There have been many recent articles on Banks having to charge for Research as required under MiFiD II, see here, here and here, so I thought I would look into the detail.

Inducements

The relevant text in the EU Commission Delegated Directive is in Chapter IV: Inducements, the title providing a clue to the intent. This Chapter sets out the rules which an investment firm has to comply with when providing or receiving fees, commissions or any monetary or non-monetary benefits (the last two include research).

So the key point here is that the onus is on the investment firm receiving the research to comply with the rules and not on the Banks providing the research.

Article 13

Then skipping to page 26 of the Delegated Directive, we find Article 13 Inducements in relation to research.

This says that the provision of research by third parties to investment firms shall not be regarded as an inducement if it is received in return for any of the following:

- direct payments by the investment firm out of its own resources,

- payments from a separate research payment account controlled by the investment firm, provided the following conditions relating to the operation of the account are met:

- the research payment account is funded by a specific research charge to the client;

- as part of establishing a research payment account and agreeing the research charge with their clients, investment firms set and regularly assess a research budget as an internal administrative measure;

- the investment firm is held responsible for the research payment account.;

- the investment firm regularly assesses the quality of the research purchased based on robust quality criteria and its ability to contribute to better investment decisions.

- where an investment firm makes use of the research payment account, it shall provide the following information to clients:

- before the provision of an investment service to clients, information about the budgeted amount for research and the amount of the estimated research charge for each of them.

- annual information on the total costs that each of them has incurred for third party research.

So there you have it.

Investment firms are required to make direct payments for research or set-up a research payment account and charge clients with an obligation to assess the quality of research and provide budget and cost information.

There are further paragraphs in Article 13 on specifics of the operational requirements of the research payment account, but I will not bore you with those, just refer you to page 27 of the Delegated Directive.

What is Not Research?

Obvious you might say as there is a working “Street” definition. But we are dealing with regulations here, so best to be on safer grounds.

Article 12 provides some help in that it defines “acceptable minor non-monetary benefits” (which by implication are not research) as:

- information or documentation relating to a financial instrument or an investment service, is generic in nature or personalised to reflect the circumstances of an individual client;

- written material from a third party that is commissioned and paid for by an corporate issuer or potential issuer to promote a new issuance by the company, or where the third party firm is contractually engaged and paid by the issuer to produce such material on an ongoing basis, provided that the relationship is clearly disclosed in the material and that the material is made available at the same time to any investment firms wishing to receive it or to the general public;

- participation in conferences, seminars and other training events on the benefits and features of a specific financial instrument or an investment service;

Phew, sigh of relief for the conference industry. 🙂

And marketing materials and the like would not be research.

Still does not fully answer our question though.

But What is Research?

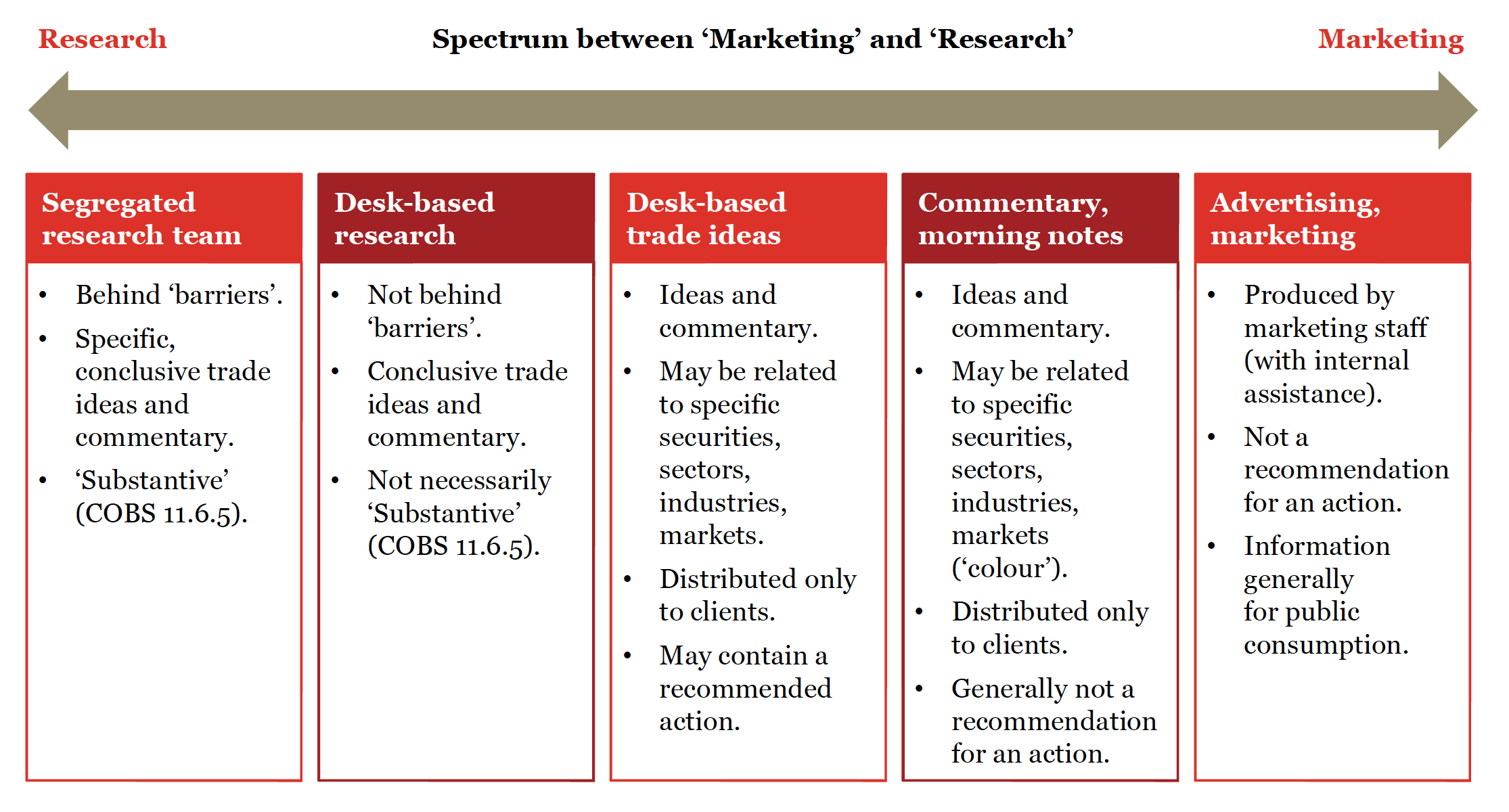

For that I like this from a PWC document titled “The Impact of MiFID II on research for investment firms“.

The implication being that the left two are research, the middle is a grey area and the right two boxes are not research. Looks like a sensible categorisation.

What Does ESMA Have to Say?

Well for that we can turn to an ESMA Q&A On MiFID II and MiFIR investor protection topics.

This has a number of responses to questions asking for clarification.

A relevant question asks “In what circumstances should material … be considered a minor non-monetary benefit … rather than research?

There is long answer the key part in which states “non-substantive material or services consisting of short term market commentary on the latest economic statistics or company results” may be treated as minor non-monetary benefits.

Whether material is substantive or not should only be linked to its content and not to the qualification given by the provider. Also that they are “reasonable and proportionate and of such a scale that they are unlikely to influence the firm’s behaviour in any way that is detrimental to the interest of the relevant client.”

For example, a detailed research report or conversation with a research analyst, ……. cannot be considered as a minor non-monetary benefit due to it being labelled as such by a provider or because such material is provided through a dealing desk rather than a research department. By contrast, short market updates with limited commentary or opinion may be capable of being considered as information that is a minor non-monetary benefit.

The restriction on inducements, including research, should also not prevent communications between a firm’s trading desk and a trader in another firm’s dealing desk in the context of seeking market information to immediately execute an order, for example on available liquidity or recently traded prices, which should be considered as part of the execution service.

Material repeating or summarising public news stories or public statements from corporate issuers (e.g. public quarterly results reports or other market announcements) could also be considered as information that constitutes a minor non-monetary benefit.

Phew. Make sense, with a fair amount of judicious copying and pasting.

Macro-Economic Research

There is a good Q&A on “Can macro-economic analysis be considered research.”

The short answer is it is likely to count as research as most macro-economic analysis is likely to, explicitly or implicitly, suggest an investment strategy (e.g. by providing views on inflation expectations, economic growth, the interest rate curve or currencies for certain countries or regions).

One exception is where material is openly available at the same time to any investment firms wishing to receive it or to the general public, for example on a website, as this could be justified as a minor non-monetary benefit.

So hence the press articles on some banks making their research publicly available and free.

FICC Research

And while a lot of the intent on Inducements covers Equity markets, lets turn to a question closer to home.

How should research related to fixed income, currencies or commodities (FICC) be treated for the purposes of the MiFID II inducements?

The short answer here is it could be either research or a minor non-monetary benefit.

More long winded from the ESMA Q&A document.

ESMA acknowledges that the current lack of established market practices and mechanisms for investment firms to pay for FICC research separately from execution costs may limit certain operational arrangements firms can adopt to comply with Article 13. Primarily, FICC markets do not currently have explicit execution commissions and mechanisms that allow research charges to be deducted alongside transaction fees. ESMA notes that firms still have the option to pay for research themselves, or using a research payment account that is funded by a direct charge to the client.

Given the commonalities between some forms of written macroeconomic and FICC research, ESMA considers that in some cases written FICC research could be capable of being priced and paid for through a subscription agreement.

There also is the option for research providers to make FICC material available to all investment firms or the general public, or for firms to receive FICC material it if commissioned and paid for by a corporate issuer or a potential issuer. In this case, the analytical input will qualify as a minor non-monetary benefit.

Some types of FICC material may also lack substantive analysis and instead represent information about financial instruments and short-term market commentary that meets the minor non-monetary exemption.

Phew. That is now really enough with the judicious copying and pasting.

But if you got this far, at least you read the key language from source documents and not journalistic paraphrasing and as any good lawyer will tell you, the devil may well be in the detail.

Final Thoughts

The onus is on Investment firms to meet the MiFiD requirement to pay for research.

Banks will need to decide whether they charge or not and how much.

Investment firms will only pay where they value the quality of the research.

At a minimum this means it should be original , draw a conclusion and not public.

Banks will need to prove the quality to get clients to pay.

Quality requires good data, analytics and expertise.

Which may require more investment by Banks in research.

Alternatively Banks may make their research public and free.

Presumably this means they can invest less in producing.

Conceding more ground to independent research boutiques.

Time will tell where the market ends up.