I wrote about Scandie swaps in October 2018. In that blog I noted that OIS doesn’t really trade. This hasn’t changed in the interim period – SDRView shows just the occasional DKK OIS trade reported. We did, however, see some SEK OIS cleared at Nasdaq OMX in April via CCPView:

Generally, it remains true to say that Scandie swaps remain tied to ‘IBOR-like indices.

I went out to investigate why, and I discovered that there was a whole lot of stuff I didn’t know about the NOK market. Amir recently described me as a “Libor geek”, so I felt like I needed to brush up my knowledge!

Read on to see what I discovered.

NIBOR

Most NOK derivatives traded today are tied to NIBOR in the Norwegian IRS market. But what is NIBOR? I thought this was a simple question, but when looking into the details, I found that the NIBOR rate is somewhat different to other ‘IBORs. From the NoRe guidelines:

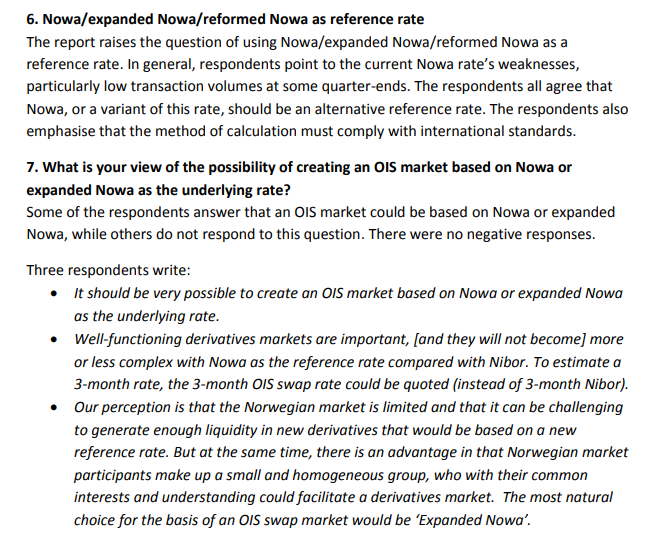

Nibor is to reflect the interest rates that lenders in the interbank market charge for unsecured loans in NOK.

Guidelines for panel banks’ Nibor submissions. NoRe are the benchmark administrator.

So far, so normal. However…

When NOK liquidity is traded in the forward exchange market, the NOK interest rate must be determined as the sum of the relevant foreign interest rate and the return derived from the difference between the spot rate and the forward rate – the forward premium (which may also be negative).

Guidelines for panel banks’ Nibor submissions

The Guidelines go on to explain that most liquidity, in volume terms, is in the forward exchange market.

So here we have a small domestic market that is choosing to use the implied interest rates from the FX forwards market to define its’ domestic interest rates. When searching for a transaction-based mechanism to define an interest rate, this has always been an attractive solution to me.

It’s probably no surprise that I, as an ex Cross Currency trader, thought this was a good idea. As far as I am aware, only the NOK market has chosen FX forwards to imply domestic rates.

NIBOR via FX – is it a good idea?

I thought NIBOR implied from FX was a great idea because:

- It is transaction based.

- FX swaps are essentially collateralised loans, with the collateralisation currency happening to be a foreign currency. This means that they are quite well protected from a counterparty credit perspective.

- Volumes are dominated in the three month and less tenors – perfect for LIBOR-type replacements.

- The USD interest rate used to define the domestic rate is well observed via transactions – either Fed Funds or SOFR.

NOK Consultation

However, the work being done in Norway on alternative reference rates

has somewhat rocked my view of the world.

The national working group have publicly consulted on rates in Norway – it is well worth a read(it is refreshingly short).

The Consultation considers a pure “Foreign Exchange Swap Rate”. Unlike NIBOR, this could be calculated based solely on observed rates, rather than asking banks to use the implied rates (“plus a spread”) to make their NIBOR submissions, as is the case today.

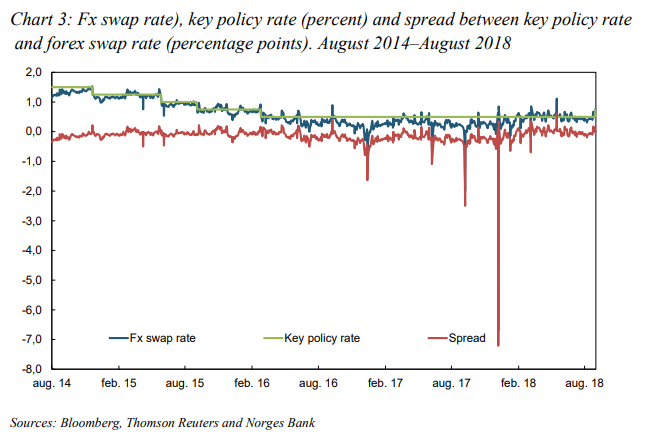

The problem? VOLATILITY. Have a look at the chart from the consultation, showing the most liquid USDNOK FX Swaps – Tom/Next. These are one day FX swaps starting tomorrow. This allows for an implied overnight interest rate to be calculated. It can be considered a “risk free rate” due to the minimal counterparty risk associated with a short FX swap (an FX swap being collateralised in the “foreign” currency).

The scale is in Percentage! And the red “spread” line shows that, at times, the implied overnight interest rate has diverged from the Norges bank policy rate by between 1-7 percentage points.

Aside from theses spikes, it is also generally volatile. Okay, it is a daily rate, therefore some volatility is to be expected. However, the extent of the volatility is certainly a negative against an FX-implied rate.

This volatility is probably why we do not see more use of FX-implied rates.

The Search for Alternative NOK Rates

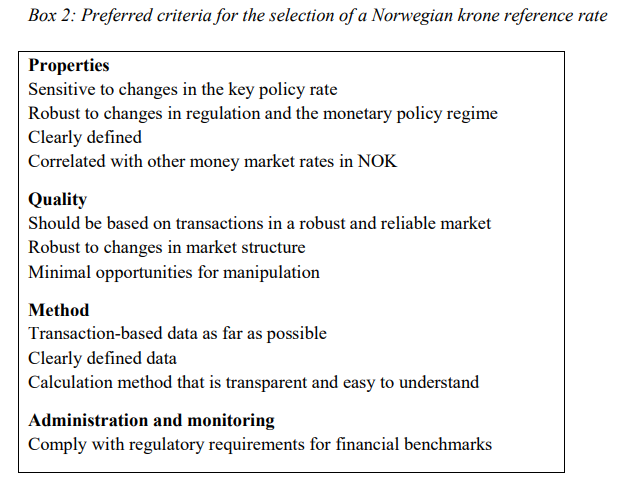

The consultation lays out the key criteria that we are looking for in a reference interest rate:

I don’t think we can argue with any of those?

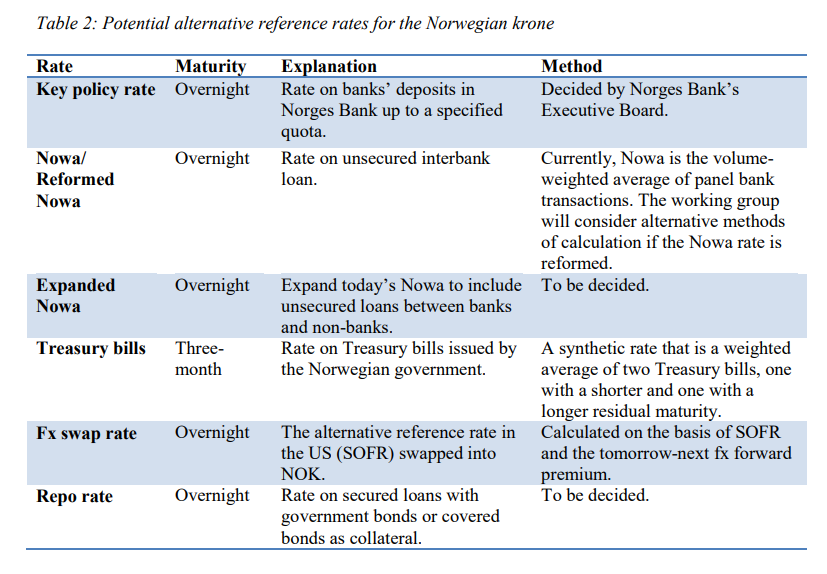

And then goes on to suggest some approaches:

Introducing NOWA

Through the consultation, I learned that NOWA, an overnight rate in Norway, has been produced since at least 2011. Details can be found here.

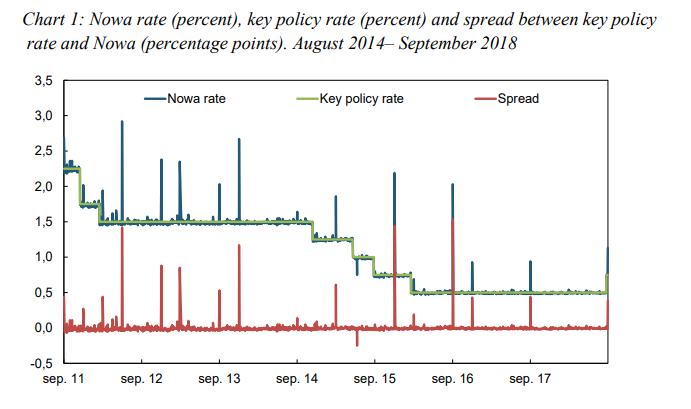

On the face of it, it sounds like the perfect replacement for NIBOR as it is generally transaction based. However, as I read more about the NOK markets, I found out that “banks are often very reluctant to lend reserves to other banks” at the end of a quarter or year in Norway. This has had the following impact on NOWA:

And the key problem is highlighted in a footnote:

Norges Bank calculates Nowa provided data is available from at least three banks and total reported turnover is at least NOK 250 million. Nowa estimates are based on figures for actual loans supplemented by panel bank estimates. Since the introduction of Nowa in autumn 2011, Nowa has been estimated around 30 times.

Footnote 9, Consultation Report from the Working Group on Alternative Reference Rates for the Norwegian Krone, October 2018. Emphasis our own.

Whilst 30 times is not a lot (less than 2% of days), it is not ideal because the days you really need some certainty are those exact days when lending markets might be constrained.

Expanded NOWA

The Consultation therefore casts an eye toward €STR, and suggests a similar methodology to create a new, Expanded NOWA. The handy chart in the consultation shows how much higher volumes would be for this rate:

From the Consultation Report on Alternative Reference Rates

Expanded NOWA would include both loans and deposits, and therefore it would inevitably be lower than the current NOWA fixing.

Work on this rate is due to continue in 2019.

Consultation Response

We are a bit late to the party with this consultation. The responses were already published and made available on 30th January 2019. You can find them here.

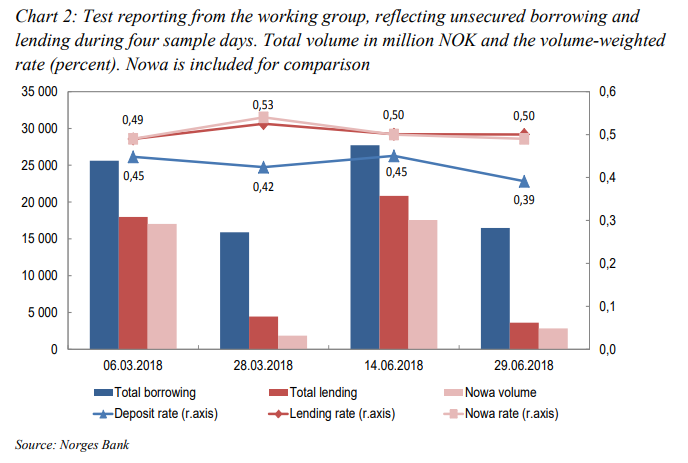

Five market participants responded to the consultation. From our perspective, it is the final answers that yield the most interesting conclusions:

Work Ahead

Finally, following the minutes of the 6th February 2019 Working Group, the path ahead for NOK derivative markets seems pretty clear. Data collection needs to start for an Expanded NOWA and there will be a further public consultation in Autumn 2019.

We will keep our eyes peeled for more information on NOWA, and keep on scanning the data for NOK OIS trades!