With a huge Thank You to Eurex, I have to admit that I messed up on a recent blog post. It happens – we work to tight deadlines and cover complex topics. Still, I hold myself to a high standard and it really hurts when mistakes creep in.

What Did I Get Wrong?

On the blog “Running the Numbers on the European Active Account Requirement“, I stated that;

For the largest firms clearing over €100bn a year, 60 trades in 12 different (sub)categories, potentially ranging from a €10m 2 year swap all the way to a €75m 30 year swap (must be transacted within the EU).

The purpose of today’s blog is to clearly state that this statement was WRONG. Apologies. I missed a crucial word in the ESMA text:

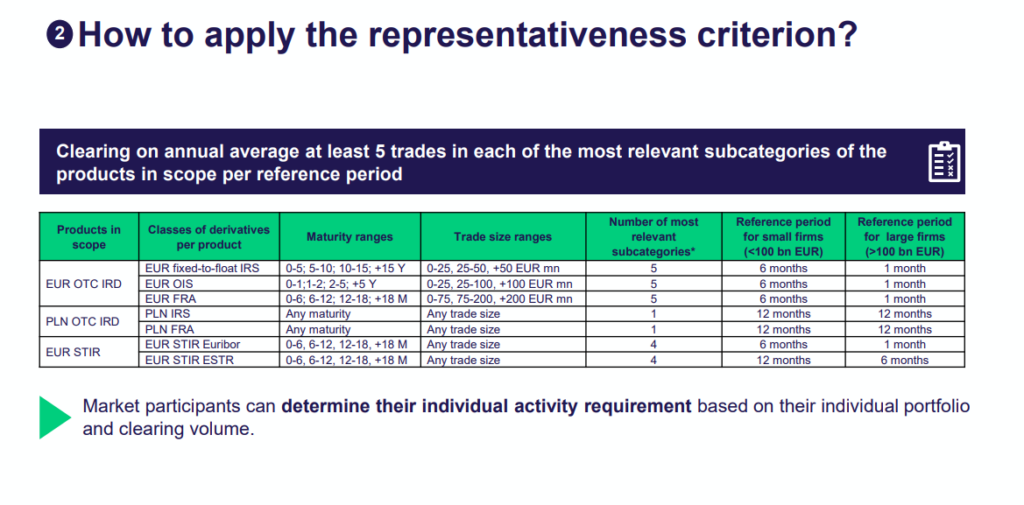

Counterparties will have to clear at least five trades in each of the most relevant subcategories per class of derivative contracts (emphasis the authors own)

Paragraph 90, Page 19, “Conditions of the Active Account Requirement“, ESMA.

And this brings us to the requirements in Paragraph 37, Page 30:

a) 5 most relevant subcategories for each of the 3 selected classes of EUR OTC IRD, i.e. EUR Fixed-to-float, EUR OIS and EUR FRA;

Reading it again, it is pretty obvious.

To clarify, counterparties do NOT have to trade 60 trades per year in each of the 12 subcategories. They have to identify the 5 most relevant subcategories for their franchise and transact 60 trades in each of those 5 subcategories. So we are actually talking about 5/12 as many trades as I originally wrote about.

Dealers will have to trade at least 300 trades (5 * 5 * 12) per year, and buyside 50 trades (5 * 5 * 2) to meet the requirements across the 5 subcatergories.

What Does This Mean for the Numbers?

Eurex have a good summary, which I am going to shamelessly link to:

A Eurex footnote clarifies the requirement (what is it with our industry and Footnotes?):

*The combination of maturity ranges and trade size ranges results in a maximal number of subcategories. Out of all possible subcategories, market participants need to determine their individual most relevant ones based on highest trading activity. Example: out of 12 possible combinations for EUR IRS, a firm has to identify its 5 most relevant ones. (Emphasis my own)

The Fifth Column (no, not that one) is the key criteria that I left out when running the original numbers. As a result, I am more inclined to agree with the sentiment of the Risk.net article now – why make it so complicated? Just define 5 subcategories rather than 12. Why make counterparties suffer the complication of having to work out which 5 are the most relevant? Maybe I am just grumpy because I got it wrong in the first place!

How many trades?

Using my new understanding, let’s go ahead and model the European swaps market based on the following assumptions:

- 25 firms clear more than €100bn per year. This is probably on the high side, feel free to make your own projections!

- 100 buyside clients who clear less than €100bn per year, but for whom 120 trades is less than half of their total activity. This is likely on the low side, with up to 300 clients in the EU.

- Which gives 25 * 300 = 7,500 dealer trades, and 100 * 50 = 5,000 client trades per year. This assumes the two pools of trades are mutually exclusive – i.e. dealers only trade with dealers and that none of the client trades satisfy a missing “bucket” for a dealer.

- How significant is moving 12,500 EUR swaps every single year?

- That is about 3.5% of the EUR Swaps market reported to US SDRs.

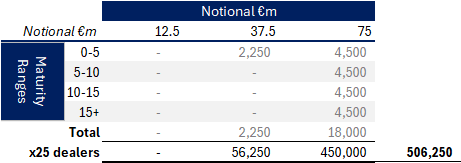

How Much Notional?

Translating my revised trade numbers into notional amounts gives me the following;

- Showing that a maximum €506bn of EUR Swaps notional could be impacted by the Active Account Requirement for dealers alone.

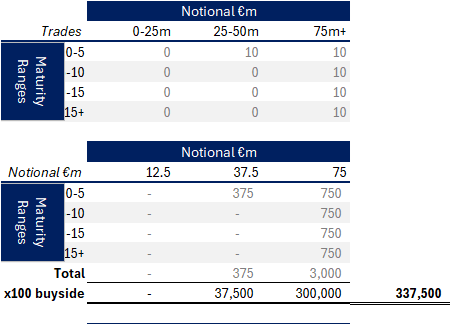

Repeating the calculations for buyside:

- Another €337bn of EUR Swaps notional could be impacted for buyside accounts.

Overall we are talking about less than €850bn of EUR swaps being impacted every year as a result of this proposal. In DV01 terms, it equates to €890m DV01.

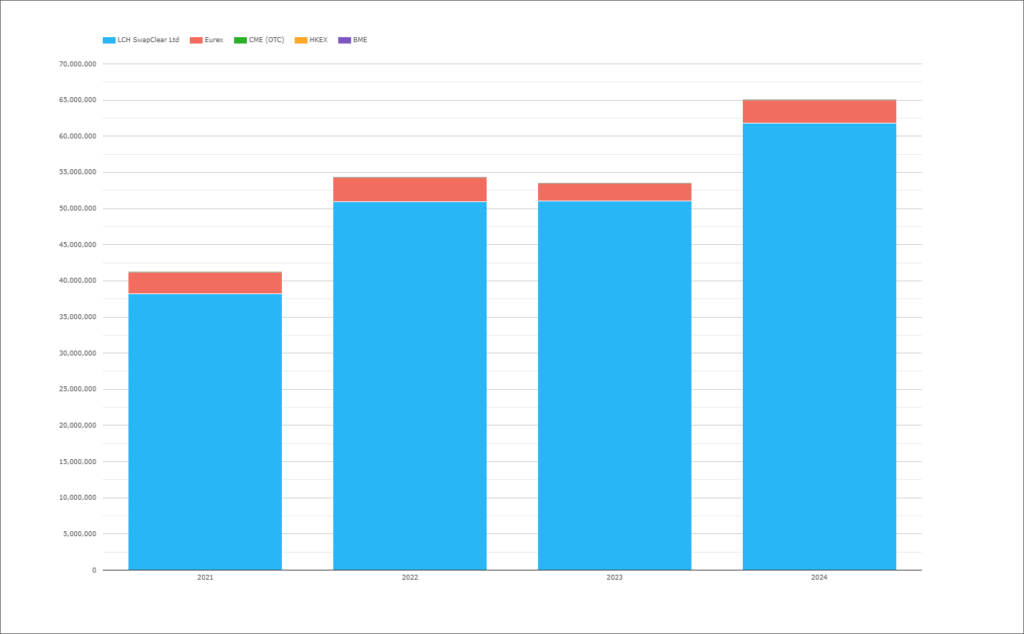

CCPView, which covers the global swaps market, shows that Eurex clears about €3Trn every year in EUR swaps:

- In 2021, LCH SwapClear processed €38.2 Trn EUR swaps and Eurex €3Trn.

- In 2024, LCH SwapClear processed €62 Trn, Eurex €3.2Trn.

In Summary

- My first pass at these regulations was wrong: I missed the detail about applying the requirements to the 5 most relevant subcategories. That is not a great sign and suggests that the industry will be unhappy with the level of complexity in this proposal.

- Market Impact of Active Account Requirements: We estimate that the proposal requires 12,500 EUR swaps to be transacted annually in the EU, covering up to 3.5% of the EUR swaps market.

- Notional and DV01 Affected: Approximately €840 billion in notional and €890 million in DV01 will be impacted annually by the proposal, providing a potential 25-30% boost to Eurex volumes compared to its current activity.

- Eurex Volume Context: Eurex cleared €3.2 trillion in notional and €2.8 billion in DV01 in 2024 for EUR IRS. The proposed requirements are well within existing capacity and align with Eurex’s market positioning.