Following on from my recent article on MiFID II and the Trading Obligation for Derivatives, I wanted to look into another key section in the ESMA Final Report; namely the requirements for Best Execution. There are two specific requirements, one for Trading venues and another for Investment Firms.

MiFID II Background

The Final Report deals with Draft Regulatory Technical Standards (RTS) of which there are 28 and describes the consultation feedback received, the rationale behind ESMA’s proposals and details each RTS. The report is now submitted to the European Commission, which has 3 months to decide (Dec 28, 2015) whether to endorse the technical standards.

Assuming that it does so, MiFID II will come into effect in Europe on Jan 3, 2017.

Best Execution and Total Cost Analysis (TCA)

There have been a number of good overview write-ups on Best Execution, two I would recommend are Michael Sparkes of ITG Analytics on Multi-Asset Best Execution and Simon Maisey of Tradeweb on TCA for Fixed Income.

I usually find that diving deep into the detail and coming back up is a good way to grasp the essence of a new regulation. So lets look at the relevant detail in the Final Report.

RTS 27 – Best Execution for Trading Venues

An investment firm has a fiduciary obligation to provide its clients with the best possible results when executing orders. The data required to assess best execution is essential for investment firms to monitor performance from venues and for the buy side to monitor the sell side.

This RTS sets out the data that must be made public for financial instruments subject to the trading obligation.

It applies to venues that can be selected by investment firms for execution of their client orders (e.g. RMs, MTFs, OTFs). As such it would seem to apply to All to All Venues and D2C Venues and exclude D2D only ones (assuming D2D continue to exist in the new market structure). Either-way a large chunk of Swaps trading will be included in the Best Execution requirements.

Frequency of Data Publication

Execution venues are required to publish data four times a year and no later than three months after the end of each quarter. So by 30 June for the period 1 January to 31 March.

This data is expected to be available free of charge in a machine readable format on their websites.

Articles 1 to 12, deal with the specifics of the data.

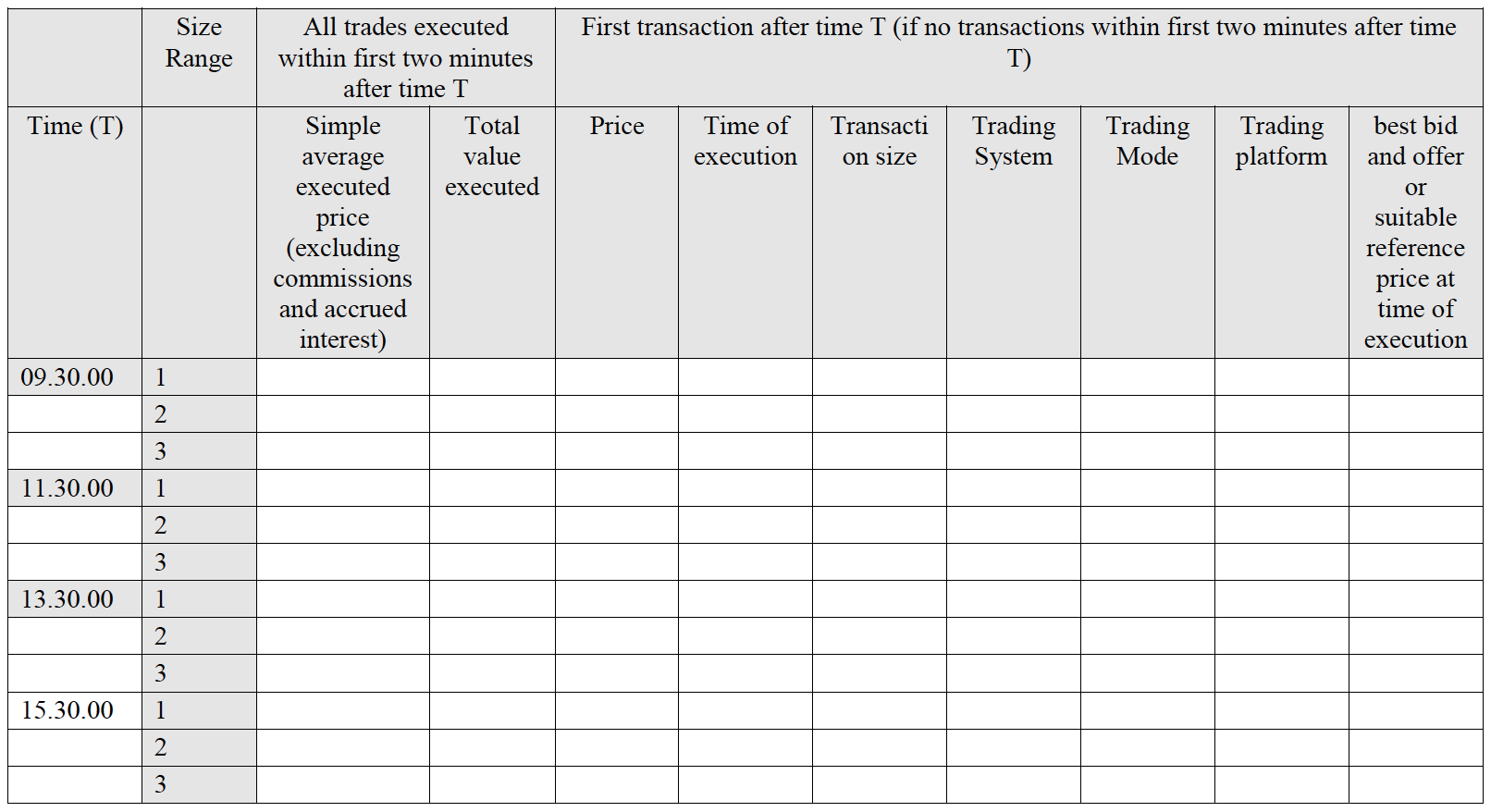

Article 4 – Price

We will start with the first interesting one, Article 4 on price. This requires price data for each financial instrument to be made available for each trading day with one format for intra-day information and one for daily information.

Intra-day requires the following:

Meaning that:

- for 4 specific times of the day (9:30, 11:30, 13:30, 15:30) and

- for each Size Range, 1 <= Size Specific to the Instrument (SSTI), 2 > SSTI and 3 > Large in Scale

- for all trades executed within the first two minutes

- the Simple Average Price

- the Total Value executed

And if there are no transactions in the 2mins, then details on the first transaction are required as per the next set of column headings in the table, so price, time, size, etc.

Daily reporting requires:

So for each trading day and instrument, the four rows above.

Lots of interesting price data indeed. Both point in time and daily averages.

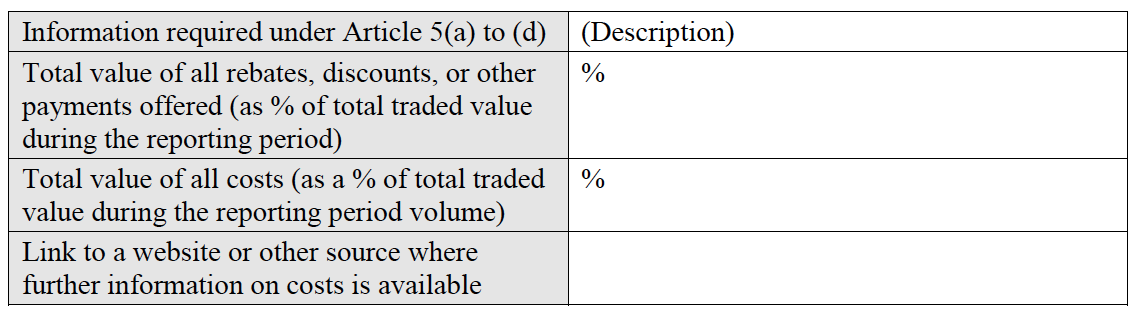

Article 5 – Costs

Costs for execution fees, fees for submission/modification/cancelling or orders, fees for access to market data or terminals and any clearing or settlement fees.

As well as a description of the nature and level of rebates and discounts.

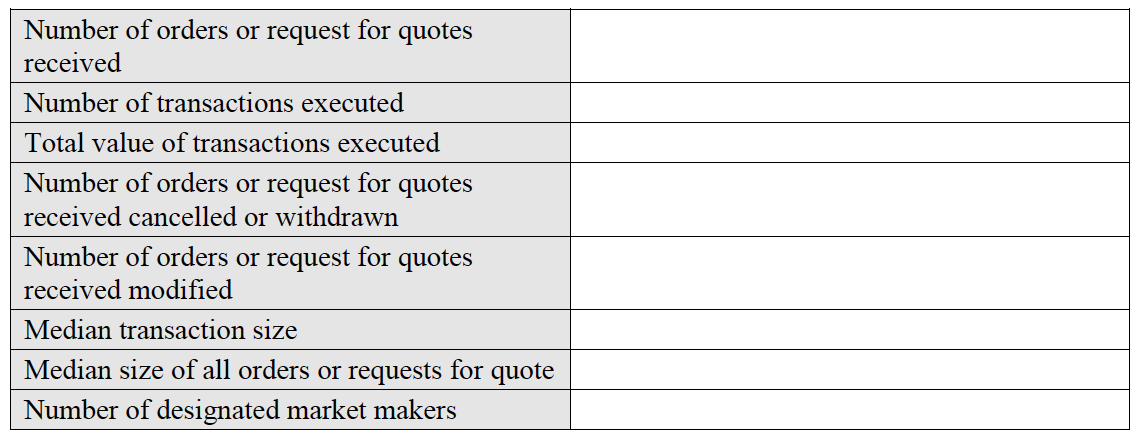

Article 6 – Likelihood of Execution

For each instrument and trading day:

Which will provide interesting comparative data on pre-trade vs post-trade and between venues.

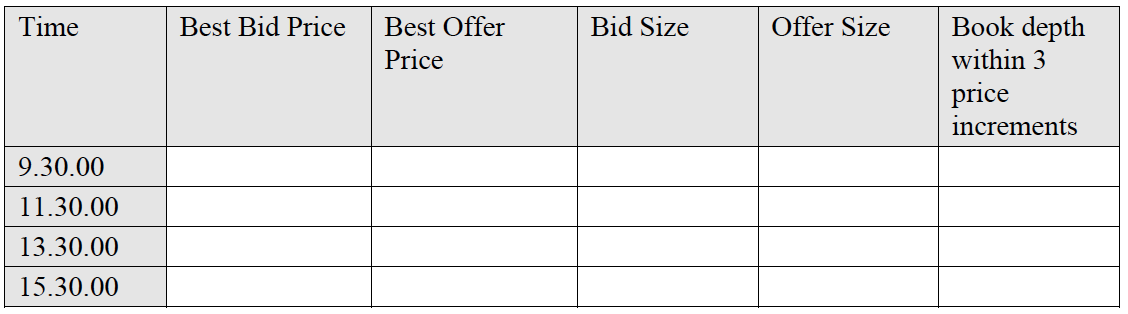

Article 7 – Additional Information for Continuous Auction Order Book and Continuous Quote

Which gives a sense of the oder book at 4 specific points in time for each trading day.

There is a second more detailed table, which I will skip as Order books are less relevant for D2C Swap trading, except to note that it contains the excellent sounding “Number of Fill or Kill Orders that failed”. For those interested, you can find this table on page 536 of the Final Report.

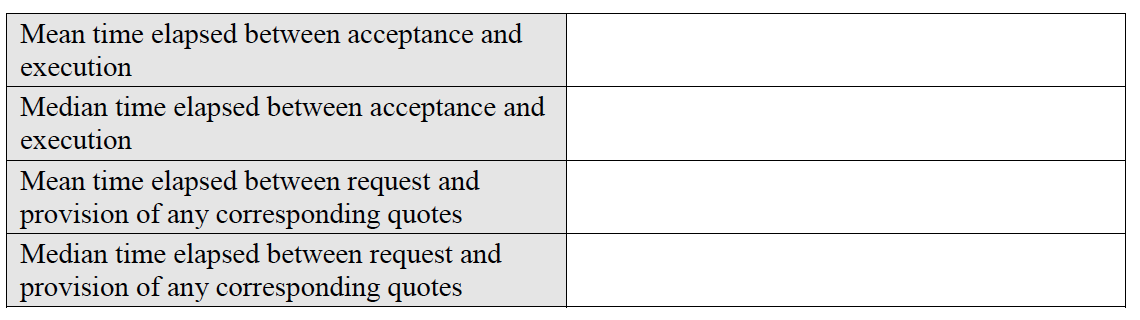

Article 8 – Additional Information for Request for Quote Venues

Simple statistics on the time between acceptance and execution and the request and quotes.

That covers much of RTS 27 – Best Execution for Venues.

Onward.

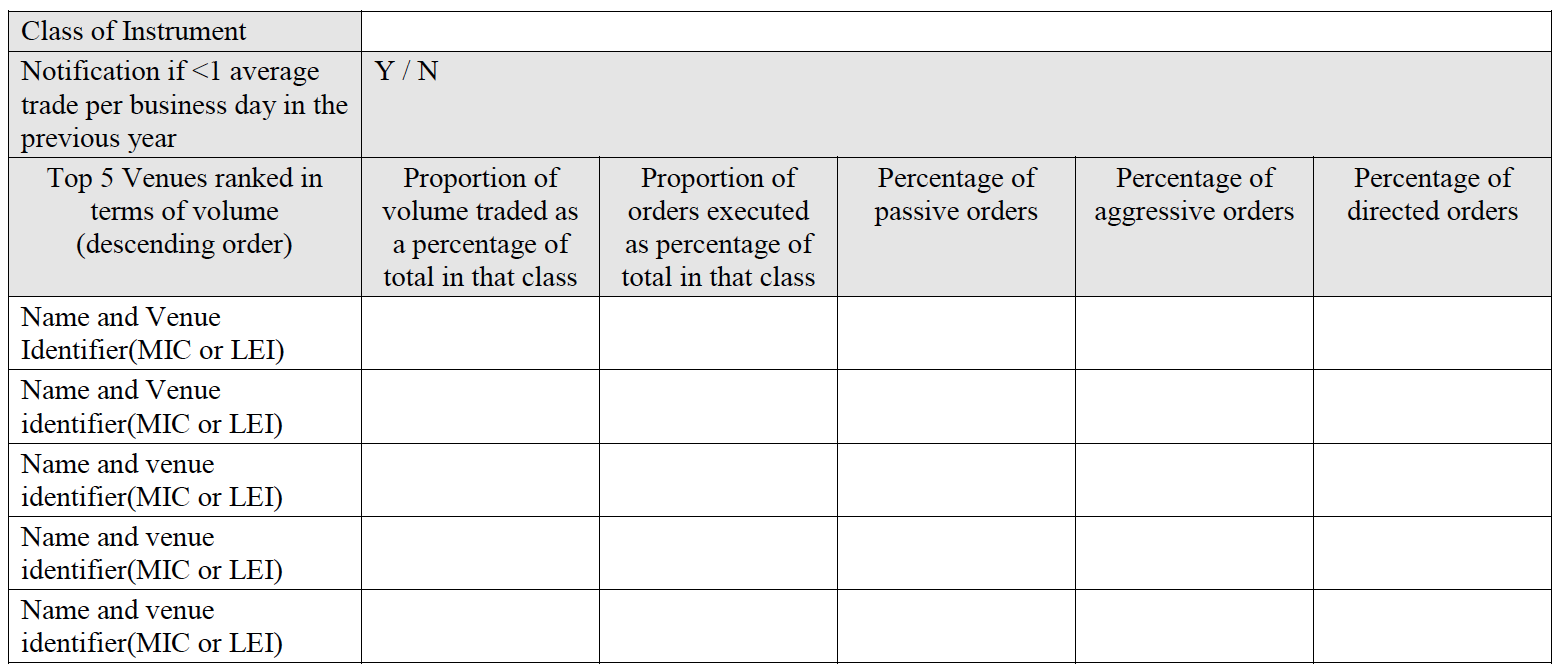

RTS 28 – Best Execution for Investment Firms

This requires investment firms to disclose annual information on the top five execution venues used for client orders in the prior year for each class of financial instrument, including whether the investment firm itself was one of the top five execution venues.

Classes of Financial Instrument

Those relevant to us today include:

- Interest Rate Derivatives

- Futures and options

- Swaps, forwards and other interest rate derivatives

- Credit Derivative

- Futures and options

- Swaps, forwards and other interest rate derivatives

- Currency Derivatives

- Futures and options

- Swaps, forwards and other currency derivatives

Information on Top 5 and Quality of Execution

Requires the following table to be completed.

Expressing volume as a percentage means that potentially market sensitive disclosures on the volume of business being conducted by an investment firm are avoided.

Passive orders means an order entered into an order book that provided liquidity, an Aggressive order means one that took liquidity and a Directed order means one where the execution venue was specified by the client prior to execution.

In addition there is a requirement to publish a summary of the analysis and conclusions the investment firm draws from its detailed monitoring of the quality of execution obtained, including an explanation of the relative importance given to price, costs, speed, likelihood of execution or other factors.

This information is required to be made public in machine readable format on the investment firms website.

Summary

That wasn’t so bad was it.

Time for a quick recap.

Trading venues will be required to make public each quarter, daily information in prescribed formats, for each instrument subject to the trading obligation.

This information will allow Investment firms to fulfil their best execution obligation to clients.

Investment firms will also be required to make public annual information on the Top 5 venues used for each class of financial instrument.

Thats it.

All very sensible and simple.

I plan to cover further aspects of MiFID II, MIFIR and EMIR in future blogs.

Roll on Jan 2017.

I like the summary of Best Ex reporting requirements into spreadsheet like views.

Don’t forget also the requirement on Investment firms to monitor ALL execution venues they potentially use for execution in order to demonstrate Best Ex and to inform the top 5 choice. This adds to admin significantly and may reduce the number of venues that firms will potentially use…