- Please note: this blog has now been corrected (25th February 2025) and updated impacts published on a new blog The European Active Account Requirements Revisited.

- The latest European Active Account Requirement suggests that 30,000 EUR swaps will have to be transacted in the EU each year, which is about 8% of the EUR swaps market.

- Approximately €1.25Trn of notional, equating to €1.2bn of DV01 risk, will be sufficient to satisfy the proposed requirements.

- These are within volumes already being cleared at Eurex.

27th January marked the deadline for the latest ESMA consultation on the European Active Account Requirement. Risk.net wrote a good summary of the requirements back in November when the consultation was first published:

What has been proposed?

The Active Account Requirement for OTC derivatives means the following trades must occur at a CCP located inside the EU:

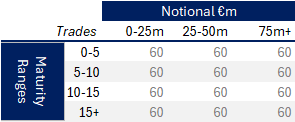

- For EUR swaps vs Euribor, 10-60 trades each year in four maturity buckets (0-5 years, 5-10 years, 10-15 years, 15 years+) covering 3 size categories in each maturity bucket (€0-25m, €25-50m, €50m+).

- For the largest firms clearing over €100bn a year, that means 60 trades in 12 different categories, potentially ranging from a €10m 2 year swap all the way to a €75m 30 year swap.

I found that I had to read those requirements three or four times for the numbers to sink in. So I found myself creating the following table, which I think effectively portrays the requirements for dealers:

How many trades?

That got me thinking – how many trades are we talking about in total? I needed to make some assumptions, so I have decided to model the European swaps market based on the following assumptions:

- 25 firms who clear more than €100bn per year. This is probably on the high side, feel free to make your own projections!

- 100 buyside clients who clear less than €100bn per year, but for whom 120 trades is less than half of their total activity.

- Which gives 25 * 720 = 18,000 dealer trades, and 12,000 client trades (assuming the two pools of trades are mutually exclusive – i.e. dealers only trade with dealers and that none of the client trades satisfy a missing “bucket” for a dealer).

- How significant is moving 30,000 EUR swaps every single year?

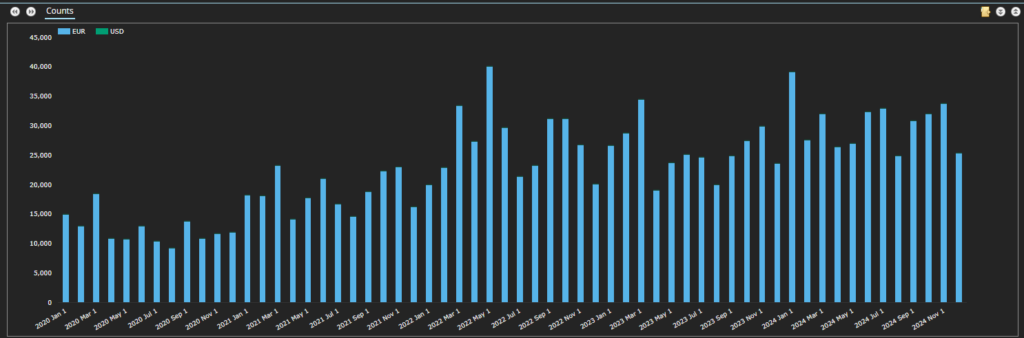

This is the kind of question that SDR data is designed to answer! Okay, so we don’t see 100% of the EUR swaps market, but it is a decent benchmark:

2024 saw 30,000 EUR swaps reported to SDRs every single month, for a total of 364,000 trades. The Active Account Requirement could impact as much as 8% of the swaps market.

How Much Notional

Hey, I’ve got a table in Excel, of course I’m going to run some simulations. You lot have read enough of my previous 500 blogs to expect that!

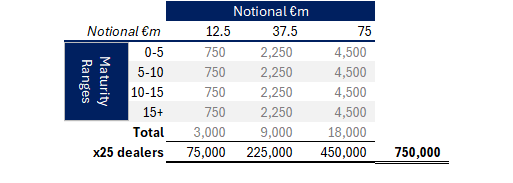

Translating my table into notional amounts gives me the following;

- Showing that €750bn of EUR Swaps notional could be impacted by the Active Account Requirement for dealers alone.

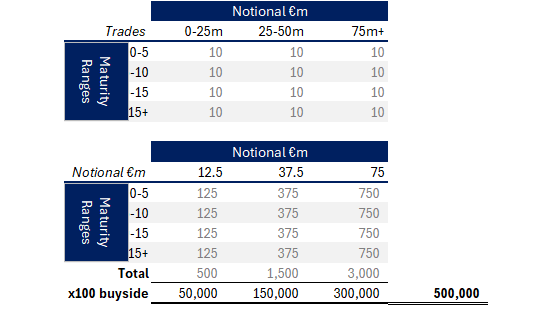

Repeating the calculations for buyside:

- Another €500bn of EUR Swaps notional could be impacted for buyside accounts.

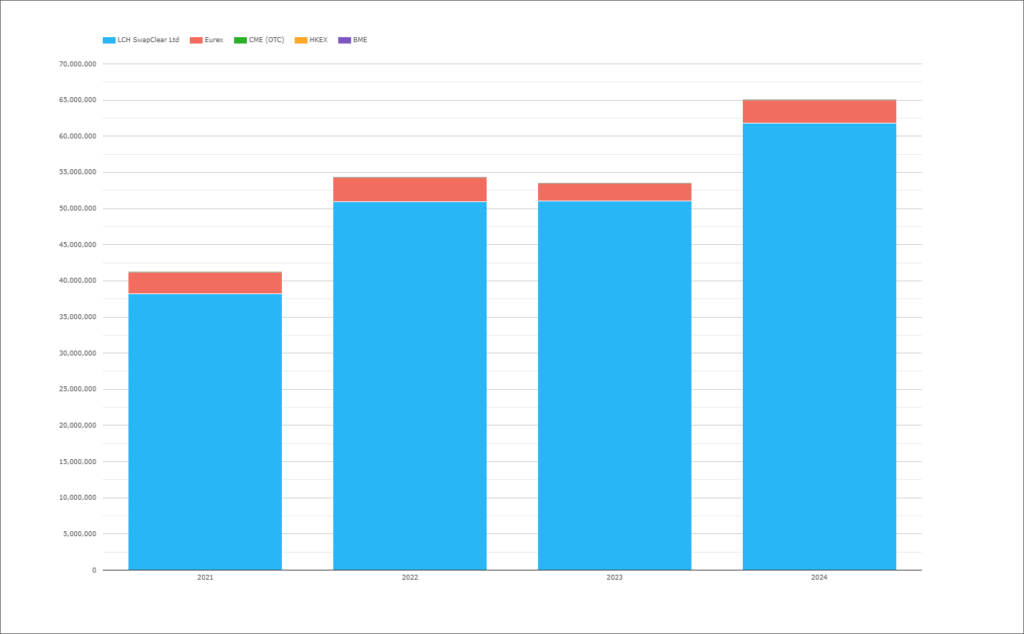

Overall we are talking about €1.25Trn of EUR swaps being impacted every year as a result of this proposal. Is that a significant amount? Let’s benchmark this amount in CCPView, which covers the global swaps market.

- In 2021, LCH SwapClear processed €38.2 Trn EUR swaps and Eurex €3Trn.

- In 2024, LCH SwapClear processed €62 Trn, Eurex €3.2Trn.

On a notional basis, €1.25Trn is “only” 2% of the swaps market. But moving this as “new” volume to Eurex would be pretty transformative, providing a 40% bump in Eurex volumes.

How Much DV01?

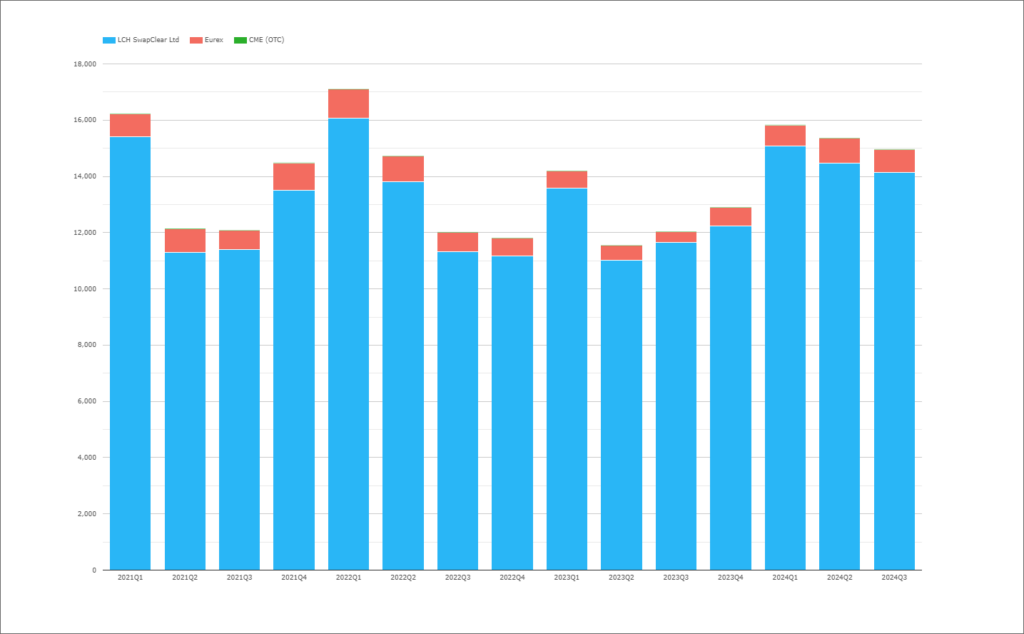

We write a lot about how we prefer to measure the market share of Eurex by DV01. A lot of notional at Eurex is transacted in short-dated FRAs, impacting the market share metrics between notional and DV01 measures.

On a DV01 basis, the market share of Eurex has varied from 3-7% in the past three years for EUR IRS:

How much DV01 do the Active Account Requirements translate to? Time to run the tables on DV01 instead:

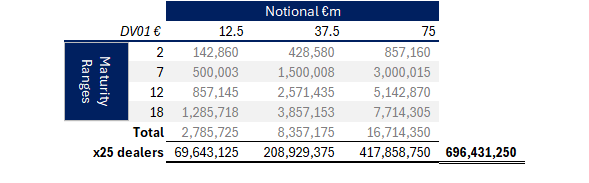

First for dealers, we find a total DV01 of €700m is required to satisfy the proposed requirements:

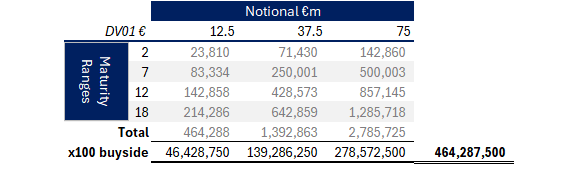

And for buyside, it equates to €465m of DV01:

This total of €1.16bn of DV01 per year compares to €2.8bn DV01 traded at Eurex in the past year, and hence is a very similar ratio to the notional number. Adding all of that as new volume would result in 40% more volume at Eurex.

The Numbers Look Reasonable

I think the numbers show that the proposal is reasonable. They are not huge compared to the global EUR swaps market, are within the volumes already being cleared at Eurex, and could lead to a reasonable degree of growth in clearing within Europe (and without threatening financial stability on day one).

We do not know how much of the requirements are already being met by either dealers or buyside. But given the scale of the numbers, it seems unlikely that anyone will “squeal” if they are implemented.

But…

This blog looks only at EUR interest rate swaps. I find it amazing that the same buckets will NOT be used for EUR OIS, or FRAs, or PLN IRS, or STIRs. I will leave readers to do their own analyses on those products.

In Summary

- Market Impact of Active Account Requirements: We estimate that the proposal requires 30,000 EUR swaps to be transacted annually in the EU, covering up to 8% of the EUR swaps market, with trades spanning 12 buckets across size and maturity categories.

- Notional and DV01 Affected: Approximately €1.25 trillion in notional and €1.16 billion in DV01 will be impacted annually by the proposal, providing a potential 40% boost to Eurex volumes compared to its current activity.

- Eurex Volume Context: Eurex cleared €3.2 trillion in notional and €2.8 billion in DV01 in 2024 for EUR IRS. The proposed requirements are well within existing capacity and align with Eurex’s market positioning.

- Reasonable Proposals: The scale of the requirements is manageable for both dealers and buyside participants, and is unlikely to disrupt financial stability.