We have written quite a few blogs this month on the challenges of getting meaningful public transparency data on Swaps and other Derivatives. Today, three weeks after the MiFiD II implementation date, I thought I would write up what I can find for EUR Interest Rate Swaps from the public sites of the major D2D trading venues.

Benchmark

As a benchmark or goal, it would be a good first step if there was a lot more data available for EUR Interest Rate Swaps from these European Venues than that available in the US under Dodd-Frank rules.

Using SDRView, we see the following US data:

- A total of 97 trades in On SEF and Cleared EUR IRS vs Euribor 6M

- From SEFView, we find that the majority of volume in EUR IRS on 23 Jan 2018 was on D2C SEFs at €20 billion, made up of both price-forming and portfolio maintenance activity.

- On D2D, we only find €50 million from three trades, two at IGDL and one at BGC.

So much for a benchmark! 3 EUR trades on D2D venues!

To put this in perspective, we saw 1,900 USD IRS reported to SDRs. Around half of which are typically transacted on a D2D venue. This whets our appetite for European data – we should see as much data for EUR swaps as we do for USD IRS in the US.

European D2D Venues with IRS

How did I go about getting this?

Well yesterday at 4:00pm London time, I sat down and accessed the public sites of the major venues and as expected it was a painful process for reasons that we have documented before:

- Needing to know the ISIN for each Swap (see here)

- Tedious repeated selection/entry of each ISIN one by one

- CSV files not available

- Having to take screenshots

- Many screenshots, one for each Venue & ISIN combination!

- Laboriously typing in the key fields into Excel

- Counting the on-screen zeros to make sure it was 10,000,000 not 100,000,000

- I could go on …..

Suffice to say at 6pm, after two hours, I ran out of time and motivation and gave up.

So while I did not get everything, I think I got all/most the TP-ICAP venues, some/most of TradX (hard to know) but unfortunately did not get to BGC at all, which I would have liked to.

And this morning, none of these public sites provide access to yesterday’s trade data!

I appreciate as MiFID II is just starting and there may be teething technical problems making both Venues and APAs coy about the published public data.

Also I am aware that many of the same firms have Data businesses and are understandably wanting to either protect those franchises or possibly commercialise the MiFiD II public transparency data.

But I really expected that public post-trade data that is 15 min delayed would have been far more readily available in a machine readable format and that this availability would in no way impact existing Data businesses or future commercial models.

Machine Readability

And just for completeness sake, below is the relevant text from the EU Commission document.

While it explicitly states APAs and CTPs, I would be very surprised if the expectation on Trading Venues that do not use APAs is any different to this.

In which case, we have some way to go for these requirements to be met by all APAs and Venues.

If you disagree, please add a comment below.

Lets move on.

Caveats on the Data

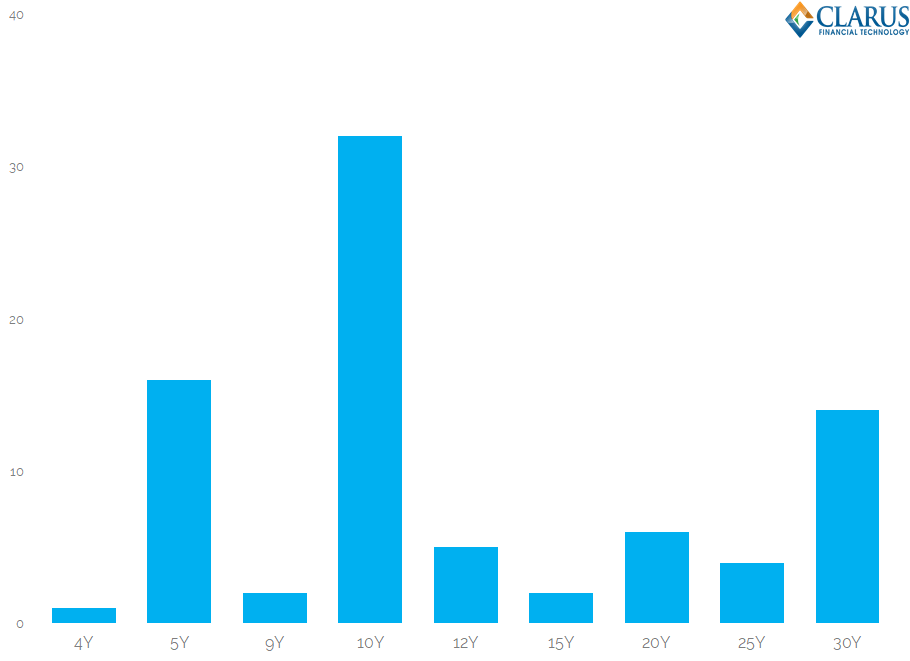

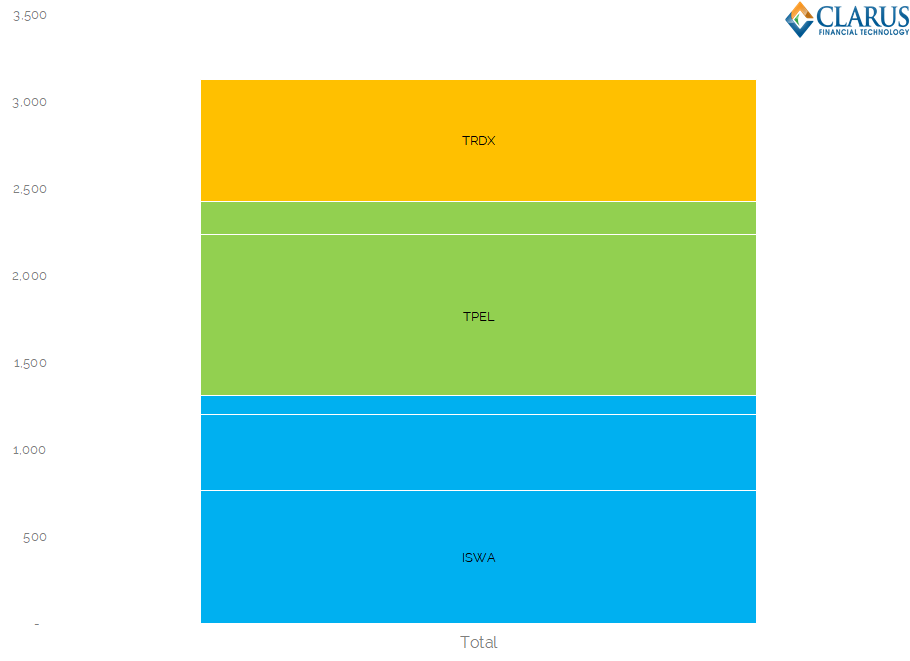

For Venues with MIC Codes of ICPM, IOTF, ISWA, TPEL, TPEO, TRDX on 23 Jan 2018, I found 94 trades/trade legs with €3 billion gross notional.

Certainly more than the 3 trades and €50 million in US data, but still a low number.

Tradeweb MTF averaged about 115 Euro IRS trades per day with an ADV in excess of €10bn (see Chris’s blog on Tradeweb MiFID Data – Interest Rate Swaps).

Of-course the deferrals available; both standard deferrals based on liquidity, SSTI, LIS, Package or National Competent Authority discretion and supplementary deferrals, mean that many trades will not be disclosed till a subsequent business day.

For these reasons and my own omissions, we must be careful with what information we can assume from the data, nevertheless we can start to produce some interesting charts.

Charts

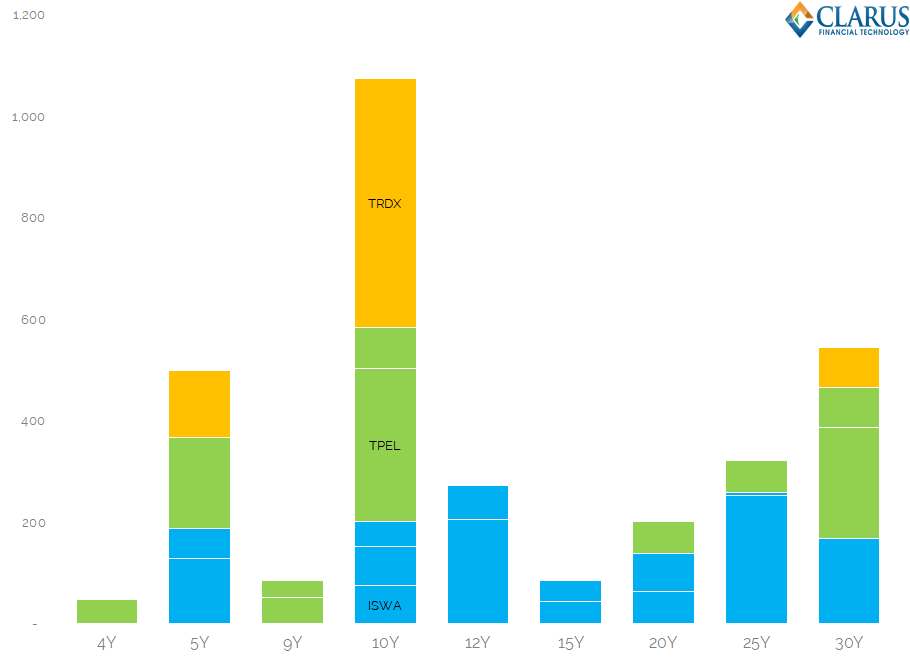

Showing that 10Y has by far the most trades/trade legs.

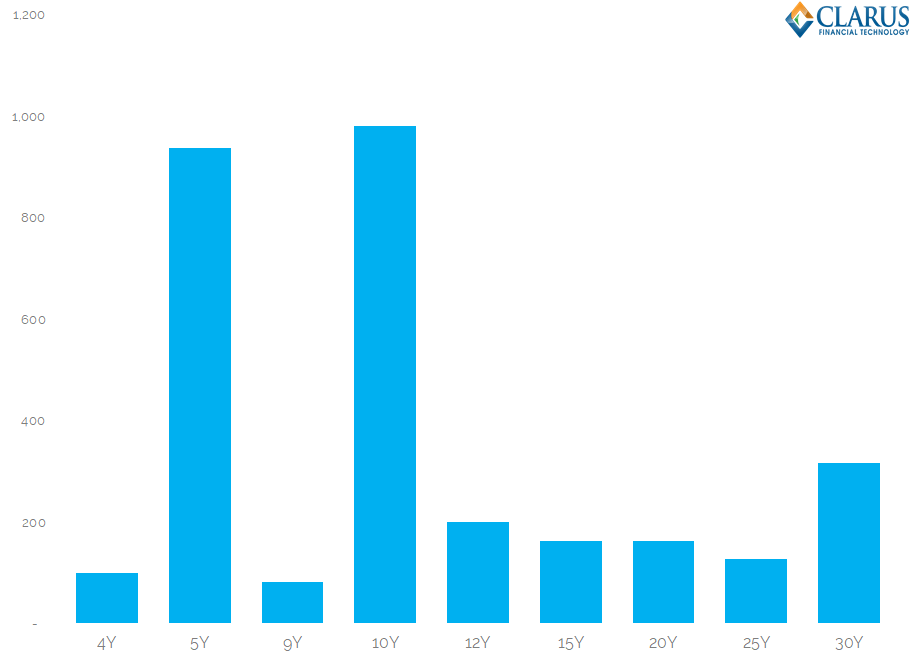

While in Gross Notional terms 5Y and 10Y are similar, both around €1 billion.

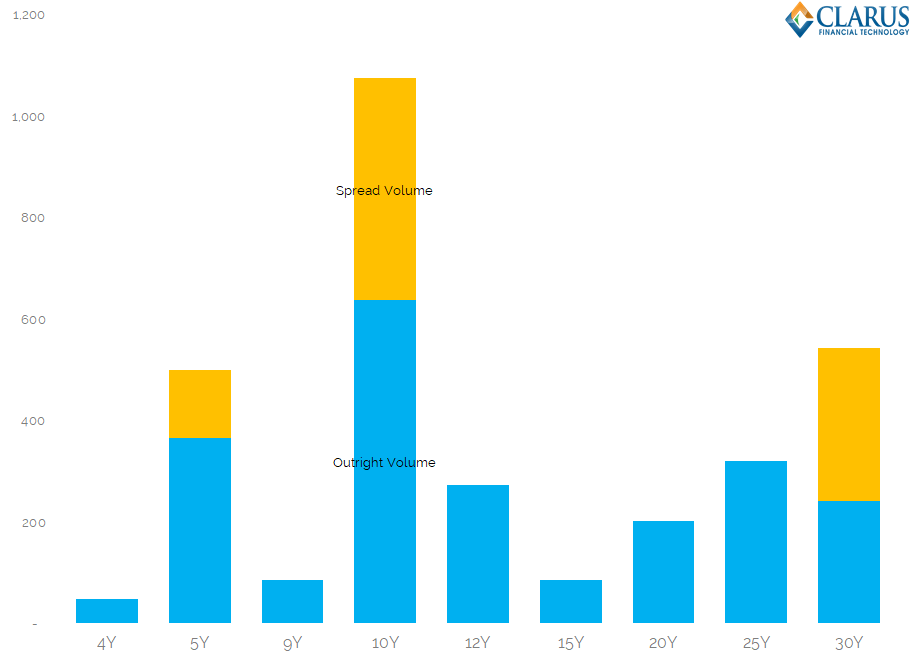

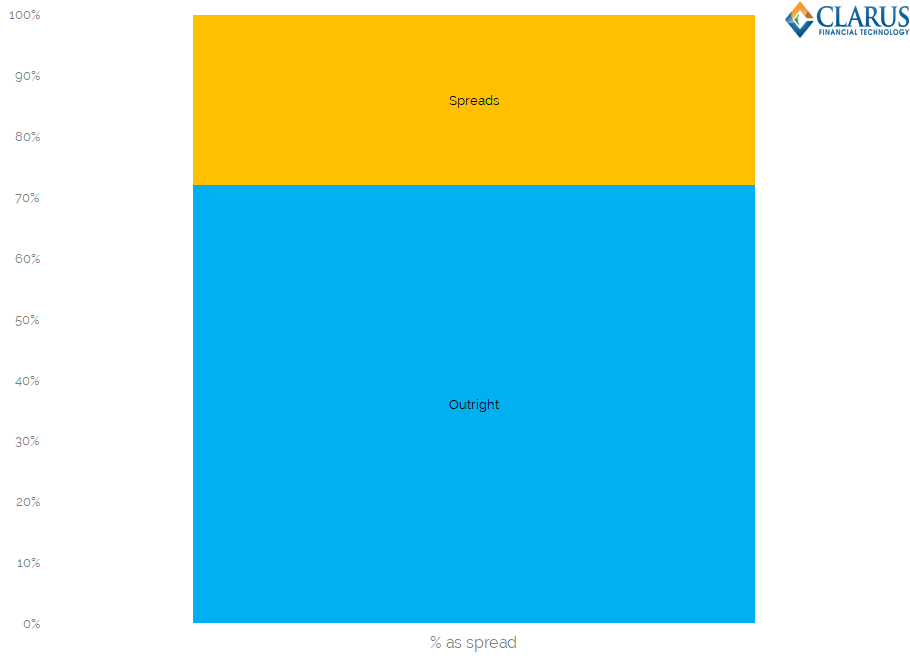

And the same but by DV01 and isolating Curve Spread trades from Outrights, with the Spreads concentrated in 5Y, 10Y, 30Y as we would expect.

Showing that 70% of this dataset is Outright risk and 30% is Curve Spread risk.

Showing that ISWA, TPEL, TRDX are the largest of the six venues.

And the same but broken out by Tenor.

The quality of the data looks “believable”. There is concentrated risk trading in 5y, 10y and 30y. But we are surely missing an order of magnitude in terms of total volumes?

A cross check with CCPView shows that ADV for D2D cleared EUR swaps (globally) is €172bn so far this year. Is it possible that 98% of volumes are trading off-venue? Surely not. We need the deferred data and other venues and APAs to see how much is on-venue and how much off-venue.

The End

In summary, after some effort, I found some interesting data.

But the limited nature of this data means we have to be careful in using.

It is far from conclusive in terms of notional, dv01, tenors and share.

It provides some insight.

But is much less comprehensive than the Tradeweb data we covered today.

We hope to get similar access to comprehensive D2D venue data.

And will then cover that in more detail.

As I am not planning to repeat the manual screenshot exercise.

Volunteers?

Market Participant? Regulator? Member of the Public? Anyone?

Amir, I can totally sympathize with what you are doing through.I’m beginning to think commercial aspects of the data sales has played a major role in designing systems in deliberately complicated way – I can understand a minor service errors, performance problems etc. but looking at what I had seen in terms of data for public perusal, this definitely looks like a planned obfuscation than accidental one.

PS: Time to crowd source the data collection 🙂 amazon turk perhaps