- Many thanks to Tradeweb for responding to our requests for access to weekly aggregated data.

- EUR IRS were by far the most traded Interest Rate Derivative across the Tradeweb MTF.

- Over €16bn in EUR IRS was transacted in the week 9th-16th January.

- Tradeweb volumes are equal to those reported by Bloomberg’s MTF for the same time period.

- Global D2C Cleared IRS volumes for the week in question were a €1trn.

- This suggests that a large portion of the market is trading off venue.

- We need to wait and see if more EUR IRS data is published after the first 4 week deferral period in early February to be sure.

Where to Start?

We are a bit like kids in a candy shop when we get new data, so first off we would like to extend a large thank you to Tradeweb for delivering us data in a usable file that makes sense.

We’ve got both Tradeweb MTF and APA data. Given that we focussed on the Bloomberg MTF previously, we will start by looking at what has traded on the Tradeweb MTF.

This blog will focus on Interest Rate Swaps. The headlines?

- Nearly 1,000 swaps traded across Tradeweb.

- Most were in EUR IRS, recording an ADV in excess of €10bn (€9m in DV01).

- About 115 EUR IRS trade every single day across the Tradeweb MTF. Impressive stuff considering such a limited Trading Obligation in the asset class. This will surely only get larger.

- Most risk trades in three benchmark maturities – 5y, 10y and 30y swaps.

- Global data suggests a huge portion of the EUR IRS D2C market remains off-venue.

The sheer size of the off-venue market in EUR IRS suggest to me that I need to quickly follow-up this blog with a look at the Tradeweb APA data too. As we said, kids in a candy shop…!

Trade Counts

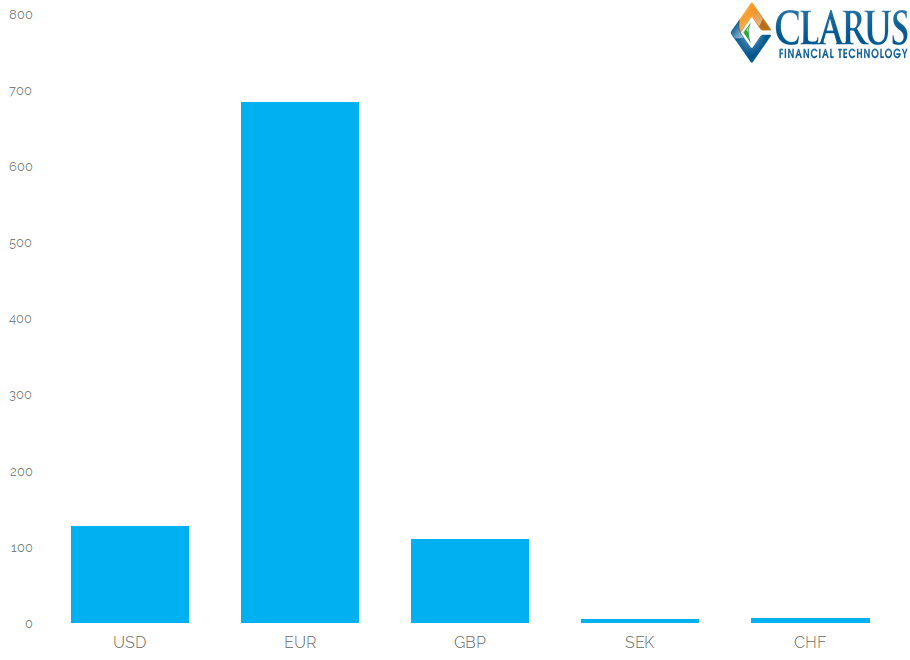

We have identified 685 EUR IRS swaps traded across the Tradeweb MTF in the period 9th – 16th January 2018 inclusive. There were also swaps traded in USD, GBP, SEK and CHF.

Showing;

- EUR IRS is the most traded IRS across the platform.

- USD is second, followed by GBP.

- 73% of all the swaps reported were in EUR. This is great news. Immediately, it looks very similar to the home currency-bias we see for Dodd Frank data in the US.

Given this large skew towards EUR IRS, let’s dive deeper.

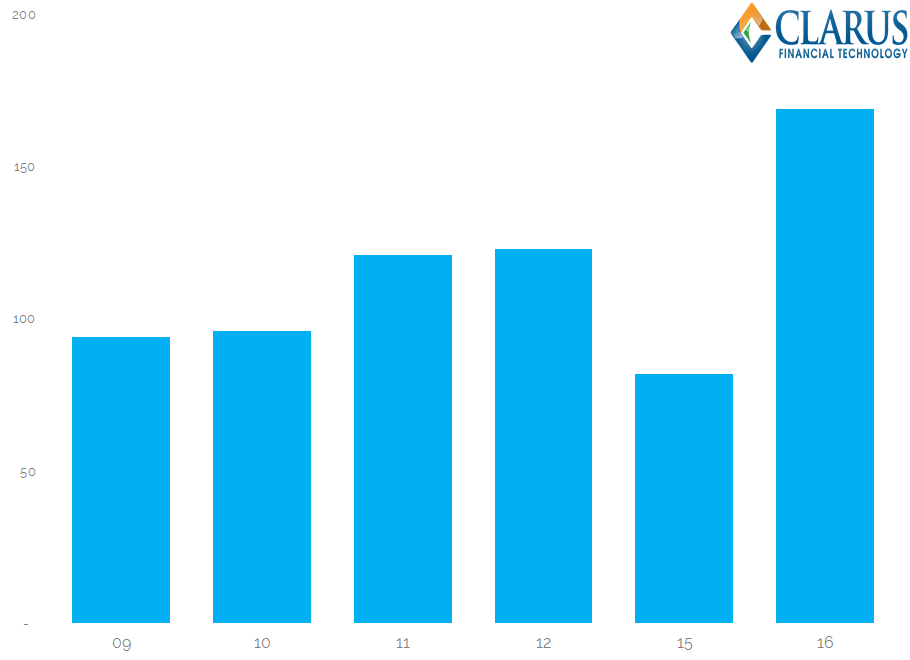

First off – are there any days that jump out as being particularly active? Looking at trade counts alone:

If I knew nothing about MIFID reporting, this would look like a fairly ordinary chart. The 16th Jan looks like a marginally more busy day than others. But then I remember that 16th Jan is a Tuesday, therefore I should see lots of nice Weekly Aggregated Volumes for illiquid swaps that still managed to trade more than once across the Tradeweb MTF in the previous week. Looking solely on trade counts, we don’t see this in the data, which strikes me as a little bit odd.

If I knew nothing about MIFID reporting, this would look like a fairly ordinary chart. The 16th Jan looks like a marginally more busy day than others. But then I remember that 16th Jan is a Tuesday, therefore I should see lots of nice Weekly Aggregated Volumes for illiquid swaps that still managed to trade more than once across the Tradeweb MTF in the previous week. Looking solely on trade counts, we don’t see this in the data, which strikes me as a little bit odd.

Trade Volumes

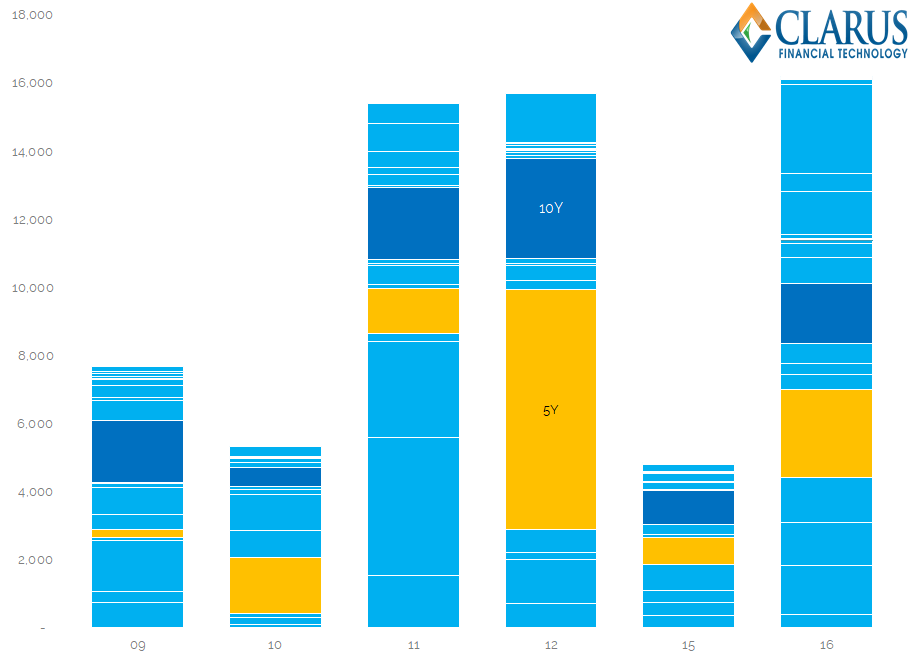

With this in mind, I looked at EUR IRS volumes. Just for fun, let’s split by maturity as well:

Showing;

- Impressive volumes. Average Daily Notional traded in EUR IRS alone was over €10bn. This is somewhat larger than we witnessed across the Bloomberg MTF, although it is a broader cut of data.

- Over €65bn total traded across the six trading days.

- It shows the importance of looking at all data that MTFs are publishing, not just the weekly aggregated volumes on a Tuesday. All of those smaller trades are soon adding up to meaningful volumes being reported within 15 minutes.

- The significant maturities in terms of volumes are 5y (orange) and 10y (dark blue).

- We see some 5y trades! This is in stark contrast to the data set we used for the Bloomberg MTF.

- Across the week, over 40 different maturities traded! In notional terms, 40% traded across just three maturities – 5y, 10y and 30y.

Trade DV01s

Let’s also take a stab at calculating the DV01s for this trade population. As we know from the ISIN debacle, we do not know the start date of the swaps. So we just have to assume spot starting.

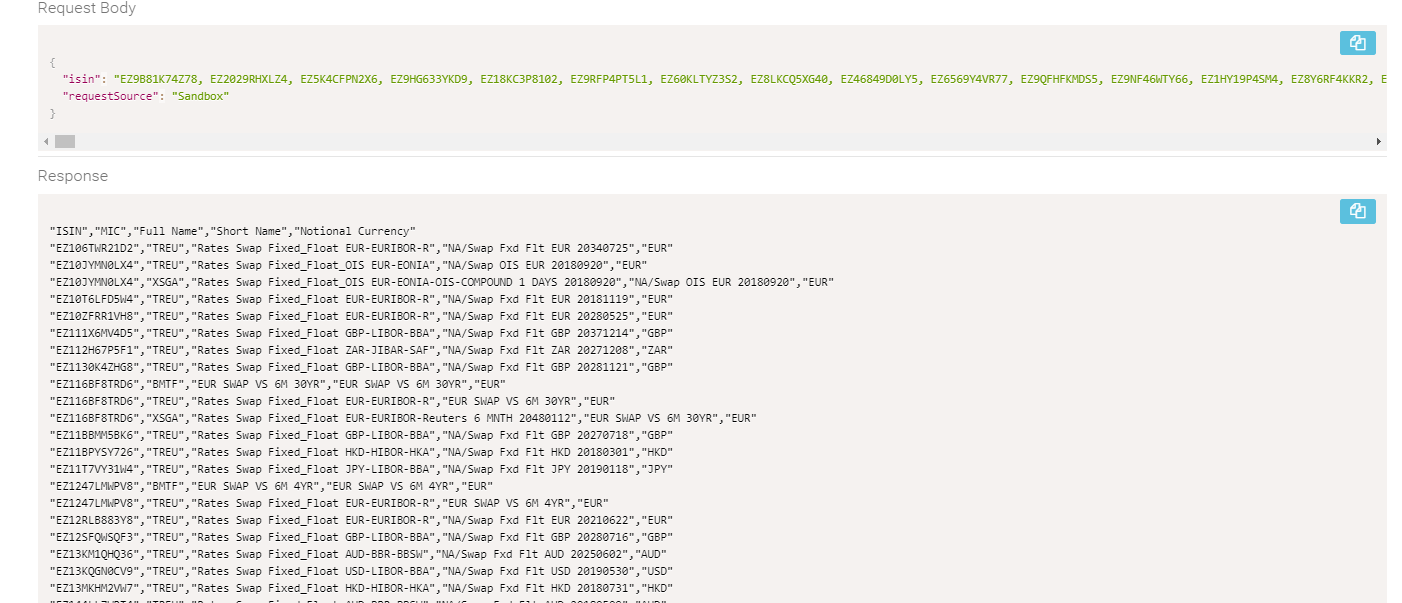

Using our Clarus Microservice, it is super simple to send all 965 (!) ISINs starting with “EZ” from the Tradeweb trade population. This covers everything reported by both the Tradeweb APA and MTF in a week. So let’s call it a round 1,000 different ISINs trading per week!

As you can see, most of the IRS ISINs were created by “TREU” (which is the Tradeweb MIC code) and they provide the maturity date in the “Short Name” of the swap. It is a simple matching job to round down the tenor of all swaps using this date.

I then import our Par DV01s using another Clarus Microservice:

Using a simple matching table, I can calculate DV01 volumes for the Tradeweb data. The results look more in-line with what we expect as MIFID II data:

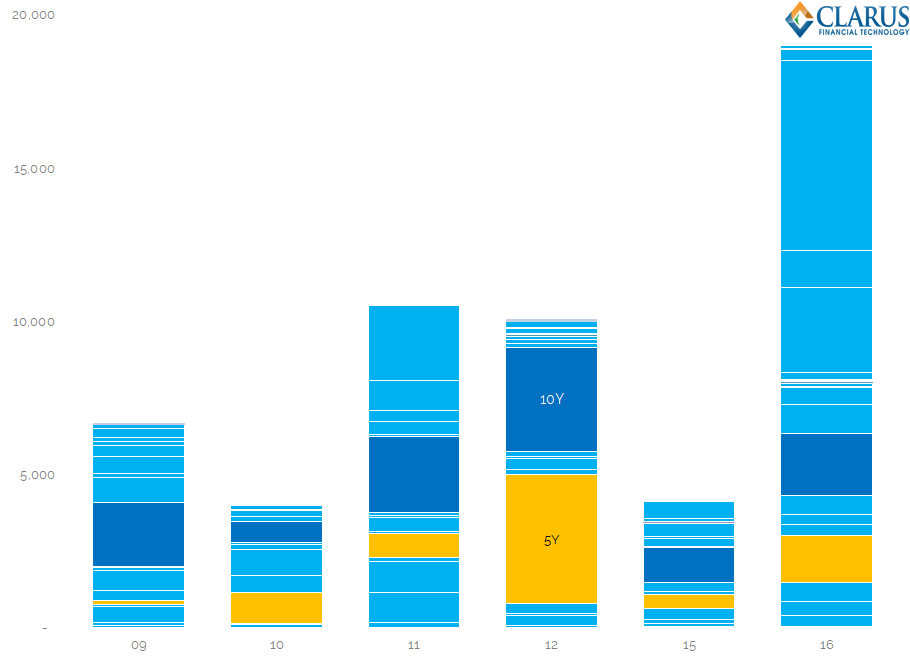

Showing;

- DV01 volumes of EUR IRS (in 1,000s of EUR) traded per day.

- There is a large spike on the 16th, which I assume is down to the reporting of weekly aggregated volumes for illiquid tenors.

- On average, over €9m DV01 trades per day across the Tradeweb MTF.

- The large spike on the 16th is due to trades in tenors between 20 and 30 years. This is where the “additional” €10m in DV01 mainly lies.

- On a DV01 basis, 43% of risk is traded across the three benchmark maturities – 5y, 10y and 30y.

In Summary – Just How Big is the Tradeweb MTF in EUR IRS?

Let’s put some perspective on these numbers.

- We reported a notional amount of €8bn across the Bloomberg MTF in an earlier blog. For this same single day, Tradeweb also reported €8bn. This was one of the smaller days in the reporting period for Tradeweb, despite it including weekly aggregated volumes.

- In the six days from 9th-16th Jan, we saw €78bn in EUR IRS reported across the Tradeweb SEF. (Source: SEFView).

- It is surprising to see that volumes in EUR IRS across the Tradeweb MTF (@ €65bn) were smaller than across the Tradeweb SEF.

- We therefore expect to see more volumes being reported across the Tradeweb MTF after the first 4 week deferral period.

- Global D2C cleared volumes in EUR IRS for these six days were €1trn (Source: CCPView).

- Data therefore suggests that most (~75%?) of the global D2C EUR IRS market remains off-venue. It must still be transacted bilaterally between dealers and customers.

- I will therefore follow this blog with a look into the Tradeweb APA data to provide some insights into off-venue trading.

- We are close to piecing together the puzzle that is MIFID II data. We assume that more data will be forthcoming after the first 4-week deferral period.