Let’s take a look at the European bond market today.

I wanted to repeat much of the analysis that I performed for MIFID II post-trade data concerning Interest Rate Swaps. However, I realised that we do not have enough of a complete data set due to a myriad of data access issues.

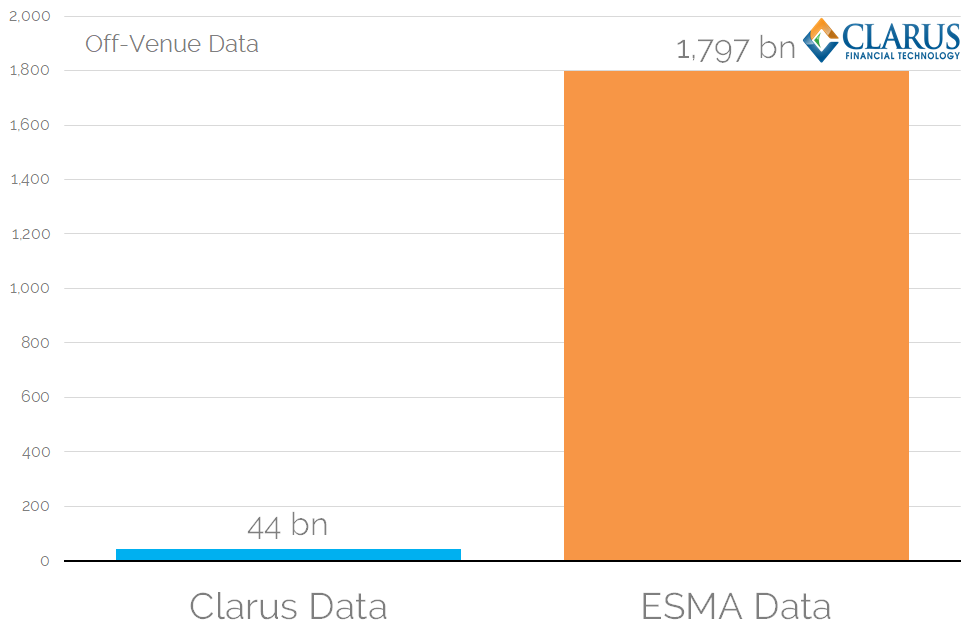

For example, the bond data that we are able to source (mainly from Bloomberg and Nasdaq, with occasional manual downloads of Tradeweb data) shows a weekly bond volume of €150bn. ESMA data suggests that the European bond market is €1.8 trillion each week.

As a result, I do not think our overall data is representative of the entire market. However, we can still look at the data and highlight what is interesting.

Talking of which, I am still looking for a reasonable estimate of the split of European on-venue vs off-market for bond trading. Any readers care to put out an estimate?

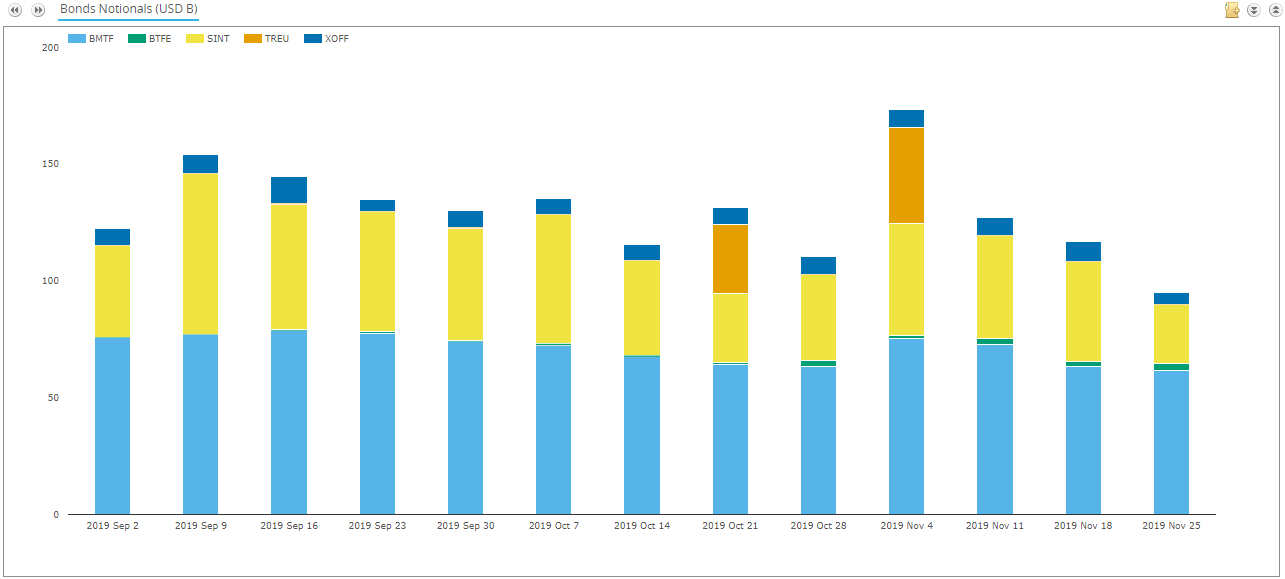

MIFID II Transparency Data for Bonds split by Execution Venue

European Data

There are two aspects of MIFID II post trade data – Off-Venue and On-Venue. Off-Venue data is mainly from bilateral dealer-to-client trades (executed on so-called Systematic Internalisers), so it is really new data that wouldn’t exist without MIFID II. It is generally accessed via APAs.

On-venue data is provided by MTF and OTF trading venues themselves, although some will choose to report to an APA. Sounds exciting to get our hands on such data, but…

When we look at the ESMA data for bonds transacted in the past six months we find a completely different scale of data compared to what we have been able to collect. We estimate we have only been able to get our hands on 9% of the data.

Showing;

- The data provided by ESMA is for “instruments that were admitted to trading for which trading venues submitted data for at least 95% of all trading days”.

- Remember that the ISIN for an Interest Rate swap (and FX) changes every single day. So in effect the file that ESMA is providing for non-equities is a list of bonds that were transacted. Indeed, there are no “EZ” ISINs (for derivatives) in the file.

- The total volume for the period April-September reported by ESMA was €47trn. This is equivalent to €359bn per day, or as the chart shows €1.8trn per week.

- Our bond data, which comes from Bloomberg, Nasdaq and Tradeweb, is just €156bn in a good week.

Whilst it seems strange to point out the short-comings of our own data, we want to highlight how difficult it is to get our hands on transparency data in Europe.

Transparency means having unencumbered data that we can work with. For now, we are left to analyse the data that we can actually collect.

Split of Data

Our total on-venue data totals €105bn per week, representing 68% of our data. But it is a tiny portion of the total market, again due to data access issues. Our data results in visibility for just three MIC codes of trading venues. When I look at this ESMA data for Bond Liquidity, I discover 163 different MIC codes reporting bond liquidity data!

That means we do not think our On-Venue Data is representative of the market.

We believe that we have even less off-venue data as a proportion of the total off-venue market.

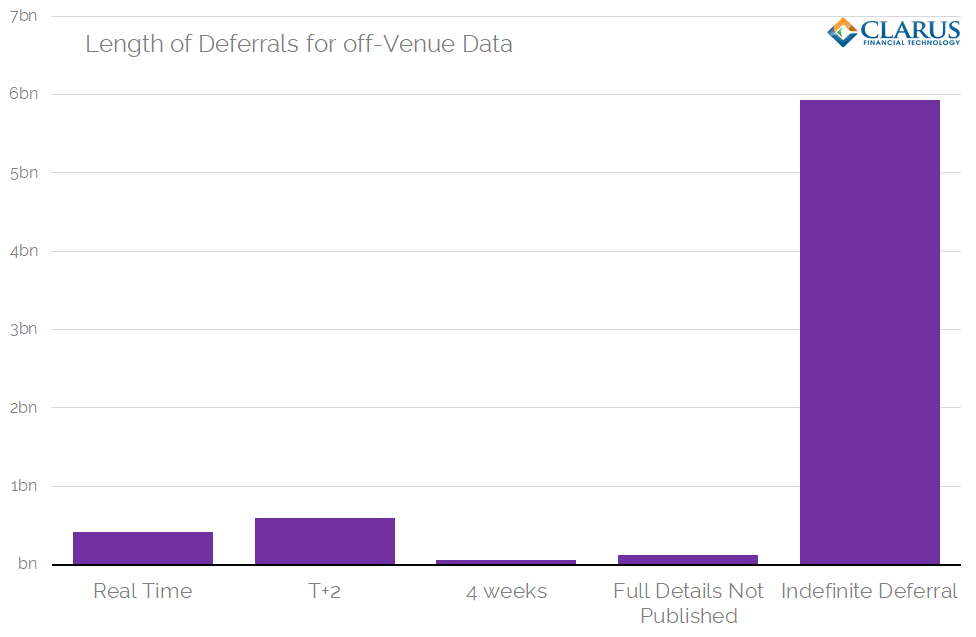

How much of the data is deferred?

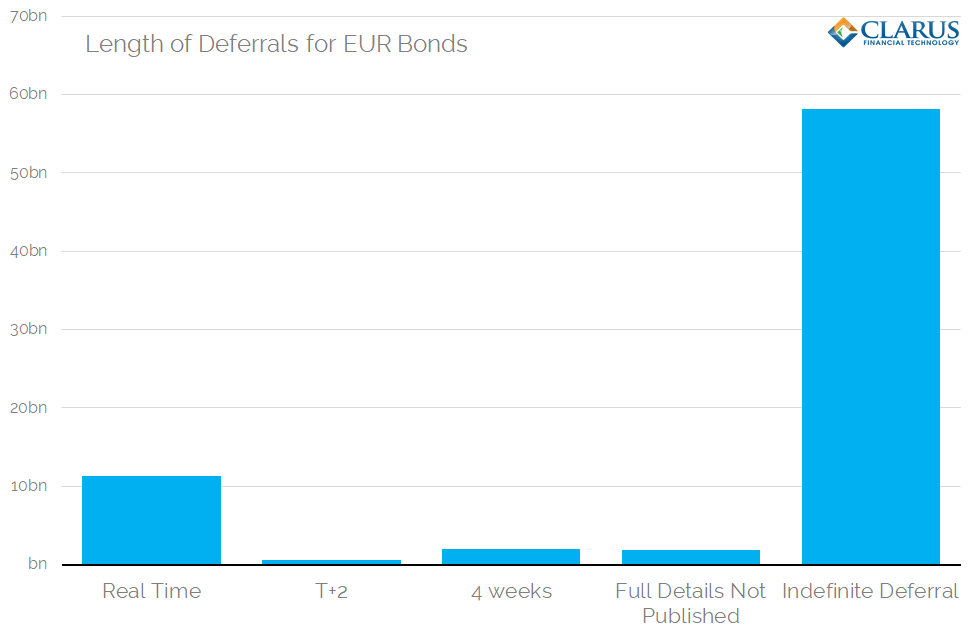

At least we can look at the data we do have. Let’s start with an analysis as to how much of the data is deferred, just as we did for Interest Rate Swaps:

85% of EUR bond notional is reported with a deferral.

Showing;

- The trades reported in real time represent only 15.3% of notional.

- A tiny portion of trades are reported T+2 (0.8% by notional). Remember this is across trades reported by APAs and MTFs. Maybe this is higher in dealer-to-dealer markets?

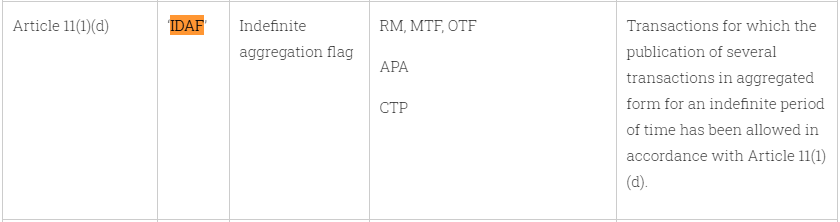

- Most volume is marked with an “IDAF” deferral, signalling;

mifidiihub.com

Our understanding of the IDAF flag is that aggregated volume over the period of a week is reported. Full trade level details are not only deferred, but they will never be published.

I discovered that TRACE data in the US, for the public dissemination of corporate bond trading, results in 97% of corporate bond trades being reported with no delay. Block trades are reported within 15 minutes. That is quite some difference!

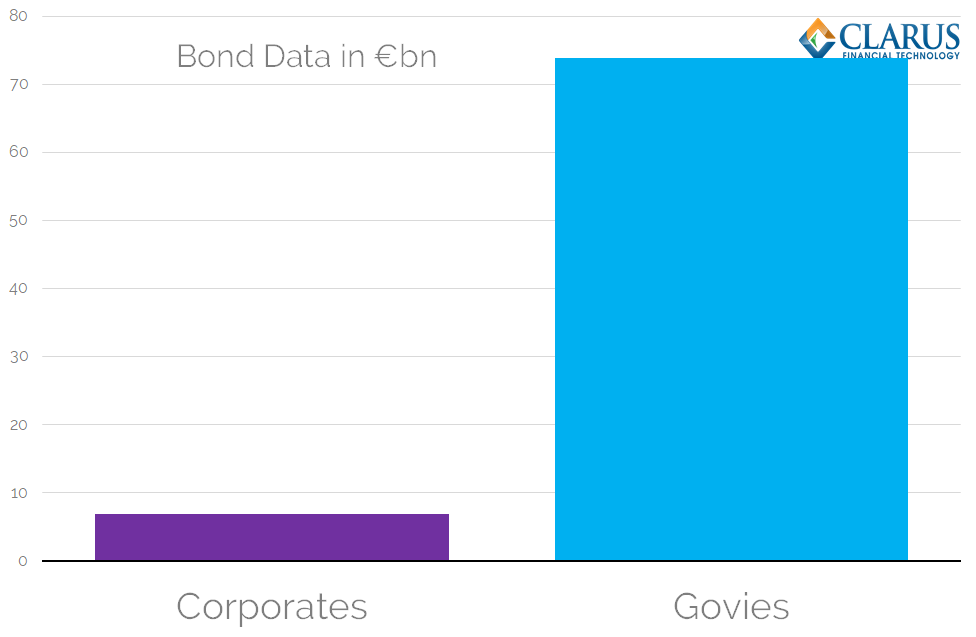

How much volume is in Corporate Bonds?

Talking of TRACE, I thought it would be interesting to look at the split between “credit” trading (Corporates) versus sovereign bond trading (Govies).

Basic information from the issuer name of the ISIN let’s us identify the split:

Showing;

- Our data suggests that Govies represent 92% of the total volume data being reported.

- This suggests that Govies should be the centre of attention for transparency efforts.

How much of our off-Venue data is deferred?

Finally, it is worth analysing the off-venue data to look at the deferrals for bonds executed away from trading venues. These volumes are mainly executed bilaterally with dealers;

- Deferrals are longer than for bonds traded on-venue.

- Over 83% of volume is published with an Indefinite Deferral.

- Just 5.8% of volume is published in real-time.

In Summary

- We can only access 9% of the total European bond market using accessible data sources.

- Of the data we can access, 85% of it is deferred, most of it indefinitely.

- Only 5.8% of volume data for bonds is published in real-time.

- Government bonds make up 92% of the total volumes we see.