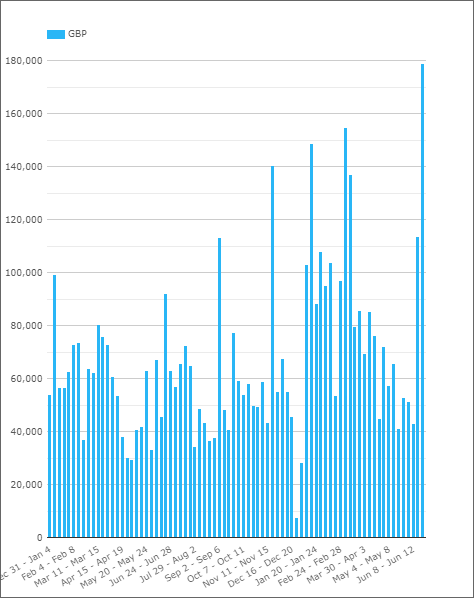

Much of the volume spike was in GBP, as can be seen, where $180bn traded:

In Summary

- There was a forceful recognition from the FCA that a discontinuation announcement of LIBOR will come in the run-up to Christmas this year.

- This allows market participants to accurately calibrate the fallback spreads for LIBORs.

- We have already therefore seen the final 6M LIBOR fixings that will be used to calibrate fallback spreads.

- The biggest market impact from this announcement is on single currency tenor basis.

Even though Mr Schooling Latter did indeed use the risk.net LIBOR virtual week to talk about the possibility of a pre-cessation announcement before the end of 2020, as far as I was concerned (from listening into the discussion) he only left this as a possibility and declined to comment on whether any decision had already been made or whether there was any “agreement” between the FCA and IBA regarding pre-cessation. As usual, the market is taking on board the additional information from Mr Schooling Latter but we shouldn’t leap to firm conclusions around any timing for pre or permanent cessation.

Brilliant, many thanks for clarifying Ben. I thought he was fairly unequivocal on the webinar, but I clearly need to listen to it again!

I have to say I share Chris’s interpretation of Edwin Schooling Latter’s comments. From 4:30 in the webcast he says that announcements confirming the end of LIBOR from end-2021 “could” come as early as November / December. It is hard to know whether “could” refers to the fact of a pre-announcement or its exact timing. But he goes on to say there “will” need to be further announcements ahead of the end of 2021 and that “it is entirely plausible that you could see announcements about discontinuation in the final weeks of this year.” Later (52:09) he says that “market participants need to be ready for announcements on what will happen at the end of 2021 towards the end of this year.” While there is a small element of ambiguity in his choice of language, the comments, taken together, come very close to a definitive statement that there will be a pre-announcement before year end. It seems clear that this will be based on confirmation from a sufficient number of panel banks of their intention to withdraw as to make a declaration of unrepresentativeness at or around end-2021 a certainty. It was a odd choice of forum in which to make such a significant statement (and I mean no disrespect to risk.net which did an excellent interview and got something of a scoop).