Nearly 2 weeks ago, Tullet Prebon announced their SEF filing with the CFTC, which inspired me to do some research into the SEF registrations to date. I blogged about it here; who they are, what they had planned to provide, etc. Towards the end of the blog, I posed the question, where was ICAP, BGC, and Tradition?

FAST FORWARD TO TODAY

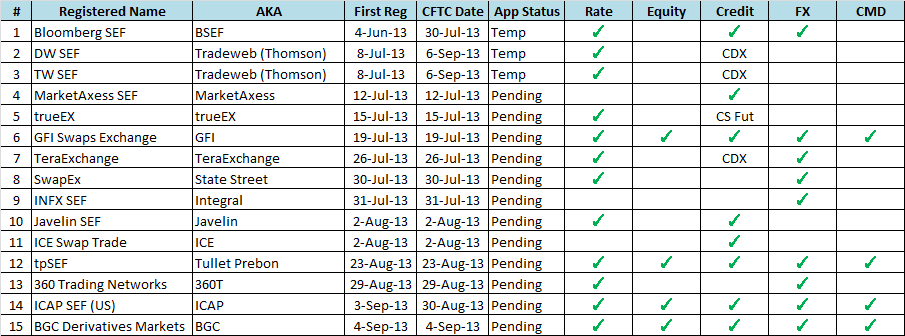

12 whole days have passed and we have received some answers. The table below provides a current summary of all SEF filings, based on data provided from the CFTC website.

I’ve added a column “First Reg” to denote the first registration date, as the “CFTC Date” seems to represent the most recent update in status at the CFTC. I have sorted by the “First Reg” date, so we can see who was the earliest to the game.

I have also added an “AKA” column, as in some cases it is not entirely clear who the SEF belongs to, or what the SEF is otherwise known as. For example, a layman reading the CFTC website might wonder who is tpSEF, who does SwapEx belong to, or wonder how Thomson Reuters is represented.

The notable changes from 2 weeks ago are the additions of 360T, ICAP, and BGC.

INTERPRETING THE SWATHE OF INFORMATION

Once again, I’ve tried to interpret as best as possible the products that will be offered via each SEF. You would think this would be straightforward. After all, the CFTC provides a list of the documents that have been filed by the SEF. Surely, somewhere in the 20+ documents that are required for each SEF, you could find a list of products they intend to offer.

Two problems with that approach exist. Primarily, it would appear that there is no requirement to explicitly list the intended products. After all, there is the parallel process of making products available to trade, so arguably, if you are a SEF, you can make anything available to trade. Second, most of the firms have taken liberty with the Freedom of Information Act, and requested many of the documents, appendices, and exhibits to be kept confidential. I’ve relied on each SEF’s submitted Exhibit L in most cases, which trolls through each SEF’s intended compliance with the SEF core principles. In here, you can begin to make educated guesses based upon the SEF’s responses. Further, Exhibit T lists the intended DCO’s, which can also give insight into which products will (or will not) be supported. So I have had to rely on a mix of information, primarily the formally filed (and not confidential) documents, coupled with the press releases and word of mouth that each SEF has generated.

WHAT DOES THE NEAR FUTURE HOLD

I would anticipate a few more SEF filings in the coming weeks. However now that the big 4 IDB’s are represented, the only omission remaining from my original forecast is Tradition. Taking out my crystal ball yet again, I am guessing there are a few old-school DCM’s that we are likely to see crop up to cover both of the DCM and SEF bases. Only time will tell.

Lastly, as the list begins to grow, the question I am forced to ponder is: “How are the SEF’s going to differentiate their business and attract liquidity?” Does anyone have a crystal ball for this one? Feel free to comment with your forecasts.

To attract liquidity I would think the SEF needs to :

– Have a better fee structure for client side clearing.

– Easy to connect to platform (eg ICE has pretty much all fed 14 on it)

– Margin management

– Ability to clear to other venues eg BSEF to LCH or ICE…

Add CME to the list…

CME Group Files an Application to Be Registered as a Swap Execution Facility

CME Group, the world’s leading and most diverse derivatives marketplace, announced today that it has filed an application to be registered as a Swap Execution Facility (SEF) with the Commodity Futures Trading Commission (CFTC). CME Group’s SEF will be available over CME Direct, a sophisticated online front-end trade management platform for accessing CME Group’s deeply liquid exchange listed and OTC energy and metals markets.

CME Group’s SEF will offer customers the flexibility they need for executing swaps side-by-side with listed futures over CME Direct in markets where we have a strong presence.

CME Group will initially focus on commodity products, and will look to develop additional markets over time with the industry.

Yes indeed, one of a few changes (eg CME, Tradition, Reuters). An update / new blog is in the works for release in the coming days.