- We take a look at the cost of carry in Interest Rate Swap trading.

- We analyse both 2y vs 10y curve trades and a simple spot starting 10y trade.

- We also take a brief look at exchange traded derivatives to estimate the carry on short-term interest rate futures.

- Positive carry trades can provide a strong motivation to pursue a particular trading strategy.

The Steamroller Trade

“Carry” trades are somewhat infamous trading strategies that are sometimes akin to picking up pennies in front of a steamroller. This is not necessarily true all of the time, and it is true to say that all portfolios must carefully consider the impact of carry on trading decisions and portfolio structure.

“Carry” trades are somewhat infamous trading strategies that are sometimes akin to picking up pennies in front of a steamroller. This is not necessarily true all of the time, and it is true to say that all portfolios must carefully consider the impact of carry on trading decisions and portfolio structure.

This blog will focus on Interest Rate Swaps and exchange traded interest rate futures.

What is Carry?

We define Carry as the Profit (positive carry) or Loss (negative carry) of a trading strategy as a result of doing nothing. In other words, if Rates were to stay identical from one day to the next, what is the result of the passage of time on your trading strategy?

What Causes Carry?

Carry is created in two ways for an interest rate swap:

- The differential between short and long-term interest rates. If LIBOR 3m is fixing at 0.5% but the 10 year swap rate is at 3.0%, I can earn 2.5% of the notional every 3 months in positive carry by choosing to receive fixed in the 10 year swap. Whoop, that sounds like free money!

- In one month’s time, my 10 year swap will still have a coupon of 3.0%, but it will now be a 9y 11 month swap. If the 10 year swap rate is still at 3.0% my off-market swap may well be in the money simply thanks to the passage of time.

How do we measure Carry?

Carry is easiest to conceptualise when thinking of forward starting structures. The classic example tends to be a 2s10s spread.

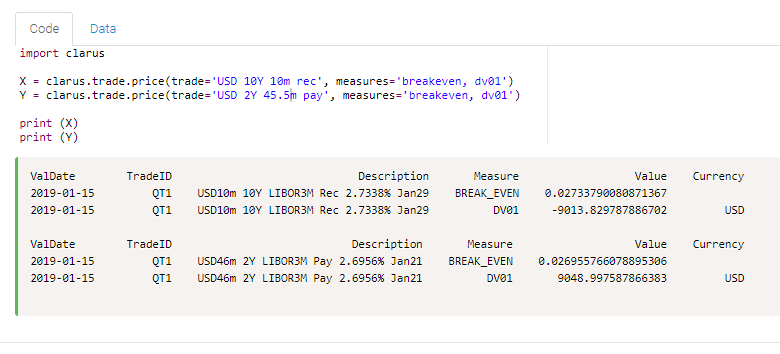

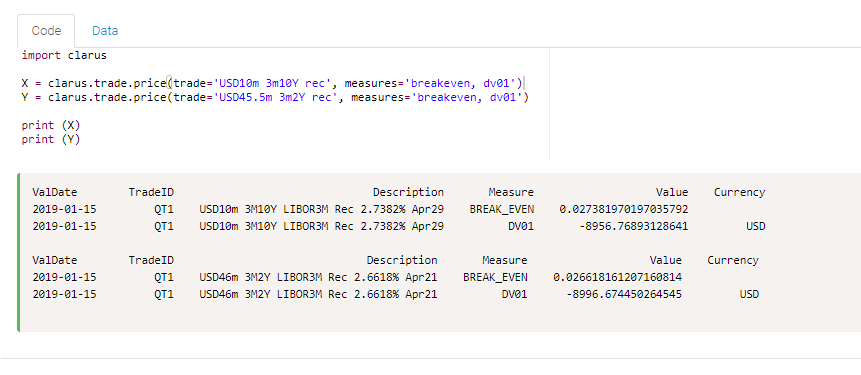

In USD, out of spot we see in our Microservices the following analysis:

2y at 2.696% and 10y at 2.73%, meaning 2s10s spot sits at a whopping 3.82 basis points.

What is the same spread, starting in 3 months time?

3m2y (i.e. a 2y swap starting in 3months time) is at 2.662% and 3m10y at 2.738%, meaning that 2s10s 3 months forward sits at 7.64 basis points.

What does that mean for carry? If we received 2s10s starting in 3 months time (i.e. receive fixed on 3m10y and pay fixed on 3m2y) and we did nothing, then we expect that trade to decay from 7.64 basis points to 3.82 basis points, earning us 4 precious basis points of positive carry. We don’t even have to worry about spot Libor fixings changing that equation, as the structure won’t have any short-end fixing risk until three months time.

As a general measure, we would say that this forward starting 2s10s has a positive carry of 1.3 basis points per month.

Carry for Exchange Traded Derivatives

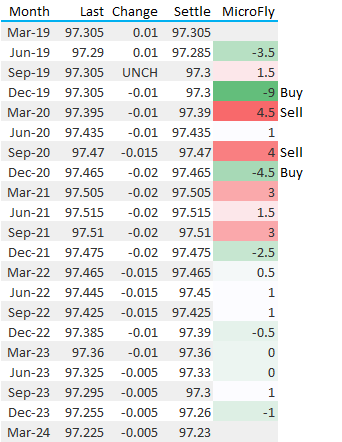

We can also look at common carry trades for short-term interest rate futures. For example, in Eurodollars, the “microflys” of consecutive quarterly contracts are often considered mean reverting to zero in a “normal” rate cycle. Therefore it is often instructive from a carry point of view to try to be long the middle contract of a microfly when it is trading below zero and short when it is above zero:

Showing;

- The Sep19-Dec19-Mar20 microfly in Eurodollars last night was marked at -9 basis points.

- Over three months, we could expect this fly to decay to be equal to the current Jun19-Sep19-Dec19 fly which is trading at +1.5.

- Therefore, if nothing else changes, the passage of time may earn us 10.5 basis points if we buy the SepDecMar fly. That is pretty attractive!

- Similarly, selling the Dec19Mar20Jun20 fly may be expected to earn us 13.5 basis points over three months if it decays as expected.

Carry on Portfolios

Measuring and managing carry across whole portfolios is far more complicated and can often be counter-intuitive. Whilst a portfolio can be cashflow positive in terms of carry (e.g. the net sum of the short-end payments from Libor fixings are lower than the average weighted Fixed coupon receipts), the impact of valuation changes along the curve can be even more significant. This depends on a number of factors, including both how steep the curve is and the precise distribution of portfolio cashflows. Carry strategies can also suffer from severe revaluation events, particularly around IMM roll dates, when the decay of DV01 risk from Swaps to Futures can be significant.

Carry for on-the-run Swaps

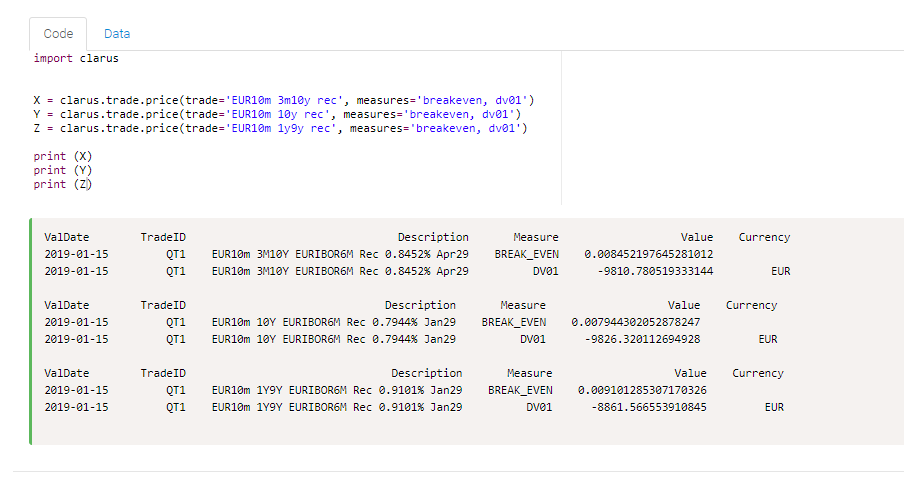

It is always instructive to look at an example, so let’s look at the current EUR10y swap.

Showing;

- If I received fixed on a 3m10y, I would expect to receive 5 basis points in positive carry over the next three months. (Trade 2 vs Trade 1 above).

- However, things aren’t quite that simple when I look at receiving fixed on a spot starting 10y swap. I would have positive carry from the effect of the coupons – I would receive fixed at 0.7944% and “pay” floating coupon of -0.24% (current 6m Euribor). That gives me a positive net cashflow carry of 1.03% of notional.

- Offsetting this, I know that if the forwards are realised, a 9y swap should have a breakeven rate of 0.9101% in 1 years time (trade 3 above).

- Do I think this is realistic? Spot 9y swaps today are trading at 0.69%.

- Enticed by the prospect of positive carry on my cashflows, I may therefore be motivated to receive fixed in 10 year swaps, knowing that my positive cashflow carry can subsidise a move higher in rates of up to ~10 basis points (i.e. 1.03% of notional for the first year versus the remaining nine years of the swap).

- This is akin to picking up pennies in front of the steam-roller because I only get to accrue my 1.03% cashflow carry whilst I have the trade on. My mark-to-market loss on the next 9 years of my trade can happen at any time! Gulp….

Carry as a Trading Strategy

Putting on negative carry trades can become quickly unpalatable for relative value traders (“RV”). This is because if a trade is expected to mean-revert, it is unlikely to be particularly volatile. We used to see this a lot in Cross Currency, where the spread between the e.g. 5y cross currency basis would typically mean revert to the 3-month front roll, dependent on long-dated issuance flows. This relationship has almost completely broken down since the financial crisis. However, we do see plenty of forward-starting swaps trading now, which are typically considered a “carry play”. It is common to pay the cross currency basis out of forward dates if it rolls down positively.

In Summary

- Carry on an Interest Rate Swap can be split into two components.

- One is the difference in coupons between the fixed rate on the swap and the current floating rate fixings.

- The second is the effect of time on the revaluation of the trade as it moves to an “off-the-run” valuation for all future cashflows.

- These two effects can be analytically considered to motivate particular trading strategies.