ISDA, SIFMA and other trade associations recently published a letter addressed to BCBS and IOSCO, which makes very interesting and important recommendations for the remaining phases of the IM implementation required under Uncleared Margin Rules. (full letter here).

Background

Uncleared margin rules (UMR) required Phase 1, 2 and 3 firms, with >$3 trillion, >$2.25 trillion and > $1.5 trillion gross notional of uncleared derivatives (in Sep-16, Sep-17, Sep-18) to collect and post Initial Margin with their counterparties, where this exceeds $50 million. Currently 50 large firms are covered by these rules.

Phase 4 in Sep-19 requires firms with > $750 billion gross notional of uncleared derivatives to do the same, while Phase 5 firms with > $8 billion gross notional will be captured in Sep-20.

Letter Recommendations

The letter requests regulatory assistance with the impending substantive challenges associated with the final phases of UMR and based on the results of a quantitative data survey, makes the following recommendations.

Before I look into each of these, it is important to summarise the key findings from the quantitative survey.

ISDA Quantitative Data Survey

Full details of the Quantitative Analysis with result tables are referred to in the letter, but I could not find them, so I assume they are not public; nevertheless the highlighted findings are very interesting.

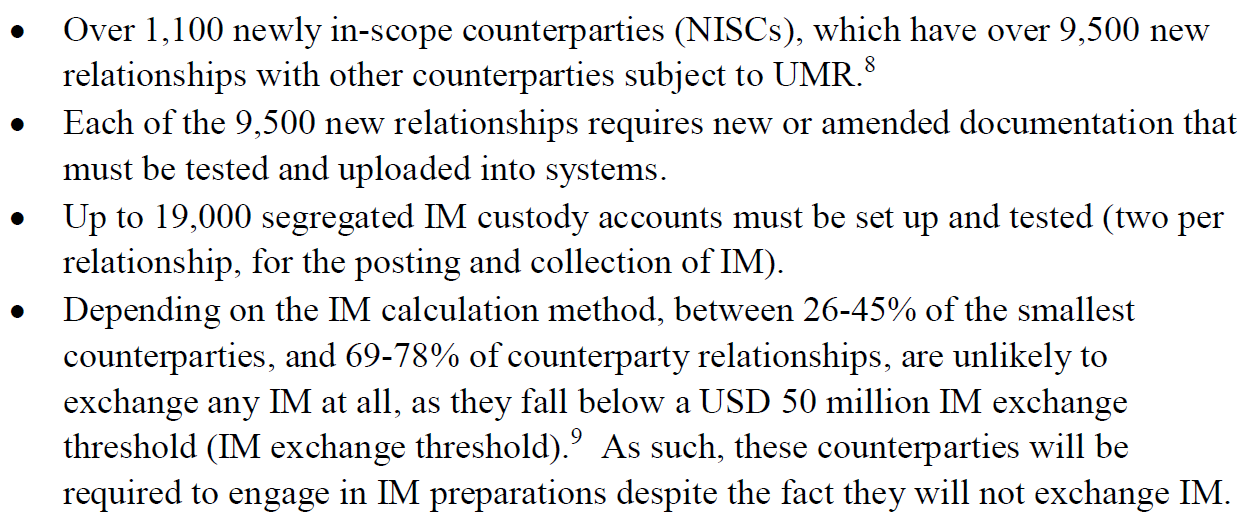

The data covers 16,340 separate legal counterparties, with 34,680 individual relationships and estimates the following impacts for Phase 5 of UMR:

Wow, 1,100 newly in-scope counterparties for Phase 5!

That is some increase from the 50 currently in-scope. (I was not able to find an estimate of Phase 4 numbers).

No wonder there is a concern with ” the impending substantive challenges”.

The letter then continues with:

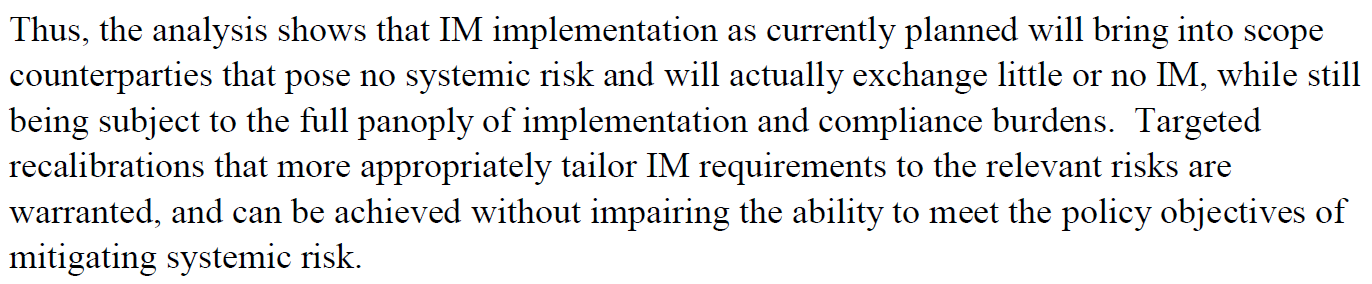

It further argues that as central clearing has grown steadily since clearing mandates were implemented and is incentivised by the benefits of multi-lateral netting, it is not necessary or appropriate to impose prohibitive IM requirements on Phase 5 counterparties that pose little systemic risk as a further incentive to clear. In fact, imposing such burdens and costs may deter NISCs from using derivatives to effectively manage their risk.

Let’s now consider the four major recommendations and do so in what I view as the least contentious order, on the assumption that this is also the most likely to happen order.

A2 Remove FX Swaps and Forwards from the $8 billion calculation

The calculation of the aggregate average notional amount (AANA) thresholds includes the notionals of physically settled foreign exchange (FX) swaps and forwards, even though these are not subject to IM, as they are short-dated, liquid and present low long-term risk. (Presumably also as many users of FX Swaps need the physical currency and may not want to/be able to use the product if it also had to be margined).

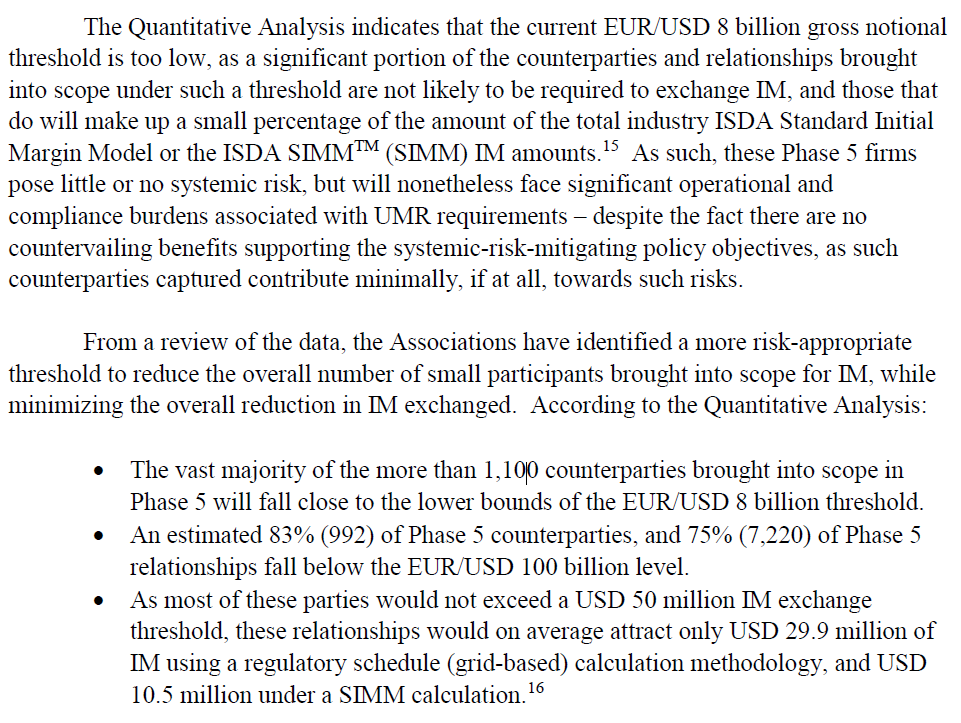

The Quantitative Analysis indicates that 19% or 227 of Phase 5 counterparties and 14% or 1,363 of Phase 5 relationships will fall into scope of regulatory IM requirements only because of the inclusion of FX swaps and forwards in the AANA calculation. Further it shows these 19%, would only account for 2.5% of the total grid-based IM posted by all Phase 5 firms in the first two years of their regulatory IM obligations.

This seems to me a clear cut argument for this recommendation and it should be adopted by regulators, as I am not aware of any real real for not doing so.

B1 Exempt Phase 4-5 non-dealer counterparties from prudential-style governance of IM models

The requirements under these rules, which the letter refers to as “prudential-style governance,” are based on those in use at banks to comply with capital requirements and include: internal initial validation, regulatory approval, model documentation, ongoing monitoring, back testing, benchmarking and independent auditing.

ISDA SIMM has been widely approved and accepted by global regulators, is the primary margin methodology used for UMR and is well known to regulators and markets participants alike, with SIMM model performance monitoring on actual portfolios takes place on a global basis co-ordinated by ISDA.

Given this, the letter argues that there is little benefit and significant cost in requiring non-dealers to comply with these requirements, as they would require entirely new processes and systems alien to such firms; with one likely result being to push these firms to use schedule IM, which is less risk sensitive and requires much more collateral to cover IM.

In-fact under U.S. rules, such model-related requirements generally apply only to swap dealers.

However under EU and Japanese rules, they apply to all in-scope counterparties.

So it seems to me that this recommendation should also be adopted.

(A further benefit mentioned, is that removing these requirements would make it more likely that dealers or third-parties would be willing to IM calculations for those NISCs that would prefer to outsource this).

B2 Exempt non-dealers from any SIMM approval (and/or pre-approval) under EU and Japanese UMR

ISDA SIMM use is subject to internal model approval, similar to the manner of capital regulations. Not only do model approval materials require significant expertise and resources in their preparation but at the same time regulators will face challenges in reviewing the high number of counterparties in scope for Phase 5.

Such materials and efforts are largely duplicative to those already performed by ISDA and Phase 1-3 firms and a possible consequence on NISCs is to push them to use Schedule IM.

The corollary to this argument is that it is prudent for regulators to engage with firms to ensure they have people and systems with a good understanding of important models they use and not just black boxes with outputs taken at face value.

However on balance, I again find myself agreeing that this should recommendation should be adopted.

In-fact I struggled with putting this before B1 or not?

Onward.

A1 Raise the Gross Notional Threshold for Phase 5 to $100 Billion

This brings us to the final one and the one that gave me “sticker shock”, raising $8 billion to $100 billion, which on the face of it seems a massive increase, even when bearing in mind that the Phase 4 threshold is $750 billion. The justification re-produced from the letter is:

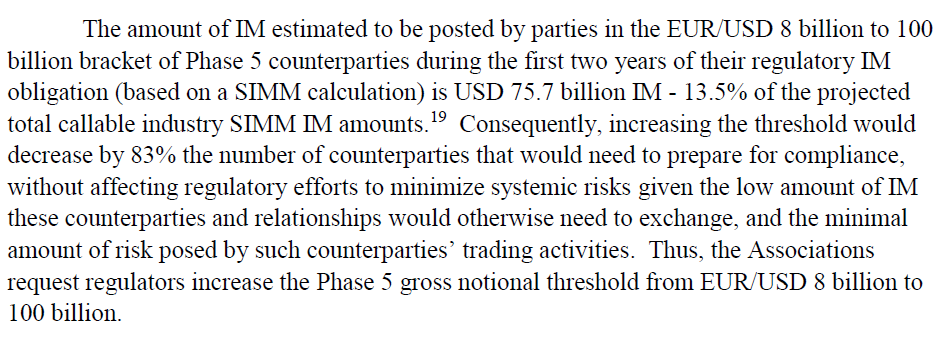

To summarise, the vast majority of the 1,100 counterparties fall close to the $8 billion threshold and most of these would not need to exchange IM as they would fall below $50 million for each of their relationships, which on average would require $10.5 million SIMM IM.

The letter further states that “if the Phase 5 gross notional threshold was increased to $100 billion, the average SIMM IM amount per counterparty (for all of their relationships) that would not be posted is estimated to be $76 million. In contrast, the 25 Phase 1 and 2 firms are collecting an average of $5 billion per firm.

And then there is this:

My thoughts

So after overcoming “the sticker shock”, am I convinced? And more importantly are regulators likely to be?

The argument rests on the fact that the vast majority of Phase 5 firms will not be required to exchange IM, as each of their relationships will be below $50 million. However what if the $50 million was $25 million, would the argument still hold? Clearly not as strong as more firms would be exchanging IM.

Also $76 billion IM is 13.5% of overall IM, a not an in-significant amount for the 992 firms that would be excluded, and excluding these leaves 108 firms in P5, a sharp drop indeed.

Now I don’t know the justification for $50 million, as opposed to any other figure and of-course if a firm is not comfortable with the credit risk of a counterparty, it can ask for discretionary IM of any amount, even $1 million. I know having a threshold is useful as it reduces the requirement for collateral, which might be in short supply, but why it has been calibrated to $50 million, I do not know.

I am also not sure where the $8 billion threshold comes from? Possibly from the US CFTC de minimis exception rules for swap dealers to register with the Commission or possibly just the law of familiar numbers, either way the justification is not obvious.

In addition, we have seen from the data that UMR IM deadlines have resulted in P1 and P2 counterparties shifting non-mandated products into clearing, namely non-deliverable forwards and inflation swaps and possibly others going forward.

I would be concerned that removing this carrot, will remove a key incentive for P5 firms to clear, as the benefit of multi-lateral netting of a cleared product is not sufficient incentive over netting un-cleared products with a single dealer relationship.

Considering the above, it seems to me to be too radical a change for regulators to accept the recommendation to increase the $8 billion threshold to $100 billion.

Should it be increased to a lower number, say $25 billion or $50 billion?

Or should it be increased at all?

Or possibly some sort of deferral or no-action letter to cope with the burden?

Or a Phase 5a and Phase 5b to segment the number of firms captured?

I am not convinced on any of these choices.

The Summary

The ISDA letter makes four major recommendations.

I think three of these should be adopted.

Doing so will significantly reduce the number of firms subject to IM.

And will also reduce the burden on other firms.

While making no material change to systemic risk objectives.

So well worth adopting, provided the legislation can be changed in time.

The fourth recommendation, for an $100 billion threshold, seems too radical.

Much more work will be required to justify such a change.

So I consider it unlikely to fly.

Still three out of four would be a very good result.

Only time (and regulators) will tell.

One of our readers pointed out that a QIS impact study for UMR was done and teh results published in https://www.bis.org/publ/bcbs242.pdf

A key paragraph on the $50 million threshold is “The near-final proposal requires two-way initial margin requirements with a universal threshold of €50 million. The initial margin that would result from applying the nearfinal proposal to the derivative portfolios that are expected to remain uncleared at the QIS respondent firms is roughly €558 billion. Extrapolating from the QIS respondents to the entire global derivatives market would raise the estimate to roughly €0.7 trillion. Margin requirements using a zero threshold rather than a threshold of €50 million, as proposed in the July 2012 consultative paper, would result in roughly €1.3 trillion of initial margin at QIS respondents or roughly €1.7 trillion for the entire global market. Since the near-final proposal would only apply the requirements to new transactions, the margin would be posted gradually over time as new transactions replace old ones.”