- Derivatives transparency allows us to monitor the continuing activity in RUB markets.

- Interest Rate Swap activity in RUB spiked in response to the central bank action this week.

- And Russia is a component of the CDX.EM CDS index, where trading continues despite huge event risks.

- FX markets are a little more opaque, but we see an increase in USDRUB NDF volumes which we can continue to monitor.

I doubt anybody needs any introduction as to why this blog is being written today. So let’s take a quick look at what has been trading in RUB derivatives markets:

RUB IRS Markets

Russian banks are being frozen out of international markets. However, other banks still have Russian exposures that need hedging. As the central bank hiked rates to stabilise the currency, RUB Interest Rate Swap markets saw a large spike in activity:

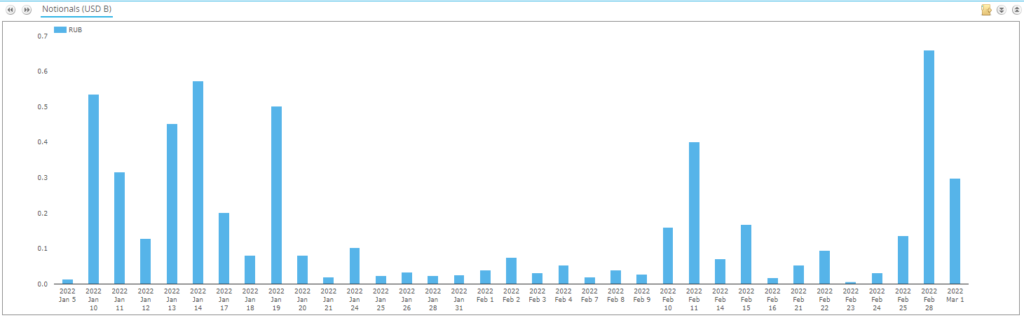

From SDRView, we saw that the 28th February was the largest trading day in RUB IRS so far this year:

Showing;

- USD660m equivalent of RUB IRS traded on Monday 28th February – the highest notional amount this year, and the 11th busiest day in the past year.

- That compares with less than $200m notional trading per day in the prior 8 days.

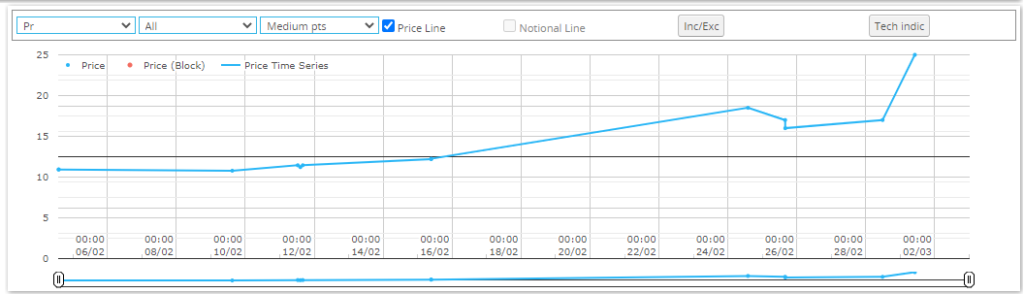

- As you would expect, the chart from SDRView Pro shows how starkly Rates increased, last printing at 25% in spot starting 2 year swaps:

- As you might expect, this is not the time to be shopping around for a quarter or half a basis point on your trade! Anyone needing to trade will be checking all of the big figures in markets like these.

- There are plenty of IMM dated trades hitting the SDR, suggesting a few things:

- Hedge funds are active. These market participants are typically the largest users of forward starting structures.

- Talking of forward-starting trades, anyone who cannot just close their exposures may look to roll their trades to a future date. If you can’t get outright prices, you may at least be able to get a price to roll positions from March to June.

- There have been some spot starting trades hitting SDRs each day. However, remember that even a spot starting interest rate swap does not create any cashflows today (or even value spot). The first cash flows due on these trades will be in three months time from now.

- It is old trades that may struggle to settle in times like these.

Old IRS Trades

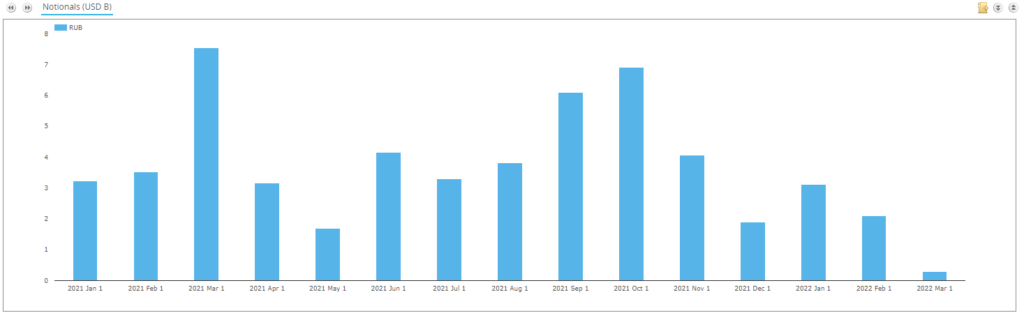

Talking of old trades, it is therefore relevant to look at activity over the past year and look for any particularly large days that could have large coupons due to settle (of course we could do this for all trades ever reported to SDRs, but this is a blog, not a data science experiment);

What do we see?

- The busiest month in 2021 was March, when over $7.5bn equivalent of RUB IRS was reported to US SDRs.

- This is relevant NOW because all of those trades (and I really do mean all) carry annual coupons on the fixed legs.

- Therefore all of that great business written back in March 2021 (which really was a different world) suddenly carries a completely different risk profile.

- Those annual coupons will be coming due this month.

- Obviously, there are caveats here:

- This is an incomplete view of the overall market.

- Coupon payments are a small percentage of the face value of an interest rate swap (varying from 5.19% to 7.3% when they were printed last year).

- We do not know the distribution of risk that these gross notional amounts represent. In an ideal world, everyone is risk neutral!

- The credit profiles of uncollateralised Pay Fixed and Receive Fixed interest rate swaps are vastly different in times like these. Why? Because it is only the Fixed coupons which are annual payments, with the floating payments quarterly. Therefore if I paid Fixed last March, I will already have received 3 floating coupon payments from my counterparty.

- It is the Receive Fixed interest rate swaps that will be garnering a lot of nervous looks from credit managers, risk departments and senior folk on trading floors as this crisis unfolds.

To point out the obvious, we haven’t heard anything about RUB Interest Rate Swaps failing to settle – or even RUB FX trades – but it is surely a sensible use of public transparency data to try and assess the risks out there.

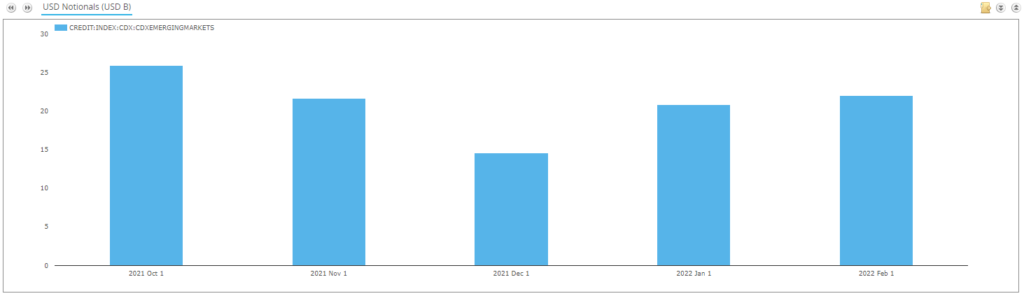

RUB CDS Markets

Are any CDS actually trading?

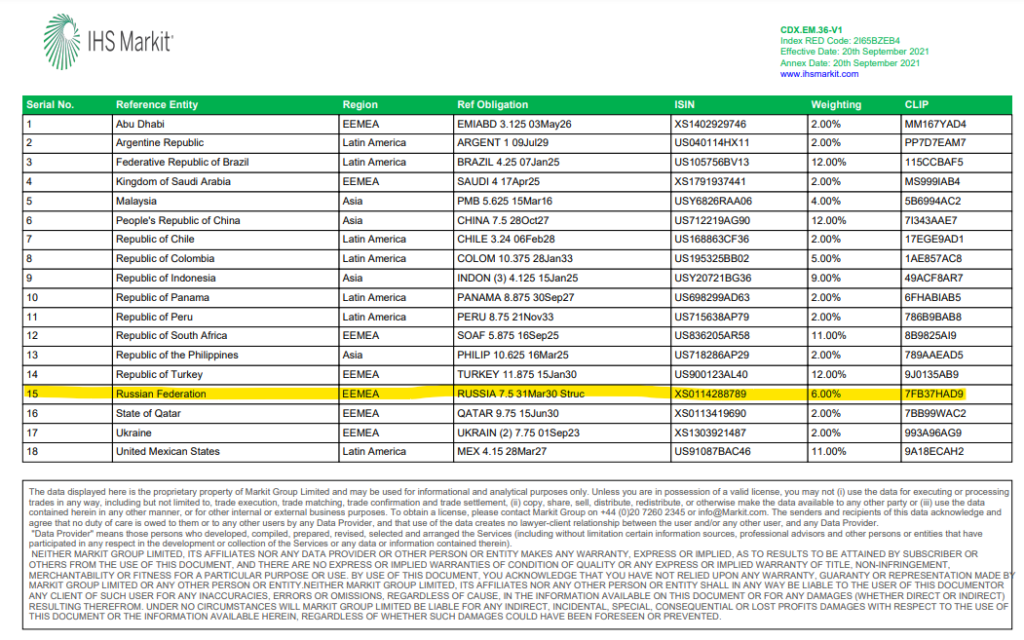

Well, I cannot see single name CDS vs Russia in our SDRView data – I guess that will be coming in a matter of weeks with SBSDR analysis. But there is activity in CDS Index trades. And a lot versus CDX Emerging Markets. A quick google of the current on the run CDX.EM series (Number 36) shows that one of the Index constituents is indeed Russia:

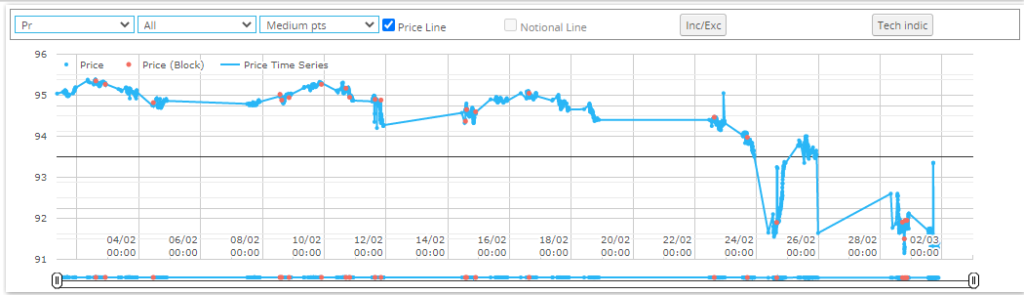

Here is the price chart from SDRView Pro:

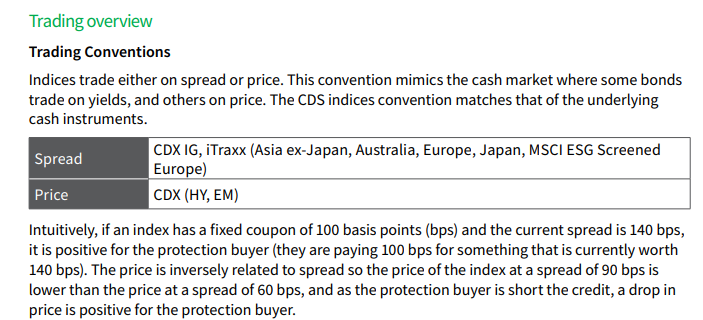

I was scratching my head a bit on this chart, until I read the (excellent) primer on CDS from the Markit website and realised that CDX.EM trades on Price not on Spread. Hence, prices go down as credit risk increases!

The chart therefore shows;

- Prices decreasing substantially, from 95.5 at the beginning of February to a low of 91.15 as of pixel time (2nd March morning).

- Trading has clearly become more and more volatile over the past month.

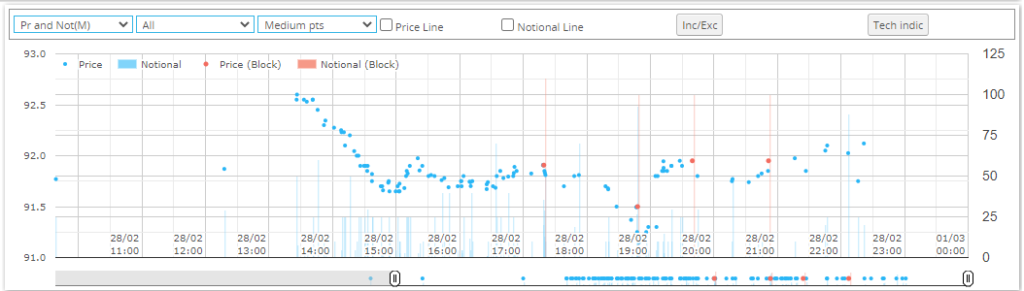

- It is difficult to assess whether the price action has “gapped” substantially. For example, price and volume evolution on an isolated day (28th February) looked fairly “healthy” despite all of the event risk in the background:

And whilst the index is clearly trading, volumes are not crazy compared to recent history:

Finally, we are approaching the roll period of CDX indices (they will roll from Series 36 to Series 37 in March according to the CDS Primer document). Looking at the index rules here there doesn’t seem any reason that Russia would be excluded from the new Series when it is published.

The Roll might be an interesting event to monitor IF the Series 37 isn’t quite as expected. Anyone know when we find out the constituents? I thought they would be out by now?

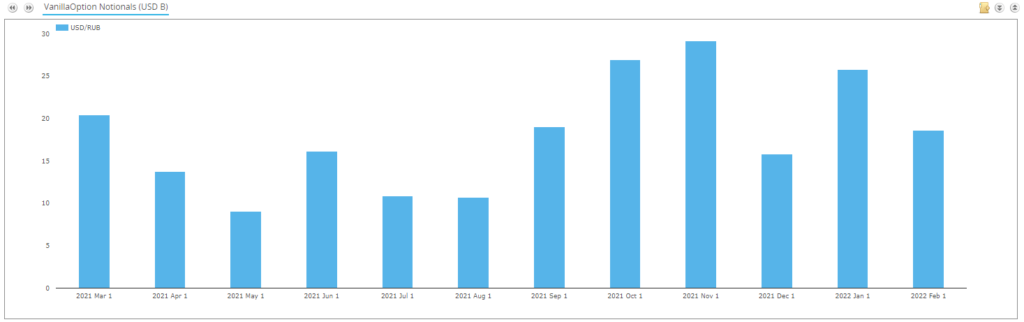

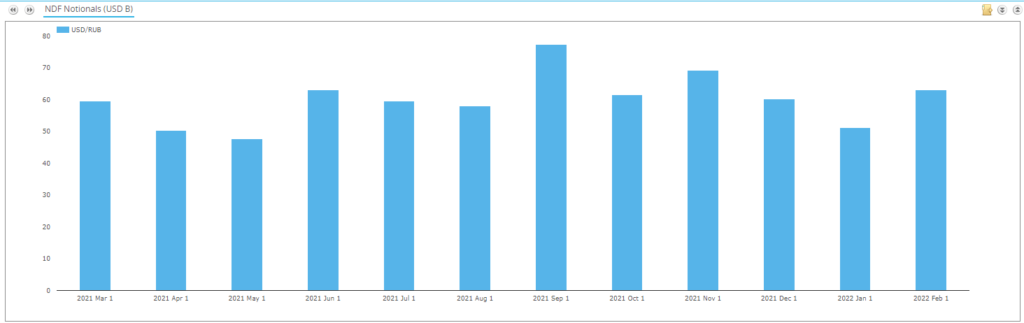

RUB FX Derivatives

Finally, we of course have some insight into what is trading in FX markets as well. For vanilla options, there is nothing of note in terms of volumes traded:

But I think what I would be doing is trading USDRUB NDFs! There are signs volumes in these are picking up (although RUB remains a deliverable currency I guess?):

Turns out this is not a particularly original thought. Risk.net reported on this a whole week ago!

In Summary

- Derivatives transparency allows us to monitor the continuing activity in RUB markets.

- Interest Rate Swap activity in RUB spiked in response to the central bank action this week.

- And Russia is a component of the CDX.EM CDS index, where trading continues despite huge event risks.

- FX markets are a little more opaque, but we see an increase in USDRUB NDF volumes which we can continue to monitor.