Our regular readers will know that the Clarus Blog focuses on Derivatives and the new regulations introduced after the Financial Crisis of 2007-08. The massive increase in availability of data on OTC Derivatives markets is of great interest to us. However at times we are guilty of not paying enough attention to older data sources.

Today I will look at one such source, namely U.S. Bank Call Reports, jargon that I have sometimes heard colleagues in the industry refer to and I have nodded sagely in agreement; well time to find out more.

OCC Report

The Office of the Comptroller of the Currency (OCC) produces a Quarterly Report on Bank Derivatives Activities, based on information filed in call reports by all insured U.S. commercial banks and trust companies.

This report has been produced each quarter since 1995, so the current is the 87th edition!

All reports are available on the OCC site here.

Lets look at the latest report.

Second Quarter 2017

First point to note is that a total of 1,418 insured U.S. commercial banks and savings associations reported derivatives activities! Wow that is a lot more firms than I would have imagined.

The second point to note is that a small group of firms dominate activity; four large commercial banks (Citibank, JP Morgan, Goldman Sachs, Bank of America) represented 89.6% of banking industry notional amounts and 86% of industry net current credit exposure in 2Q 2017.

The report has separate figures for U.S. Insured Commercial Banks and Bank Holding Companies (BHC) and I will focus as much as possible on the latter as BHCs represents a more complete picture of trading revenue in the banking system. (Recall that since the Financial Crisis former Investment Banks such as Goldman Sachs and Morgan Stanley adopted BHC structures).

Trading Revenue

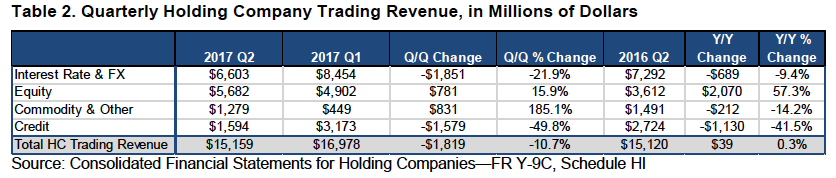

One of most interesting figures is data on Trading Revenue, so lets re-produce Table 2 from the report.

Showing:

- Total revenue of $15.2 billion for BHC in Q2 2017, down $1.8 billion on the quarter

- Interest Rate & FX the largest with $6.6 billion, down 22% in the quarter and 9% Y/Y

- Equity the next largest with $5.7 billion, up 16% in the quarter and 57% Y/Y

- Credit $1.6 billion, down 50% Q/Q and 41% Y/Y

- Commodity & Other $1.3 billion, up 185% Q/Q and down 14% Y/Y

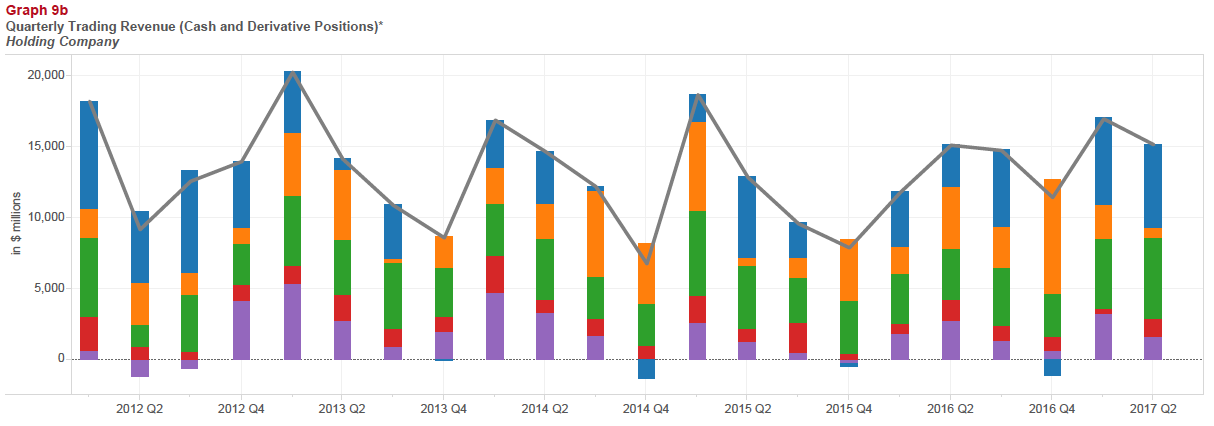

Longer term data is shown in the Appendix.

IR is generally the largest revenue asset class each quarter

4Q 2016 was an exception with FX the largest and IR showing a loss

Equity is generally the second largest revenue asset class

Credit shows the greatest variability in quarterly revenue

The most profitable overall quarter was Q1 2013 with $20.3 billion and the least profitable Q4 2014 with $6.8 billion.

In the years 2012-2015, Q1 has the highest trading revenue and then a drop, but this pattern changed in 2016 with Q2 and Q3 higher. No quarter shows an overall loss, but IR shows losses in Q4 for 2013 to 2016 and CR for Q2 & Q3 2012.

Interesting data indeed.

Market Risk

Value-at-Risk is used to control market risk in trading operations and the trend in figures for these are interesting (though not directly comparable between firms due to differences in methodology).

Showing a pronounced downward trend at each bank, largely due to the extended period of lower market volatility since 2008 and a reduction in market risk appetite at firms.

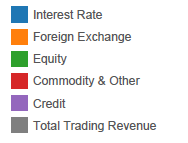

OTC vs Centrally Cleared

There are interesting tables and charts on the stock of derivatives that are centrally cleared compared to over-the-counter. Extracting just the IR, FX and EQ tables from Graph 15, which is for Insured US Commercial Banks and not Bank Holding Companies.

I assume Centrally Cleared here represent Futures as well as Swaps that are Cleared and we can see that while IR is similar between Cleared and OTC, in both FX and EQ the OTC notional is much larger. (The same is true in Credit).

Credit Risk

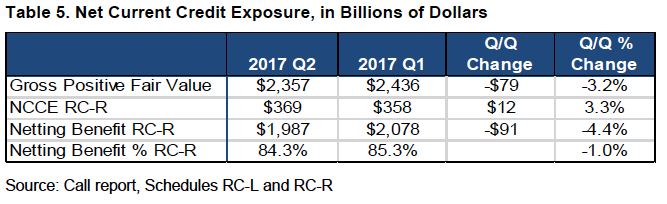

Net Current Credit Exposure (NCCE) is the primary metric that OCC uses to evaluate credit risk in derivatives and Table 5 provides a nice summary.

Showing that a Gross Positive Fair Value of $2.4 trillion is reduced to $369 billion of NCCE RC-R, a netting benefit from legally enforceable netting agreements of 84%.

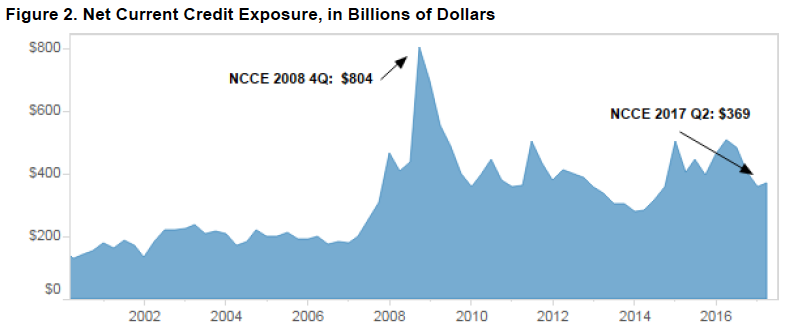

As the above figure shows, NCCE peaked in 4Q 2008, during the financial crisis, when interest rates had plunged and credit spreads were vey high. (There is an extended write-up in the Quarterly report on the trend since).

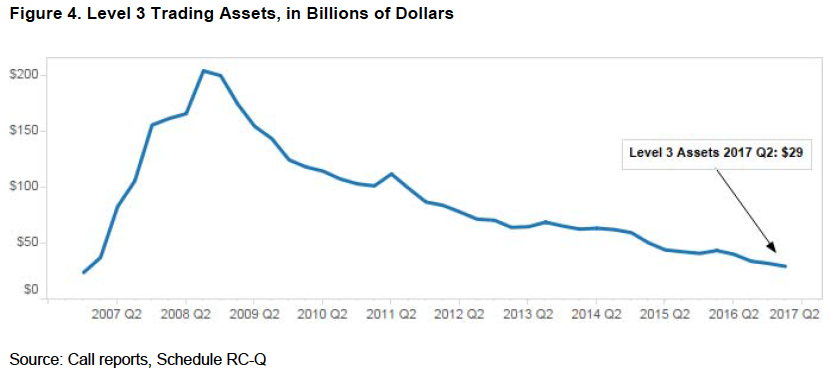

Level 3 Trading Assets

Level 3 trading assets are assets whose fair value cannot be determined by using observable inputs such as market prices.

These peaked at $204 billion at end 2008 and in the most recent quarter banks held $29 billion, which itself is 33% lower than a year ago and 86% from the peak.

The End

There are lots of other graphs and tables in the Quarterly report.

Unfortunately I am out of time to look at these.

In particular the tables in the Appendix.

A task for another day.

In the meantime, please visit the OCC site for the current report.

Or check back for our take on the 3Q 2017 report.