In March 2019, just over 8 years after its launch, SGX shut down it’s OTC Financials Clearing business. However SGX continues to innovate and has focused on the futures market. One example of this is the launch of FlexC FX Future, a product which aims to replicate a Non-Deliverable Forward and capture liquidity/volume from the OTC market.

We have been asked a number of times by Clearing Brokers in Asia to review this product, so I decided to took a deeper look.

The Basics

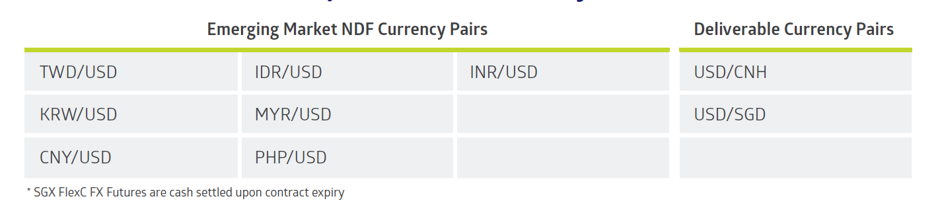

The FlexC FX future product aims to replicate seven non-deliverable and two deliverable FX products. It allows a settlement price, for delivery up to 100 days in the future, to be negotiated bi-laterally between two market participants and then reported to SGX for clearing though SGX’s Titan application. The contract sizes are relatively small, around USD 25K per contract.

The currency pairs supported are as follows:

These futures are margined using 1-day Span, with margin offset benefits between these and other derivative products cleared at SGX. (Product brochure available here).

The Benefits

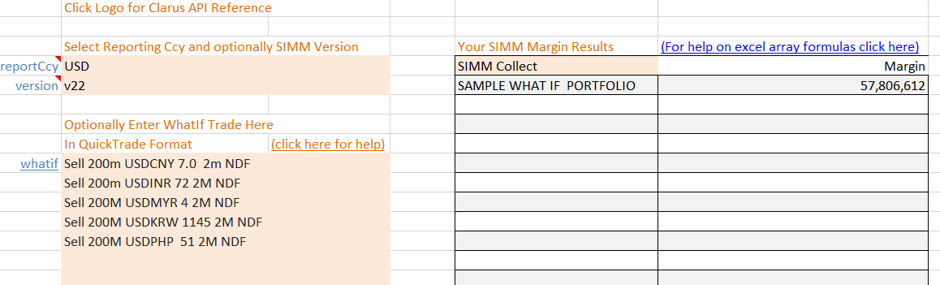

The first benefit main is the margin reduction. For a sample portfolio of 5 FX NDF trades, where the notional exposure is around USD 1B, the following Margin number can be calculated using Clarus SIMM for Excel.

This shows and IM number of around USD 57.8M. The same IM for the same set of trades booked as futures is about USD 18.5M a significantly lower amount of IM. The futures IM number is before any risk reduction that you may get from offsetting future positions in other product types.

A second benefit is paperwork. If you have an account for derivatives clearing at SGX you can clear this product. No additional paperwork such as that required trade under UMR or joining a clearing service such as LCh ForexClear.

The Technology

It has been reported that the FlexC contract requires a technology upgrade for clearing members to support it. It is always a bit of a challenge having legacy technology being a roadblock to the adoption of a new product. It is rumoured that around half of SGX’s derivative clearing members have implemented the required changes to their clearing systems to support this product which is a great start, but given the hard time an SGX panellist gave a FIS panellist at the FIA Asia event in early December, vendors probably still need to deliver on some of their promises in this area!

The Drawbacks

The key challenge with the development of a new contract is the creation of a liquidity pool. SGX has engaged with Tradition to provide support in creating a marketplace for the product and SGX has taken a strategic investment in BidFX which one can only assume this is to support the development of liquidity.

One of the other challenges is the Futures nature of this product. The currency pair of each of the non-deliverable products is defined as NDF currency versus USD, which is to keep to the conventions used for FX Futures. The OTC NDF market trades as USD versus NDF Currency. This approach means that enterprise risk management systems will need to be re-configured or upgraded to net OTC and ETD FX NDF positions.

In Conclusion

SGX recently cleared their first trade with the Singapore entities of Bank of China and ICBC, clearing the deliverable USD/CNH futures (see here), so trades are starting to be executed. The product has been designed to be easily accessible with little or no admin to add it to an existing clearing account at SGX, a lesson that SGX appear’s to have learn’t from the challenges with it’s OTC Clearing service. As with most innovative new products, technology and liquidity are crucial to success. It will be interesting to watch how volumes develop in each currency pair over the course of the year.