Since Uncleared Margin Rules started to bite in September 2016, traditional NDFs have shifted markedly to clearing in response to UMR (see NDF Volume Data). Deliverable currency NDFs have also experienced dramatic increases but with much smaller clearing percentages.

Why the low clearing percentages? Answer: there’s a whole different purpose to these trades.

I explain in detail below.

Incentives – FX Forwards vs NDFs

FX risk is normally traded using deliverable FX spot/forwards or swaps. (From here on I refer simply to FX forwards though everything mentioned applies also to spot/swaps).

- UMR exempt: FX forwards lie outside of the scope of the mandates (trade reporting, clearing, SEF/MTF/OTF trading and most notably importantly uncleared margin rules (UMR)).

- Subject to leverage and RWA charges: FX forwards contribute to Basel III leverage and counterparty credit risk-weighted assets (ccRWA) and the associated ratios. Basel III has been live for several years for trades with all bank counterparties with no sign of a shift of FX forwards to clearing in response.

Overall, there has been no evidence of a push for FX forwards toward clearing or to substitute NDFs for physical FX (or vice versa).

Something else is up.

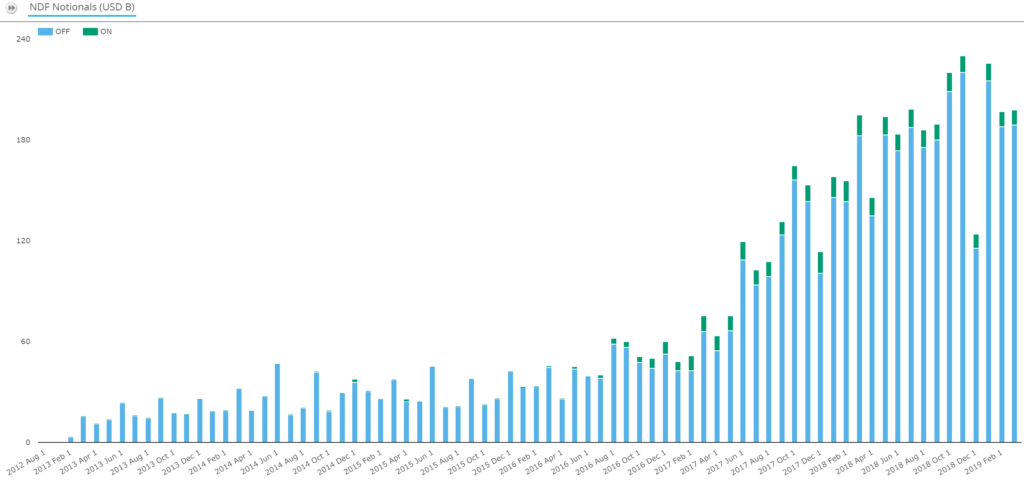

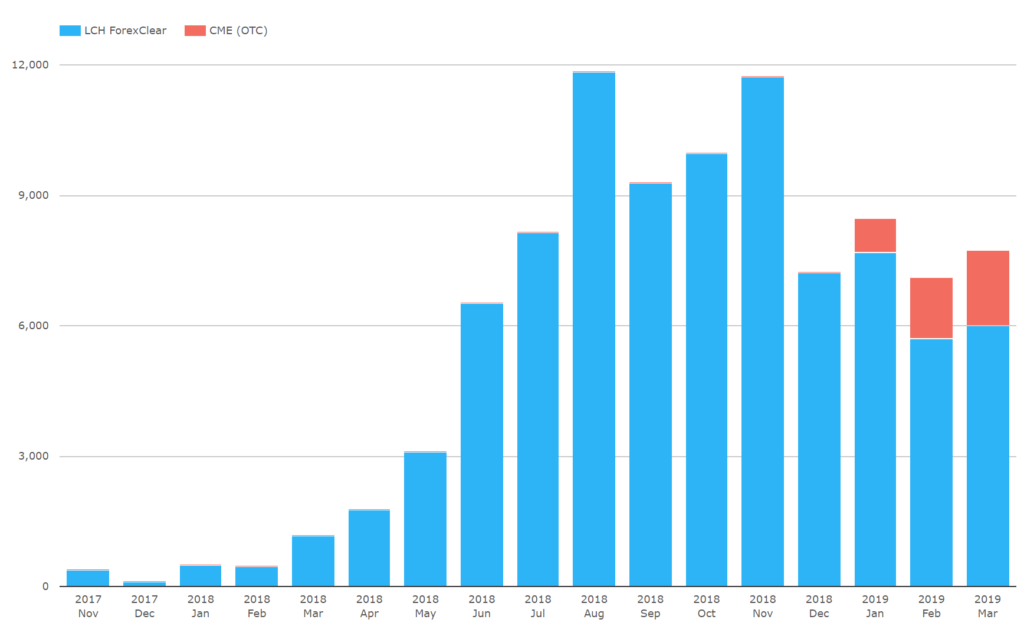

Let’s take a look at G10 NDF volumes – both US reported and global cleared volumes are below.

G10 NDF Volumes

Taking the two charts together we can see:

- G10 NDFs have been reported since the start of US trade reporting in 2012 but became material and started clearing in response to UMR 1, 2 and 3 in Septembers 2016, 2017 and 2018.

- Volume peaks came in November 2018 at $230bn US traded and $12bn globally cleared – indicating about 2.5% cleared (after doubling the US traded to account for non-US person trades).

- By March volumes declined by about a 1/3 of cleared volumes and 1/6 of uncleared from November

- LCH ForexClear is the primary CCP for these volumes, with CME starting in Jan 2019 and reaching about 20% in the most recent month.

Before we explore further let’s do a quick aside about FX risk and ISDA SIMM.

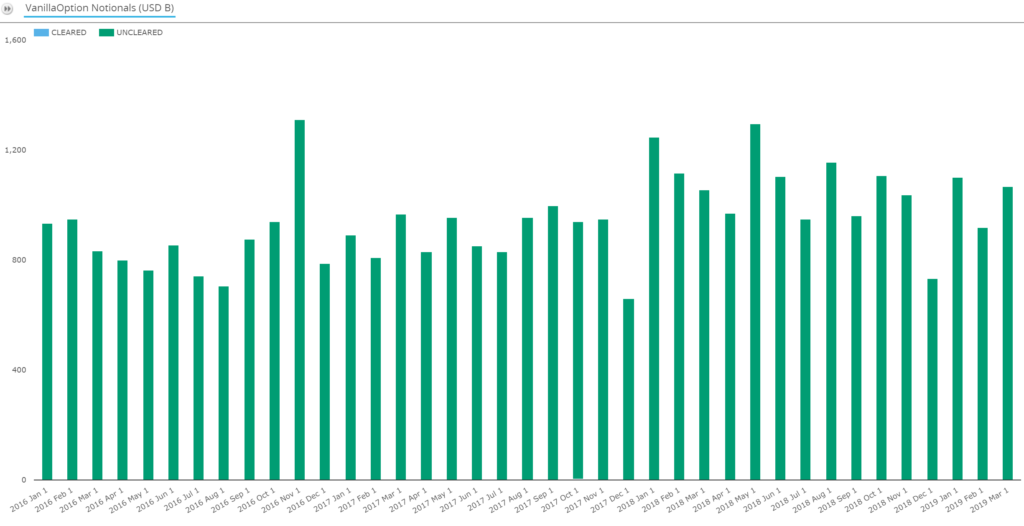

FX Options dominate SIMM FX risk

FX products in-scope of UMR and therefore in the SIMM portfolio for a given counterparty include: FX options, NDFs, NDOs.

- Cross-currency swaps are in scope of SIMM but the FX principal exchange is exempt – so we can ignore.

- NDO’s are very small in notional – so we can ignore.

- Per above there’s no trading reason to use deliverable currency NDFs.

Therefore, the pre-existing currency FX delta and vega in SIMM is all down to FX options. And options trading volumes are chunky.

We can see:

- US reported volumes averaging $1.1tn per month in 2018 (up from $0.9tn in 2017). BIS H2 2018 showed us $13.3tn global notional outstanding.

- With a probable weighted average maturity (WAM) of less than 2 years, D2D volume should mostly have transitioned to SIMM after UMR 1/2/3 with D2C to come after UMR 4/5.

How can SIMM IM be optimised using NDFs?

Let’s think this through a bit:

- FX Options clearing only emerged in March 2019 as a daily occurrence for EURUSD and AUDUSD. This cannot explain 2018.

- FX options SIMM contribution is dominated by FX delta. Anecdotally, it breaks out on average ~10:1 delta vs. vega (though portfolios and trades vary a lot). FX delta optimization is the first priority.

- If we can’t clear the FX option, we can reduce its delta by offsetting with an opposite direction FX delta trade. For this:

- FX forward – the natural choice – won’t land in the SIMM portfolio. Won’t work in reducing IM.

- Deliverable currency NDFs would work (no FX pair delivery). Could work.

- Synthetic FX forwards (same strike put and call FX option collars, with FX pair delivery). Could work.

- We need to neutralize the market risk effect of the offsetting trades to avoid trading new market risk.

From my prior post, there are two ways to use deliverable currency NDFs to do the offset in a market risk neutral way.

- Risk compression (using uncleared NDFs only). With more participants, a higher percentage of date, counterparty and currency pair delta positions are completely offset or offset up to the limit of risk tolerances set by the participants. A lower percentage of delta positions will be both non-zero and available for further reduction within risk tolerances. Risk tolerances among other things may address concerns that further reduction of SIMM risk will uncover non-SIMM risk and therefore increase ccRWA.

- Delta clearing (using equal and opposite uncleared and cleared NDFs). The same risk tolerance applies here about not wishing to uncover non-SIMM risk / increase ccRWA. In addition, risk tolerances need to be set here depending on a participant’s appetite for CCP facing FX delta and the associated IM.

Putting the whole picture together

You may be asking one or more of the questions below.

- If there is a margin penalty, why from nothing has the uncleared market grown to $230bn a month? Optimisation offers a margin benefit not a penalty. The purpose in both 1 and 2 is to offset FX delta in the SIMM portfolio reducing risk and IM.

- Why have so few of the uncleared G10 NDFs cleared if CCP IM and counterparty netting normally favor clearing? Only a small fraction of the total risk positions can be converted to clearing. This is covered by the explanations under approaches 1 and 2 above.

- Does the data bear out approaches 1 and 2? I will spell out the stats in a follow-on to this article. The relative sizes are explained by the answers under 1 and 2 above. Looking at daily NDF volumes, I see a pronounced weekly and monthly pattern in the SDRView and CCPView NDF volumes. This strongly suggests that 1 and 2 are both happening and being driven by third party compression provider(s) or SEFs. Only compression vendors can do approach 1 – risk compression. Approach 2 can be done by a pair of counterparties in isolation. However, the regularity of the clearing volumes and also the prominent press releases from Quantile noting it’s facilitation of G10 NDF clearing at LCH ForexClear and CME suggest third-parties are the major driver.

- Have G10 NDFs peaked? If so why? It’s too early to tell. This may be just FX market volume driven (e.g. FX Options declined also). Or may be because other techniques are becoming more prominent for 2019.

- Is the volume materially optimization driven? I believe so. I will lay out more in a follow on to this article to explain this view.

…and some possible gotchas / alternatives:

- How limiting are the risk tolerances? Banks might want – for simplicity and certainty of progress – to constrain all metrics to improve. No trade-off decisions are then required between metrics. This can however limit effectiveness of each technique. Ultimately, if a lot of delta remains in SIMM, this will be an opportunity for other optimization techniques to compete with 1 and 2.

- How bad are the leverage costs? I am unclear whether the extra NDF leverage forms a major constraint on the effectiveness of techniques 1 and 2. It sure hasn’t stopped them yet. I believe the vendors are quite smart at minimizing these effects as part of their runs. In any case, it is worth restating that despite signs to the contrary from the reported leverage increase, the counterparty risk is actually going down!!

- What about delta conversion to non-SIMM? Possibly but how much is the question. Pairs of parties can use non-SIMM FX forwards and offsetting SIMM synthetic FX forwards to convert FX delta between the two portfolios. I will cover this in a separate article on FX forward optimization.

- What about vega risk compression? I’m not sure whether this has become material or not. The monthly FX options volume increase in 2018 seems enough to include the onset of material vega risk compression. Given FX options have an innate trading purpose (unlike G10 NDFs) it’s harder to separate risk compression patterns dis-aggregated from the daily trading volume. I don’t recall seeing anything in the press on this. Another topic for a future post.

Conclusion

The data seem to support G10 FX option FX delta compression and conversion. I will lay out daily data evidence in a follow-on to this article.

How limiting are the constraints on the effectiveness of approaches 1 and 2? This will be determined by how much SIMM IM is left to be optimised.

These include vega risk compression (using FX options), delta conversion to non-SIMM (using FX options and FX forwards) or FX option backloading to clearing.

All of these are possible but the practical scale is the question. I hope to do a couple more articles on these. Then I will have laid out a rounded summary of what’s going on.