I’ve been pondering the appropriate spread between LCH and CME. It would seem to me that every firm should have their own true cost of putting on a swap at CME or LCH, based upon a multitude of factors not limited to how they are currently positioned.

I thought it worthy to explore what these parameters are, and see if one could arb the CME/LCH swap market. After all, the swaps held at each clearing house have no combined market risk, complete with offsetting cashflows held in secure accounts. One would assume there exists some opportunity to receive the higher fixed rate at CME and pay fixed at LCH. Do the economics of OTC clearing allow for this at current market rates? At what point does it make sense?

Headline Winner

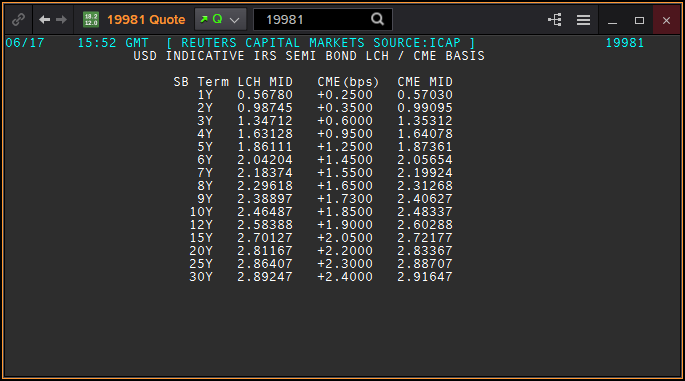

Let’s take a look at the ICAP SEF screen for 17 Jun showing the following indicative mid prices for the switch trades:

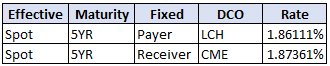

One would think by simply being a payer at LCH and receiver at CME, I could lock in some profits, for example 1.25 basis points on a 5 year swap. On a 100 million USD swap (average 5Yr notional) that would be $12,500 per year, or $62,500. Easy money. Let’s do that.

Just open your account

So let’s go through what this might entail.

First, to keep things simple, let’s assume I am an indirect client. Call me a private hedge fund, a floor trader, a wealthy investor, or whatever terminology means that I do not have any overheads, capital ratios to maintain, or prying investors to answer to. In this example, I am trading out of my parent’s basement. 60+ grand will buy me some beer and that new Katy Perry album.

Having said that, I’m going to ask you to also believe I have a solid line of credit to borrow funds, and am able to find an FCM that will take my swaps business. Just play along here.

Running the numbers

So in order to determine this is a sure thing, we need to run some numbers. Let’s start on the income side of the equation. Step one, I sign up for my free trial to CHARM by calling the guys at Clarus. Then I load up the following trades you see to the right.

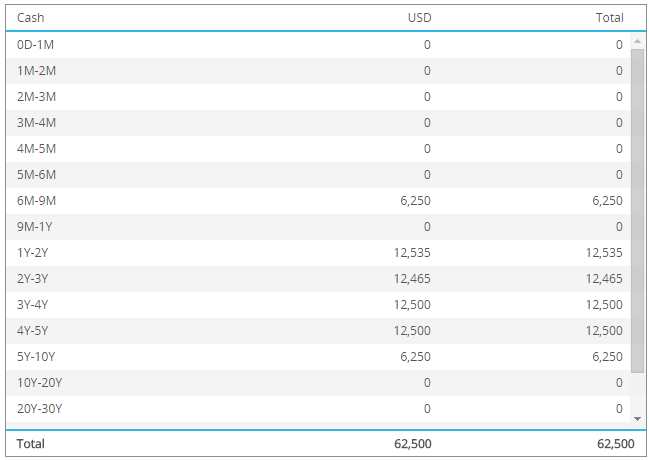

Running a simple cashlow report, I can clearly see that 62,500 coming in over the next 5 years:

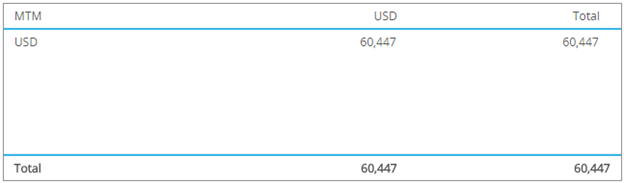

And assuming this is struck at a mid-price, the immediate mark-to-market will of course be zero, given that my LCH trade is revalued at LCH prices, and CME trade is revalued at CME prices.

However I need to be aware that over time, as the basis moves, I’m exposed to mark to market gains and losses, and hence there will be variation margin payments. But importantly because both CME and LCH are fixing off of the same 3M Libor, my floating coupon payments will always offset.

If I use a risk-free curve (or just choose CME or LCH alone) to value my position, I should see the MTM / present value of this 62,500:

Let’s now look at the cost of putting on and carrying this position over 5 years. I believe there will be the following costs:

- Execution fees.

- Clearing fees (payable to FCM & Clearing house):

- Trade Booking Fee

- Trade Ticket-based Maintenance Fee

- Monthly Minimum Fees

- Portfolio IM-based fee Charge

- Required funds (payable to FCM):

- Variation Margin

- Initial Margin

Let’s step through these.

Execution fees

Bloomberg SEF offers trades at $10, however I believe I’d have to pay a few thousand in terminal fees every month to have that luxury. Few thousand x 12 months per year x 5 years comes to many thousand before you add that $10. Most SEFs have their own pricing plans ranging from all-you-can eat to ala carte to limited time free.

I should mention the basis market really only exists on the IDBs at the moment. If I wanted to trade a CME/LCH switch I might have to leg into it on a client SEF and eat the spread on each side.

For our purposes, I am going to assume my parents have a Bloomberg terminal in the basement, and I can trade at mid. Trading at mid always works in grade school finance. So at 10 bucks per side, the total cost is $20. Great, I’m on my way to $62,480.

Clearing Fees

The world of clearing fees seems quite competitive and complex. For starters, a client is charged fees raised by both the DCO as well as the FCM.

The DCO’s have different schedules (CME and LCH) designed for either “standard” or “active” clients whereby:

- Trade booking fee (either $ per million in “standard” schedules or a flat fee in the “active” plans). Looking at the schedules for our 5 year swap these seem to be ~$4 per million “standard” or $25 “active”.

- Maintenance fee (either a $ per million in “standard” schedules or a risk consumption fee which is a % of IM in the “active” schedule). Looking at the schedules it would seem to be $2 – $3 per million per annum on the standard schedule.

This is what it looks like in a table for our single $100mm swap package. We need to figure out what that 10bp of IM equates to. We’ll get to that in a minute.

Regardless of what the DCO is charging me (via my FCM), my FCM has more unpalatable fee schedules. Amir has previously cited some of the clearing firm’s EMIR-publicly-disclosed fee schedules, which I believe are still roughly accurate. And in speaking to a few FCMs I’m led to believe I need to assume at a minimum:

- Trade booking fee should be ~$1,000

- Maintenance fees run anywhere from 10 – 100 basis points on IM, charged periodically. A recent Risk Magazine article by Peter Madigan discussed one FCM raising this fee by 75bp (not to 75bp, but by 75bp).

- There are typically monthly minimum fees that run into the tens of thousands of dollars.

For the purpose of my analysis, I will assume $1,000 ticket fee and the most ridiculous 10bp on IM. (I got a great deal because I am financing my basement washer/dryer from this same firm). Further, I negotiated zero monthly minimum fees.

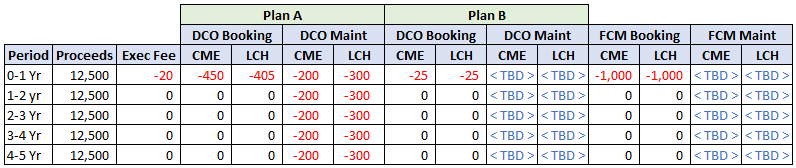

So let’s look at a schedule of proceeds and costs as it stands:

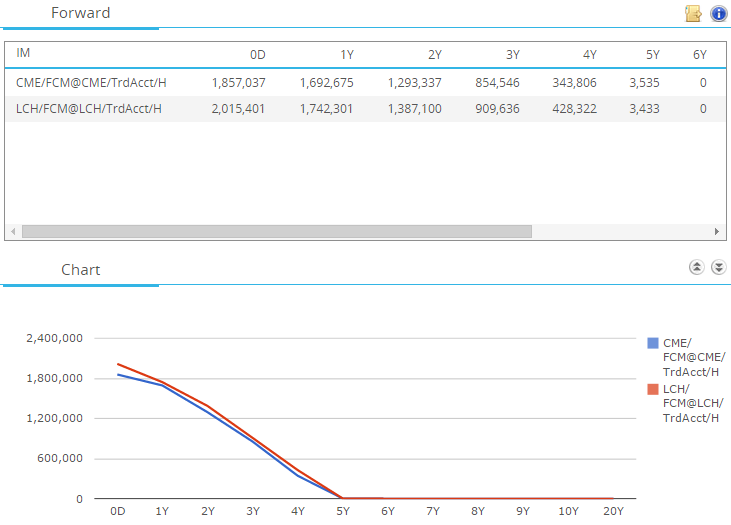

So it would seem that in order to determine my most economical approach, we need to understand what my initial margin will look like over the life of this trade. So I go back to CHARM to see the 5 year forward analysis of initial margin, which shows me how my margin will behave over the life of the portfolio.

This helps complete the picture. Let’s plug these into my table to see which DCO plan I should be on.

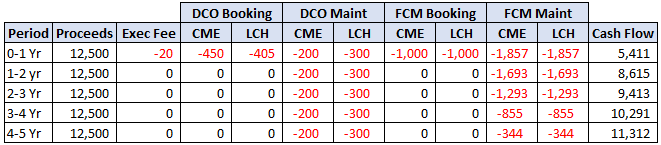

The DCO’s (and FCMs) charge periodically upon an average IM usage. In my example, I have taken some liberties by treating the IM as a step function. However it is pretty clear that I should be on the pay-as-you-go plan (plan A) that has a flat per-million maintenance fee. Let’s use that. Here is my cashflow schedule:

The final column shows my expected cashflows. Nice solid gains every year. Trading the swap market is easy from a basement. But my $62,480 gain is now down to just over $45,000.

Raising the funds

Now we just need to line up some funding for our first margin call. As we saw, my day 1 Initial margin comes to roughly $3.9 million and tapers down over 5 years. While I could fund this overnight, if we really are going to attempt some arbitrage we better lock in 5 years of funding, which I will do in 1 year increments. Pulling some 1 year forward rates from my curve, and after mortgaging my parents basement (it has a dartboard), my bank agreed to finance my annual obligations at the following rates. Note the forward curve is fairly steep:

Kicked out of the basement

Alas, given all of my very favorable assumptions on overhead, SEF execution, and FCM fee structures, it becomes clear that this just isn’t going to work. Even if I am willing and able to fund at overnight rates (maybe 15bp for a while) this starts to become murky. Further, even if I assume my investors are happy using firm capital to fund the margin, I am not beating treasuries.

And really, 10bp FCM IM maintenance fees are not happening. Plug in 50bp and the analysis starts to become more credible (and further loss-making). In fact let’s recap all of the assumptions that are way too aggressive:

- Zero overhead.

- Negligible execution fees.

- FCM giving me 10bp maintenance fees.

- FCM not charging minimum monthly fees, when in fact some FCM’s have recently jettisoned some paying clients.

- No accounting for variation margin obligations (which, when considered with PAI, is fair).

- I have used “house” Initial Margin calculations. True client margins that most FCMs would charge are 10% higher.

- I have assumed I can deal at mid price, and that taxes are zero.

- I’ve assumed annual granularity for proceeds and fees in order for the analysis to be palatable. One would need to get more explicit.

Worth noting as well that all of these numbers (except execution fees) scale with position size at LEAST linearly. So it’s not fair to say “well just do 100 billion instead”. In particular, as I add size, clearing house initial margin add-ons scale super-linearly which magnifies the primary cost component in all of this algebra.

Finally, I’d acknowledge this is not a true arb as even if we secured funding, some of these components just cannot be locked in or predicted with certainty.

Don’t leave your basement just yet

So clearly the arb will not work at current prices and assumptions. But surely there is a price whereby this strategy becomes profitable for me.

Now that we have all of the parameters readily at hand, we can simply compute my personal breakeven rate:

So all I need to do is wait for the 5yr basis spread to go above 3.932 bp, and I’m in the black.

Whats the point

If I had more appetite, I’d look at an existing directional book that is indicative of a swap dealers positions, and look at both directions.

But the point is that each firm already knows all of the parameters and each firm is starting with a portfolio composition that is unique to themselves (mine was of course 0). Given these parameters, we can compute a break-even rate for each firm to put on basis trades in each direction.

Many firms should discover they have a natural axe to play with, they just haven’t found that axe in the basement yet.

The largest component of computing this break-even rate is your forecasted margin, and how it behaves over time.

For that, you need CHARM.

Call us from your trading floor (or your parent’s basement) to find out more.