Six months ago I wrote a report that looked at the health of the FCM community. My general findings were that:

- The number of FCM’s was actively shrinking

- Only a small portion of FCM’s were handling Cleared Swaps

- The amount of client funds to support cleared swaps has doubled in the last year, concentrated largely in a handful of FCMs

I saw a report by John Needham last week that made me wonder if anything had changed. So I set out to update my numbers and see if there was anything of interest in the most recent CFTC data.

UPDATING SOME DATA

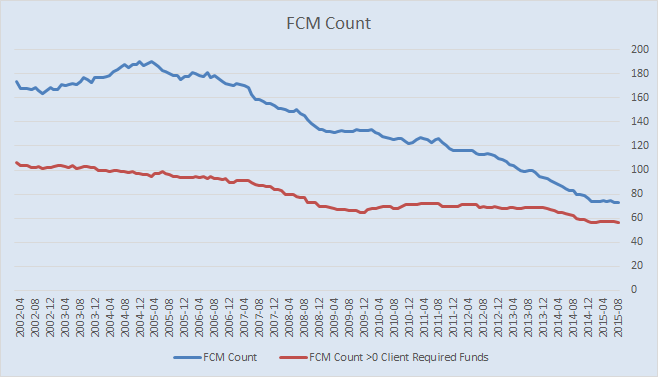

First off a simple count of the FCMs in the report. We noted last time this had been reduced to 74 firms in February. I am happy to report a little plateau here since then, as this number now stands at 73 firms offering clearing services.

As John noted however in his report, only 56 of these have any Customer Margins held. So I went back and changed my analysis to show both the FCM count, as well as a count of only the ones that had non-zero margin requirements.

Plotting both of these on a chart, you can see the total number of FCMs leveled off over the past 6 months (blue line) as well as the red line showing the count of FCMs that had ANY client requirement for futures and swaps. I have to think many of the 0’s are not just brand new or dying firms, but could also have FX position related balances – but it’s hard to say.

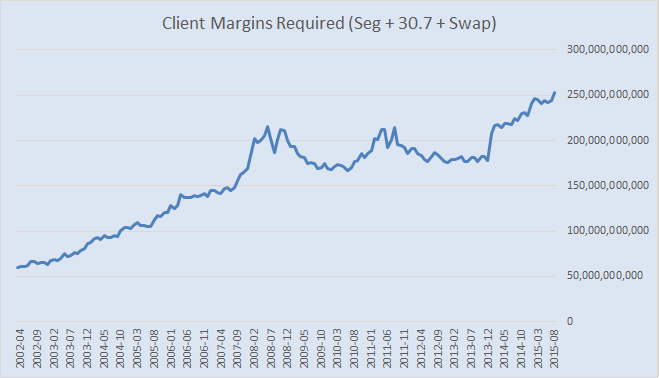

Next, I thought it worthwhile to look at the Client Required Margins since 2002. This says there was a significant increase in activity (as witnessed by required margins) up through 2008, then a leveling off until 2014 where it picks up again. Has the industry been stagnant since the financial crisis?

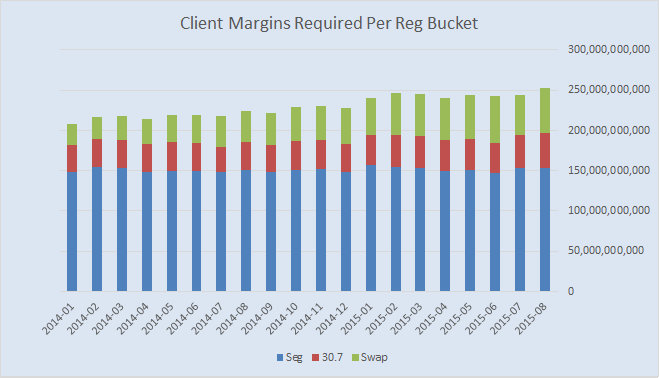

Very important to note that the spike in 2014 where the required margins resumes its upward movement is due to the addition of reporting of swap margins, which had not been included until January 2014. If we break down the composition of these margins since Jan 2014, you can see quite clearly that the only notable growth has been in swaps. Thank you Dodd-Frank clearing requirement I suppose.

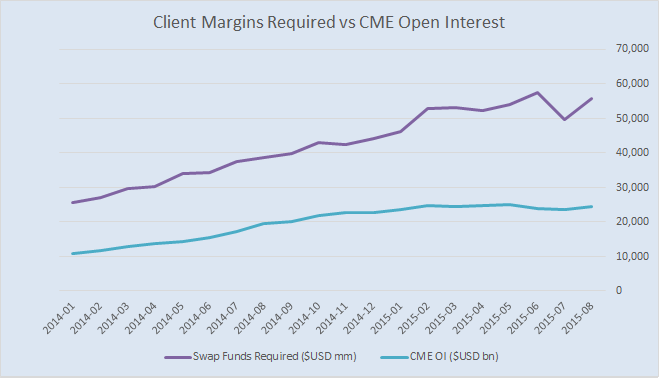

As I did in my last post, I sanity checked this increase in client swap margins with swap activity at the CME. Few assumptions here – first, that these margins are supporting swaps only at the CME, and second that CME cleared swaps are primarily client-driven. Both of which are not great assumptions, but still a fair proxy.

LEAGUE TABLE

I thought it worthwhile to look at the swap data since it began being reported 18 months ago. I created a table of the swap clearing FCMs, ranked by the most recent amount of client margins held for swaps. Let’s have a look:

The “Sparkline” is a quite useful tool as it shows the trend in the data for that FCM, and nicely highlights in red the largest value on the mini-chart. Just be a bit careful of the scale of the Y axis in a sparkline, as they are unique to each “spark”.

A handful of things to point out:

- Total required swaps margins increased in the 18 month period from 25 billion to 55 billion.

- Credit Suisse ranks #1, up 2 spots, however off of their highs in terms of client funds.

- Citi has dropped 2 spots and Barclays is off 4.

- Wells Fargo showing steady growth over the period and ranking 6th, up 3 spots.

- RBC the other notable here, basically a startup in 2015 that now ranks #13 showing a clear investment in this business.

- SocGen and Newedge – I chose not to combine these into 1 entity as I wasn’t convinced that the data supported a simple “change of names”. But I would assume most ex-Newedge clients are now SocGen clients. Ditto for Jefferies Bache as would believe these ended up in the same pie.

- ED&F Man another startup, jumping into 17th

- The table also serves as a nice recent history lesson with BONY, Jefferies, RBS and State Street disappearing. Remember them?

- BOCI (Bank of China International) is a bit of a mystery. They have reported 0 client required margins, but have consistently reported $6 to support client swap trading. As in six US dollars. Their client must be preparing to buy a Starbucks latte. Or a swap on a Starbucks latte.

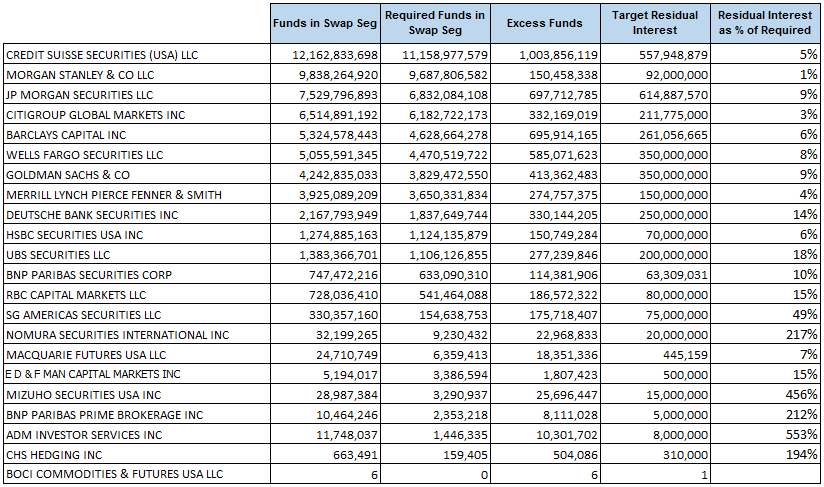

RESIDUAL INTEREST ANALYSIS

If you remember back to my blog on Residual Interest, I discussed how FCMs will size up a chunk of funds to keep aside to protect against being called into deficit when they pledge margin calls to clearing houses on behalf of their clients. I am not an expert at analyzing the CFTC data on this, but I would generally think the larger the proportion of residual interest held, the more conservative the firm (or logically the other way around). On the other side of the coin, one might argue the lower the residual interest, the perhaps more operationally efficient the firm is – with their ability to more frequently make margin calls.

Whatever the case, I’ll post the table below which shows each firms residual interest as a percentage of client margins required. While I cannot contribute much analysis of this, at a minimum I get to point out that BOCI has set aside 1 dollar for that imminent latte swap.

SUMMARY

Recapping all of this:

- The amount of FCMs seems to have levelled off, with a few newcomers in to replace those going out.

- Total margins pledged to FCMs to support derivatives seems to have plateaued since the financial crisis. Only gains would seem to be due to the reporting of swap margins.

- Many useful nuggets of information in the FCM league table which corroborates much of the rumors concerning “who is investing” in clear swaps.