Over the past week, we got final word on the plan for packaged trades on SEF. We now have a phased-compliance timeline as follows:

- May 16 – packages where all components are MAT.

- June 2 – packages with at least one MAT swap combined with other swaps that (while not MAT) are subject to clearing requirement

- June 16 – Spreads over US Treasuries, where the swap components are MAT

- November 16 – Packages that include an MAT swap and:

- Futures

- A swap that is not subject to clearing requirement

- A swap that is not CFTC-regulated

So to digest all of this, you might do well to review which products are MAT again. With this fresh in your mind, lets look at some examples of what is in and out on the timeline:

- May 16: 7YR/10YR spread rate switch would be included (both are MAT). An 8YR/10YR rate switch would not, as the 8YR is not MAT.

- June 2: Our 8YR/10YR curve trade would fall into this.

- June 16: 10YR spreads over treasuries.

- November 16:

Lets try to figure out what this might mean. But first, data.

DATA

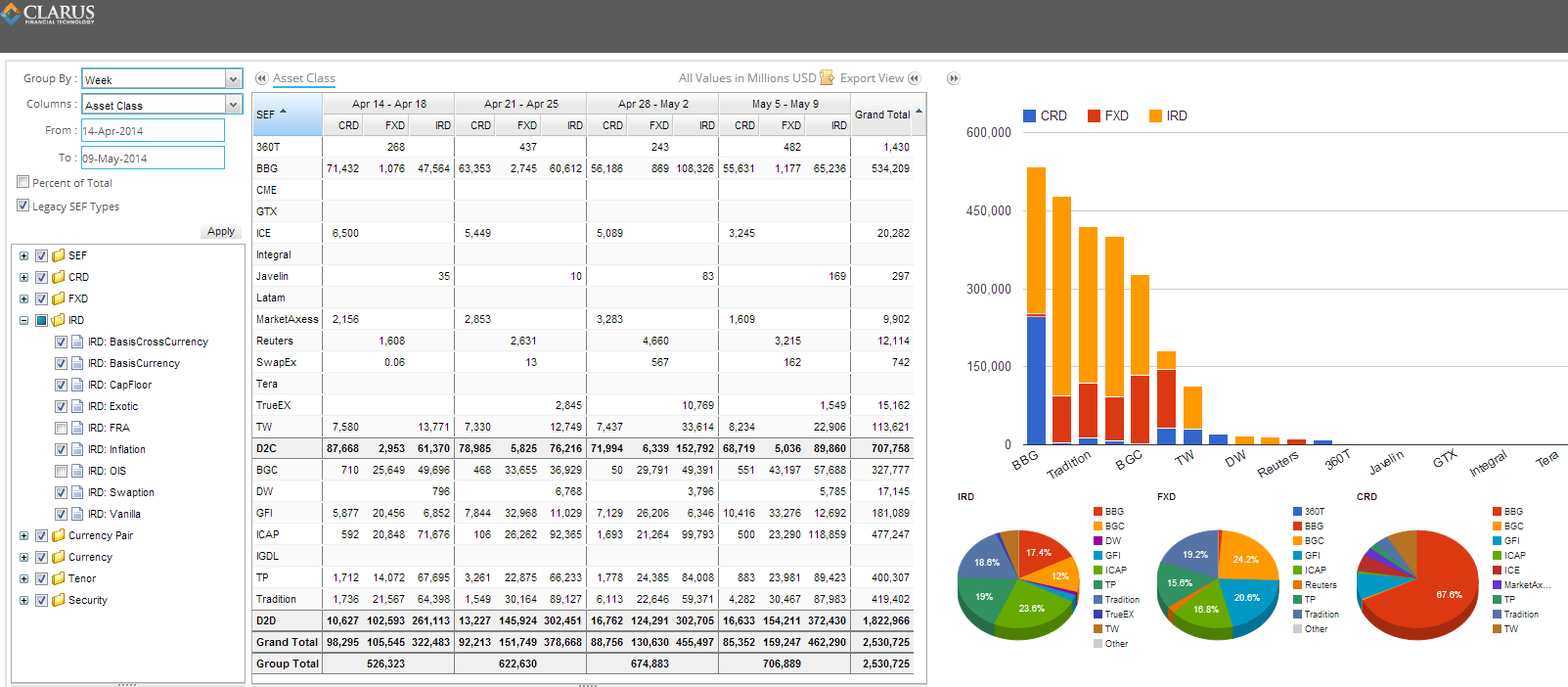

First lets have a peek at the trailing 4 weeks of SEF data. I have decided to normalize the data this week by excluding both FRA’s and OIS.

It’s interesting to note Bloomberg’s activity in IRD over the previous few weeks:

- During the week of April 28 – May 02, Bloomberg appeared to have eclipsed the IDB’s in interest rate derivatives (108bn vs 99bn for nearest alternative)

- This is almost certainly down to the April 29 Apple Bond issue of $12b, consisting of 3Y, 5Y, 7Y, 10Y, 30Y issues.

- As in the other 3 weeks, Bloomberg activity reverted to the norm.

WHAT IS GOING TO CHANGE

Lets collectively look into the crystal ball and see if we can come up with a guess of what we can expect to see from the most recent guidance on packaged trades.

First stop, headline On/Off analysis. SDRView Professional shows us that for Wednesday May 7, 60% of USD swaps were traded ON-SEF, 40% OFF-SEF. Spot checking May 7 to other days shows this split mostly consistent between On and Off SEF activity.

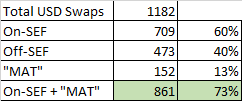

1,182 Total trades, 102 bn total notional. Of which:

- 473 trades (40%) and 49bn (48%) is OFF-SEF

- 709 trades (60%) and 53bn (52%) is ON-SEF

Hence, what we need to do is to investigate the 473 Off-SEF trades and find ones that appear to be “required trades”, but are still off-SEF:

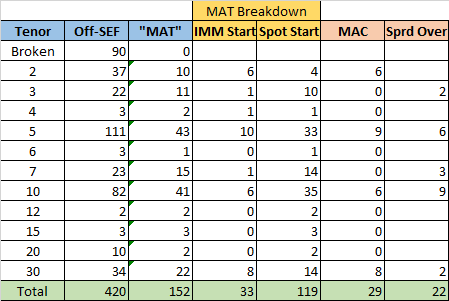

The first thing to note is that of the 473 trades, 53 of them are not on MAT-able tenors. This leaves 420 swaps. Of those 420 swaps, the ones that meet the Par or MAC rate / Spot or IMM start / MAT tenor criteria is summarized in the table below:

What this tells us is that 152 of the 420 Off-SEF swaps are “MAT-able”. I went the extra mile and brokedown the 152 MAT-able swaps into IMM-start and Spot Start. And of the IMM-start (33 trades), I’ve denoted how many are MAC contracts (29 trades). Further, of the 119 Spot-start swaps, I’ve denoted how many of these have been priced at 5-decimals, meaning they are most likely spread over treasuries (22).

Taking all of this into account, we can start to make some guesses. Lets assume that that all of these “MAT-able” swaps become On-SEF by July 16. This would mean that 152 of the 420 currently Off-SEF trades on this date would be On-SEF. This would come to a total of 73%:

JUST GIVE IT TO ME STRAIGHT

Lets summarize this:

- Approximately 60% of USD IR swap activity is traded On-SEF

- If you assume that all USD IR “MAT-able” swaps get traded On-SEF, that total would increase to 73% of daily trade activity

Now, lets be clear on some of the pitfalls of this analysis:

- There are a good degree of fwd start, non-IMM swaps that are simply not MAT

- This analysis does not look at non-MAT-able swaps that might get packaged with MAT-able swaps (which would make them “required”)

- The horizon of this analysis is only as far as the 16-July packaged trade relief

So with all of these caveats in place, I could estimate an increase in SEF activity, over current activity, by 16-July, within the USD IRD market, from 60% to 73%, or perhaps a 20% increase. Given that USD IR activity is only a portion of the total SEF activity (and only USD, EUR and GBP are MAT-able), I am hesitant to predict much of an increase.

So wait, only 73% of the USD IRD market is MAT-able after the package exemption ends? I am starting to be wary of whether there has been an increase in non-MAT-able trades. Could it be the case that institutions have begun to trade non-spot-starting, or not-quite-par, or not-quite-5-YR swaps? That is an analysis for another day.

Dare I guess, that the true growth of SEF activity will only come when we break down the barriers of MAT. That is to say, when any-start, any-rate, any-tenor swaps become “required”.

PREDICTION

I have become a glass-half-full kind of guy. I’ve seen us go through the February MAT-week with a giant sigh. I just don’t see a massive change to occur over the coming weeks.

The package trade relief starts to expire on Friday May 16. So for the current week, we may not expect much change. If we benchmark the last 4 weeks of SEF IRD activity at (excluding OIS and FRA):

- 261 bn (14-Apr – 18-Apr)

- 302 bn (21-Apr – 25-Apr)

- 303 bn (28-Apr – 02-May)

- 372 bn (05-May – 09-May)

And don’t forget that two of these previous weeks have been Easter holiday weeks.

I am going to place a wager that over the next couple weeks, we’ll come in at a ho-hum 350 bn this week (12-May through 16-May) and 330 bn next (19-May through 23-May).

Further, we’ll go into June wondering why nothing has changed.

So assuming I am right, there are more questions to be answered. But lets wait and see. My crystal ball might be due for servicing.