Last week we put out a joint press release, see AcadiaSoft Partners with Clarus Financial Technology to Provide Joint Initial Margin Analytics Service and I wanted to provide more detail on the value of this.

Background

Uncleared margin rules (UMR) require firms to exchange Initial Margin on bi-lateral derivatives exposures and the financial industry relies on the AcadiaPlus platform and in particular IM Exposure Manager for reconciliation, calculation and dispute resolution of IM.

Reconciliation here means not just comparing margin figures, but where there are material differences, comparing the underlying risk exposures that are the inputs to calculate IM. Consequently every financial firm that is live with UMR, sends its Common Risk Interchange Format (CRIF) files to the AcadiaPlus platform.

Our partnership means that a firm can authorise us to get this data in our CHARM service.

Why is that Important?

As a provider of Software-as-a-Service (SaaS) solutions, we want our customers to get value in week one of signing up with us and not after a 1-year implementation project. Meaning that a customer’s data needs to be available with zero integration effort.

We expect nothing less on our smart phones, when we download an App and authorise it to get our data from Apple, Google, Facebook, etc.

We should expect the same in enterprise SaaS solutions, barring the difference that authorisation is not granted for self-use by a user but by an authorised person for the firm.

Using CHARM

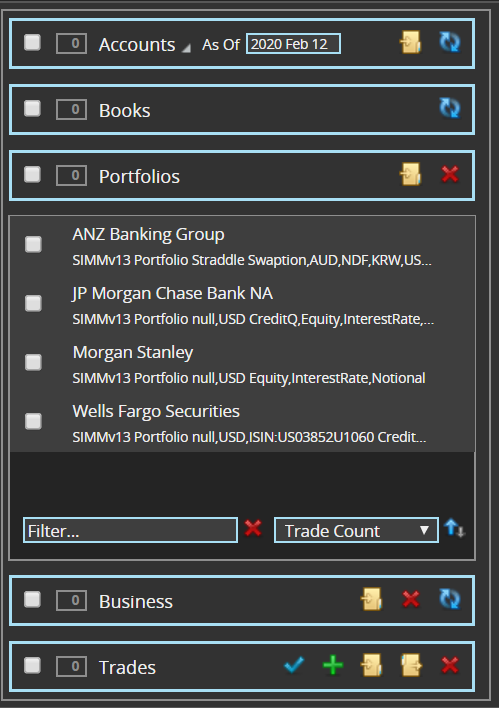

Now when a user logs into CHARM, they see a panel with their counterparty portfolios.

Selecting any or all of these to calculate IM.

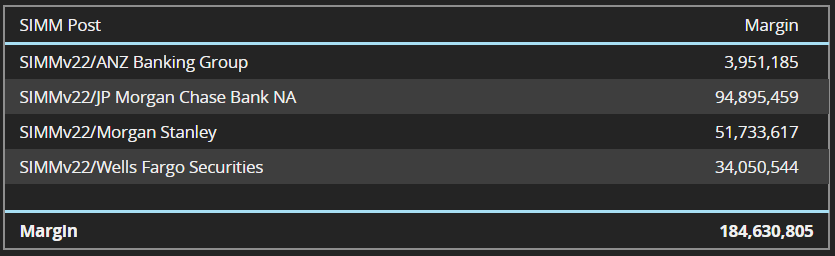

Showing an overall gross IM of $184 million, of which two counterparty portfolios are above the $50 million IM threshold above which IM needs to be pledged.

We have our start-of-day baseline IMs for each and every counterparty portfolio from CRIF files received from AcadiaSoft.

Intra-Day Use

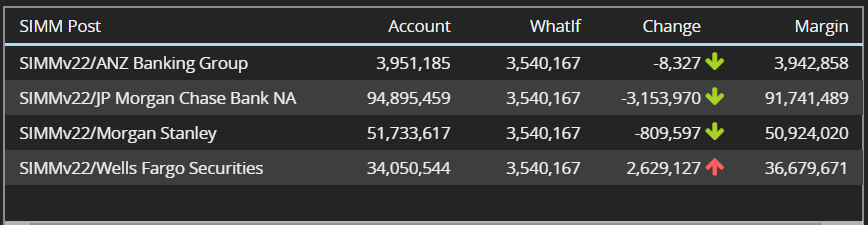

Next we can enter a what-if-trade and assess the impact.

Showing that for the same what-if trade (in this case a Swaption) the IM would decrease the most for JPM, increase the most for Wells, while MS would move within $1 million of the $50 million threshold.

Useful functionality for large trades that materially move IM.

Even more important for monitoring only counterparties, as for these threshold limits will be set below $50 million, say $30 million, due to the fact the custodial, legal and operational infrastructure is not in-place as is not required until the threshold is crossed.

Intra-Day, End of Day and Next-Day

When trades are executed during the day, customers can enter these in the CHARM GUI or use an API to update the state, so that the next what-if calculation has the most up to date state.

At end of day, a firm has a good estimate of the change in IM for each counterparty portfolio.

And next day we start again by loading CRIFs from AcadiaSoft.

No overhead in using our own database of trades and having to keep this in sync with a golden source.

An example of a more efficient post trade infrastructure.

There is More

There is more to see and use.

Please contact us to schedule a demo and discussion.

To learn how you can benefit from our AcadiaSoft partnership.