- We attempt an analysis of available MIFID II transparency data.

- Analysis shows that 89% of notional in vanilla EUR IRS is reported with a four-week delay.

- We show that at least €800bn of transaction data for vanilla, cleared EUR IRS is missing each week.

- We estimate that as little as 5% of notional of off-venue vanilla EUR IRS trades are actually being published by APAs.

Transparency

Our frustrations continue with MIFID II data. Anyone wanting to understand why we are so frustrated should head over to the recent ESMA consultation responses and read ours here.

Now that those responses are in, let’s assume that the data access issues get fixed and we are able to access the data from APAs, MTFs and OTFs. Would we be able to use the data to provide transparency? Would our understanding of market dynamics, price movements and liquidity improve?

To assess that, we need to look at the data we have so far. Whilst our subsequent analysis is based upon a subset of the overall market, we strongly believe that there are serious issues with the data being published.

Real-Time Reporting

As we collect more data (from Bloomberg and Nasdaq), we are struck by the sheer lack of real-time reporting for OTC Derivatives. Everything appears to be deferred. Post trade transparency 15 minutes after execution is a myth at the moment.

We use the Bloomberg MTF data as a proxy for the whole market. For EUR IRS traded in the month of September 2019, we see the following:

- 6,583 trades.

- €415.6bn in notional of vanilla Fixed-Float EUR IRS.

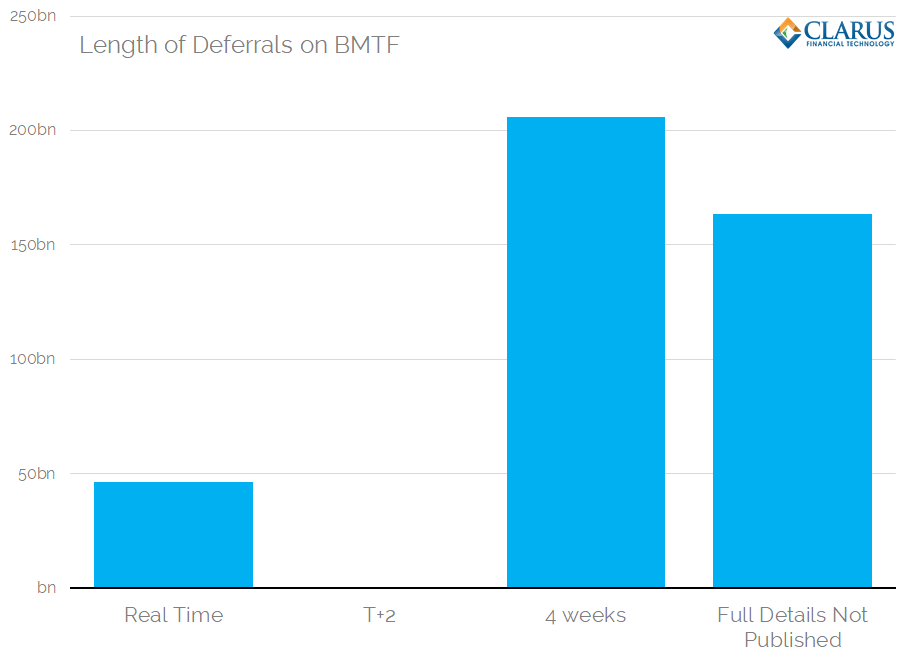

And yet how much was actually reported in real-time? We’ve had to use September data to ensure we have a full month of trades, because most trades are being deferred by four weeks.

With many thanks to our regular readers who have helped clarify the deferral flags in MIFID II data, the chart above shows that:

- The trades reported in real time represent only 11% of notional.

- This is because so many trades are either deemed “Illiquid” or are above the “SSTI” threshold for EUR IRS.

- There are no trades reported after T+2.

- Almost all volume is reported with a 4-week delay.

When trades are published with a four week delay, they are first published in aggregated format on the following Tuesday after execution. These carry a specific deferral flag, “FWAF”. These should, in theory, be “promoted” into a full disclosure (using the flag FULJ for example) after 4 weeks, and hence the aggregated data will be removed from the data set.

However, the publication of full trade details is not consistently happening for all trades. This may be due to ISIN errors (the trades are aggregated at an ISIN level), or transaction identifiers. It is also potentially a bug our end (it does happen..VERY occasionally). We’ve included them to show how potentially complex it is to monitor these deferrals and to be able to perform accurate analysis. Rubbish in = rubbish out.

There appear to be a lot of trades missing

Here’s the MIFID II post-trade data that we’ve managed to pull over the past six weeks:

Showing;

- How difficult it is when we do not have automated processes. We have attempted to grab Tradeweb APA and MTF data manually on four occasions now. That process is arduous, painful, obstructive and unpleasant.

- We have a decent amount of data for four weeks. We cannot claim it is complete due to deferrals and the likelihood of some missing files from Tradeweb. We also do not have any data from interdealer venues. We do, however, think the data is representative.

For clarity;

- Red bars are the Tradeweb MTF (a D2C MTF).

- Green and yellow bars are the Bloomberg MTFs (one in London, one in Amsterdam. Both Bloomberg venues are D2C MTFs).

- Everything else is an APA (and hence represents the off-venue D2C market – interdealer trades are generally executed on an MTF or OTF).

Even eyeballing the data therefore suggests that the vast majority of EUR IRS that are actually being reported are being transacted on-venue. This raises the issue as to whether the data is truly representative of the market. For example:

- In the week of 16th September, when we have the most complete data from Tradeweb APA, 7% of total notional was reported to an APA. The rest was reported by an MTF and hence traded on-venue.

- If we assume that 100% of trades reported to an APA are from dealers (“SIs”), then this suggests that 93% of notional in vanilla EUR IRS is being transacted across an MTF in the D2C market (i.e. on-venue).

We find this split between off-venue and on-venue to be completely unbelievable. Is there another APA out there collecting all off-venue trades in EUR IRS? This seems very unlikely given that we have been looking at this data for two years and are constantly keeping ourselves updated of what is out there. More likely is that trades are not even being reported (or published) by APAs.

Why do we think trades are missing?

Trades are not being published by APAs due to another quirk in MIFID II. At the moment, off-venue OTC derivatives are only published by an APA if the transaction is considered “traded on a trading venue”. ESMA has defined this phrase in a very granular manner (known as TOTV) in May 2017. It means that many off-venue trades are not being reported at all.

Our extensive experience of monitoring what is happening in the US with SEF trading supports this conclusion. For example, focusing on EUR swaps traded by US persons, we find:

Showing;

- More than half of all EUR Swaps transacted by US Persons are transacted off-SEF.

- For comparison, remember that the EU data suggests only 7% of trading is off-venue.

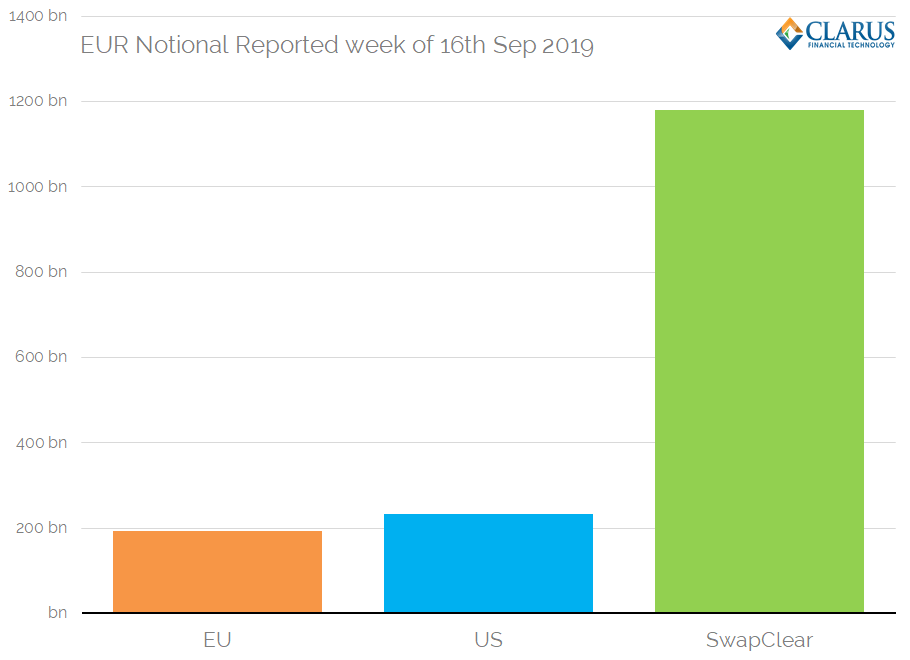

A full comparison of the EU and US data-sets shows:

- EUR swaps reported under MIFID II for the week of 16th Sep: €193.4bn

- EUR swaps reported under Dodd-Frank for the week of 16th Sep: €233bn

Showing that more EUR IRS are being reported in the US than in the EU, even though the EU is the much larger home market for these transactions.

We can also combine this with the total size of the EUR cleared market:

- EUR swaps cleared at just LCH SwapClear for the week of 16th Sep totaled: €1.179 TRILLION.

Even leaving aside the uncleared EUR IRS market, combining the EU and US data sets means that we are missing almost €800bn of EUR IRS volume.

Where is the data?

Given that the US transparency requirements apply to all transactions involving a US person, we know that the missing transactions are in the EU data set.

We estimate that approximately 90% of off-venue volume in vanilla EUR IRS is missing from the APAs. This is based on the fact that over half of all EUR IRS in the US are transacted off-SEF.

This could even be a conservative estimate. We are missing data from interdealer venues. Including that data could mean that as little as 5% of notional in vanilla EUR IRS that is traded off-venue is being reported by APAs.

What needs to be done?

To answer the title of the blog, we need two things.

First, we need to get rid of the deferral regime. All transactions are made available within 15 minutes (most within two minutes) in the US.

Secondly, we need to ensure that every transaction is reported, not just those deemed TOTV.

In Summary

- Understanding MIFID II transparency data is hard.

- Most volume in vanilla EUR IRS is being reported with a four-week delay.

- Even after the four-week delay, we find that €800bn of vanilla, cleared EUR IRS are missing from the EU data.

- We estimate that as little as 5% of off-venue volume in vanilla EUR IRS is being reported.